What is Global Recordable Optical Disc Market?

The Global Recordable Optical Disc Market refers to the industry focused on the production, distribution, and sale of optical discs that can be recorded or written onto by users. These discs include CDs, DVDs, and Blu-ray discs, which are used for storing data, music, videos, and other digital content. The market encompasses various segments, including blank discs for personal use, pre-recorded discs for commercial distribution, and specialized discs for professional applications. The demand for recordable optical discs has been influenced by technological advancements, changes in consumer preferences, and the rise of digital streaming services. Despite the growing popularity of cloud storage and digital downloads, optical discs remain relevant due to their durability, portability, and ability to store large amounts of data securely. The market is driven by factors such as the need for physical backups, the popularity of home entertainment systems, and the demand for archival solutions in various industries. As technology continues to evolve, the Global Recordable Optical Disc Market adapts to meet the changing needs of consumers and businesses, ensuring the continued relevance of optical discs in the digital age.

CD, DVD, Blu-ray Disc in the Global Recordable Optical Disc Market:

The Global Recordable Optical Disc Market includes various types of discs, each serving different purposes and offering unique features. CDs, or Compact Discs, were among the first optical discs to gain widespread popularity. They are primarily used for audio recordings, data storage, and software distribution. CDs have a storage capacity of up to 700 MB, making them suitable for storing music albums, small software applications, and personal data backups. DVDs, or Digital Versatile Discs, offer a higher storage capacity than CDs, typically ranging from 4.7 GB to 8.5 GB for dual-layer discs. This increased capacity makes DVDs ideal for video content, including movies and television shows, as well as larger software applications and data storage. DVDs have been widely used in the entertainment industry for distributing films and TV series, and they remain popular for personal video recordings and data archiving. Blu-ray Discs represent the next generation of optical discs, offering significantly higher storage capacities, typically starting at 25 GB for single-layer discs and up to 50 GB for dual-layer discs. Blu-ray technology provides high-definition video and audio quality, making it the preferred choice for modern home entertainment systems and high-definition content distribution. The development of Blu-ray discs was driven by the increasing demand for high-quality video and audio experiences, as well as the need for larger storage solutions for digital content. In the Global Recordable Optical Disc Market, each type of disc has its own niche, catering to different consumer needs and preferences. CDs continue to be popular for music enthusiasts and collectors, while DVDs are favored for their affordability and compatibility with a wide range of devices. Blu-ray Discs, on the other hand, are sought after by consumers who prioritize high-definition content and advanced features. The market for recordable optical discs is also influenced by technological advancements, such as the development of rewritable discs, which allow users to erase and rewrite data multiple times. This feature is particularly useful for data backup and storage, as it provides flexibility and cost-effectiveness. Additionally, the introduction of multi-layer discs has further expanded the storage capacity of optical discs, enabling users to store even larger amounts of data on a single disc. Despite the rise of digital streaming and cloud storage solutions, the Global Recordable Optical Disc Market continues to thrive due to the unique advantages offered by optical discs. These advantages include their physical nature, which provides a tangible backup solution, and their compatibility with a wide range of devices, including computers, DVD players, and gaming consoles. Optical discs also offer a level of data security and longevity that is not always guaranteed with digital storage solutions. As a result, they remain a popular choice for consumers and businesses seeking reliable and durable storage options. The market for recordable optical discs is also supported by the continued demand for physical media in certain regions and industries. For example, in areas with limited internet access or bandwidth, optical discs provide a practical solution for distributing and accessing digital content. Additionally, industries such as education, healthcare, and government rely on optical discs for secure data storage and distribution, further driving the demand for recordable optical discs. As the Global Recordable Optical Disc Market continues to evolve, it adapts to the changing needs of consumers and businesses, ensuring the continued relevance of optical discs in the digital age.

Online Sales, Offline Retail in the Global Recordable Optical Disc Market:

The usage of the Global Recordable Optical Disc Market spans both online sales and offline retail, each offering unique advantages and challenges. Online sales of recordable optical discs have become increasingly popular due to the convenience and accessibility of e-commerce platforms. Consumers can easily browse a wide selection of discs, compare prices, and read reviews from the comfort of their homes. Online retailers often offer competitive pricing and discounts, making it an attractive option for budget-conscious consumers. Additionally, online sales provide access to a global market, allowing consumers to purchase discs that may not be available in their local area. This is particularly beneficial for niche markets, such as collectors of rare or limited edition discs. The rise of online sales has also led to the development of specialized e-commerce platforms dedicated to optical media, catering to specific consumer needs and preferences. However, online sales also present challenges, such as the risk of counterfeit products and the inability to physically inspect the discs before purchase. To address these concerns, consumers are encouraged to purchase from reputable retailers and verify the authenticity of the products. Offline retail, on the other hand, offers a more traditional shopping experience, allowing consumers to physically browse and inspect the discs before making a purchase. This is particularly important for consumers who prioritize the quality and condition of the discs, such as collectors and audiophiles. Offline retail also provides immediate access to the products, eliminating the need for shipping and delivery times associated with online purchases. Additionally, brick-and-mortar stores often offer personalized customer service, with knowledgeable staff available to provide recommendations and assistance. This can be especially beneficial for consumers who are new to optical media or require guidance in selecting the right type of disc for their needs. Despite the convenience of online sales, offline retail remains a popular choice for consumers who value the tactile experience and personalized service offered by physical stores. The Global Recordable Optical Disc Market continues to thrive in both online and offline channels, with each offering unique benefits to consumers. Online sales provide convenience, accessibility, and a wide selection of products, while offline retail offers a tangible shopping experience and personalized customer service. As consumer preferences continue to evolve, the market adapts to meet the changing demands, ensuring the continued relevance of recordable optical discs in both online and offline retail environments.

Global Recordable Optical Disc Market Outlook:

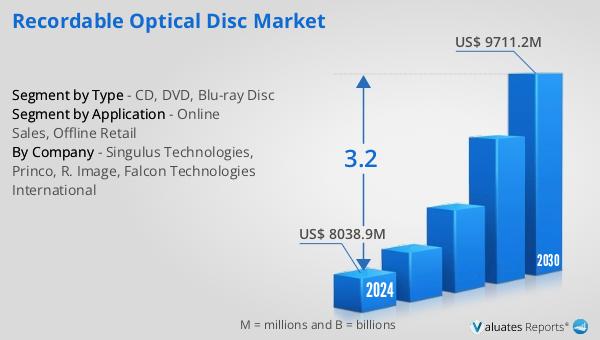

The outlook for the Global Recordable Optical Disc Market indicates a steady growth trajectory over the coming years. The market is expected to expand from a valuation of approximately $8,038.9 million in 2024 to around $9,711.2 million by 2030. This growth is projected to occur at a Compound Annual Growth Rate (CAGR) of 3.2% during the forecast period. This positive outlook reflects the ongoing demand for optical discs across various sectors, despite the increasing popularity of digital storage solutions. The market's growth can be attributed to several factors, including the continued use of optical discs for data storage, entertainment, and archival purposes. Optical discs offer a reliable and durable storage solution, making them a preferred choice for consumers and businesses seeking to preserve important data and media. Additionally, the market benefits from the ongoing demand for physical media in regions with limited internet access or bandwidth, where optical discs provide a practical solution for distributing and accessing digital content. The Global Recordable Optical Disc Market also continues to innovate, with advancements in disc technology and storage capacity driving consumer interest. As the market evolves, it adapts to the changing needs of consumers and businesses, ensuring the continued relevance of optical discs in the digital age. This steady growth trajectory highlights the enduring appeal of optical discs as a versatile and reliable storage medium, capable of meeting the diverse needs of consumers and businesses worldwide.

| Report Metric | Details |

| Report Name | Recordable Optical Disc Market |

| Accounted market size in 2024 | US$ 8038.9 million |

| Forecasted market size in 2030 | US$ 9711.2 million |

| CAGR | 3.2 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Singulus Technologies, Princo, R. Image, Falcon Technologies International |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |