What is Slurry Blending and Distribution System - Global Market?

Slurry Blending and Distribution Systems are integral components in various industrial processes, particularly in sectors like semiconductor manufacturing, mining, and construction. These systems are designed to mix and distribute slurry, which is a semi-liquid mixture typically composed of fine particles suspended in a liquid. The global market for these systems is driven by the increasing demand for efficient and precise slurry handling solutions. As industries continue to evolve, the need for advanced slurry blending and distribution systems has become more pronounced. These systems ensure that the slurry is consistently mixed and delivered to the required locations, maintaining the desired properties and performance. The market is characterized by technological advancements, with manufacturers focusing on developing systems that offer enhanced precision, reliability, and ease of operation. Additionally, the growing emphasis on sustainability and environmental compliance is pushing companies to adopt systems that minimize waste and energy consumption. As a result, the slurry blending and distribution system market is poised for significant growth, driven by the need for efficient and sustainable solutions in various industrial applications.

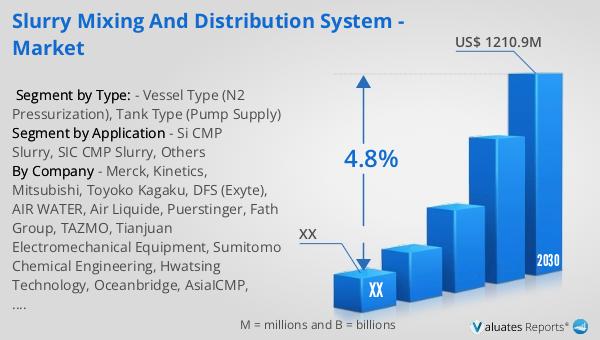

Vessel Type (N2 Pressurization), Tank Type (Pump Supply) in the Slurry Blending and Distribution System - Global Market:

In the realm of slurry blending and distribution systems, two primary configurations are often discussed: Vessel Type (N2 Pressurization) and Tank Type (Pump Supply). The Vessel Type system, which utilizes nitrogen (N2) pressurization, is designed to maintain a consistent pressure within the vessel, ensuring that the slurry is evenly distributed. This method is particularly advantageous in applications where precise control over slurry flow is required. By using nitrogen, a stable and inert gas, the system minimizes the risk of contamination and oxidation, which is crucial in sensitive processes such as semiconductor manufacturing. The pressurization ensures that the slurry is delivered at a consistent rate, reducing the likelihood of blockages and ensuring uniformity in the end product. On the other hand, the Tank Type system relies on pump supply to move the slurry from the storage tank to the point of use. This configuration is often favored in applications where large volumes of slurry need to be handled. The pump system can be tailored to accommodate different flow rates and pressures, making it versatile for various industrial needs. One of the key benefits of the Tank Type system is its ability to handle slurries with varying viscosities and particle sizes, providing flexibility in processing different materials. Both systems have their unique advantages and are chosen based on the specific requirements of the application. The choice between Vessel Type and Tank Type systems often depends on factors such as the nature of the slurry, the required flow rate, and the sensitivity of the process. As industries continue to demand more efficient and reliable slurry handling solutions, manufacturers are investing in research and development to enhance the capabilities of both Vessel Type and Tank Type systems. This includes the integration of advanced sensors and control systems to monitor and adjust the slurry flow in real-time, ensuring optimal performance. Furthermore, the push towards automation and digitalization in industrial processes is driving the development of smart slurry blending and distribution systems that can be remotely monitored and controlled. This not only improves efficiency but also reduces the need for manual intervention, minimizing the risk of human error. As the global market for slurry blending and distribution systems continues to grow, the demand for both Vessel Type and Tank Type configurations is expected to rise, driven by the need for precise, efficient, and sustainable slurry handling solutions.

Si CMP Slurry, SIC CMP Slurry, Others in the Slurry Blending and Distribution System - Global Market:

The application of slurry blending and distribution systems in the global market spans several key areas, including Si CMP Slurry, SiC CMP Slurry, and other specialized slurries. In the semiconductor industry, Si CMP (Chemical Mechanical Planarization) slurry is a critical component used in the planarization process of silicon wafers. The precision required in this process necessitates the use of advanced slurry blending and distribution systems to ensure uniformity and consistency in the slurry composition. These systems help in maintaining the desired particle size distribution and chemical composition, which are crucial for achieving the required surface finish and planarity. Similarly, SiC CMP slurry is used in the planarization of silicon carbide wafers, which are increasingly being used in high-power and high-frequency electronic devices. The unique properties of silicon carbide, such as its hardness and thermal conductivity, require specialized slurry formulations and precise handling to achieve the desired results. Slurry blending and distribution systems play a vital role in ensuring that the SiC CMP slurry is delivered with the necessary precision and consistency, minimizing defects and improving the overall yield. Beyond the semiconductor industry, slurry blending and distribution systems are also used in other applications, such as in the production of advanced ceramics, battery materials, and specialty chemicals. In these areas, the ability to precisely control the slurry composition and flow is essential for achieving the desired material properties and performance. For instance, in the production of advanced ceramics, the slurry must be carefully blended to ensure uniform particle distribution and prevent agglomeration, which can affect the final product's strength and durability. Similarly, in battery manufacturing, the slurry used in electrode production must be precisely controlled to ensure optimal performance and longevity. The versatility and precision offered by modern slurry blending and distribution systems make them indispensable tools in these and other applications, driving their adoption across various industries. As the demand for high-performance materials continues to grow, the role of slurry blending and distribution systems in ensuring quality and efficiency is becoming increasingly important.

Slurry Blending and Distribution System - Global Market Outlook:

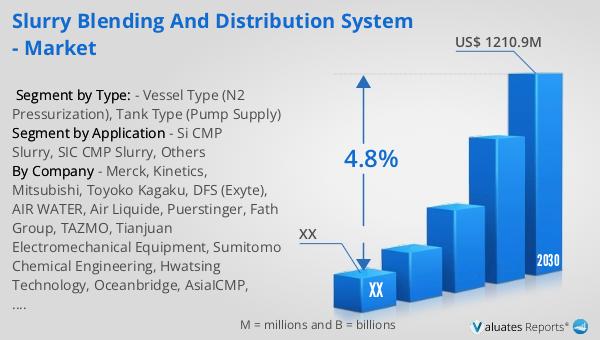

The global market for slurry blending and distribution systems was valued at approximately $848 million in 2023. This market is projected to grow significantly, reaching an estimated size of $1,210.9 million by 2030. This growth represents a compound annual growth rate (CAGR) of 4.8% during the forecast period from 2024 to 2030. The increasing demand for efficient and precise slurry handling solutions across various industries is a key driver of this market growth. As industries continue to evolve and adopt more advanced technologies, the need for reliable and sustainable slurry blending and distribution systems is becoming more pronounced. These systems are essential for ensuring the consistent and precise delivery of slurry, which is critical for maintaining the desired properties and performance in various applications. The market is also being driven by the growing emphasis on sustainability and environmental compliance, as companies seek to minimize waste and energy consumption in their operations. As a result, manufacturers are focusing on developing systems that offer enhanced precision, reliability, and ease of operation, while also reducing their environmental impact. This focus on innovation and sustainability is expected to drive the continued growth of the slurry blending and distribution system market in the coming years.

| Report Metric | Details |

| Report Name | Slurry Blending and Distribution System - Market |

| Forecasted market size in 2030 | US$ 1210.9 million |

| CAGR | 4.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Merck, Kinetics, Mitsubishi, Toyoko Kagaku, DFS (Exyte), AIR WATER, Air Liquide, Puerstinger, Fath Group, TAZMO, Tianjuan Electromechanical Equipment, Sumitomo Chemical Engineering, Hwatsing Technology, Oceanbridge, AsiaICMP, PLUSENG, Axus Technology, SCREEN SPE Service, PLUS TECH, TRUSVAL TECHNOLOGY, GMC Semitech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |