What is Car Rear Bumper - Global Market?

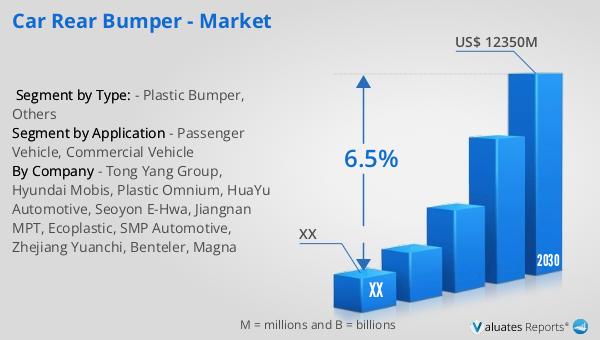

The car rear bumper is an essential component of a vehicle, designed to absorb impact in the event of a collision, thereby protecting the vehicle's rear end and its occupants. The global market for car rear bumpers is a dynamic and evolving sector, driven by the increasing production and sales of automobiles worldwide. As of 2023, the market was valued at approximately US$ 7,858 million, with projections indicating a growth to US$ 12,350 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.5% from 2024 to 2030. This growth is fueled by advancements in automotive technology, increasing consumer demand for enhanced safety features, and stringent government regulations regarding vehicle safety standards. The market is predominantly concentrated in Asia, Europe, and North America, with Asia leading in automobile production, accounting for 56% of the global output. Europe and North America follow, contributing 20% and 16% respectively. This geographical distribution highlights the significant role these regions play in shaping the market dynamics, influenced by factors such as economic growth, urbanization, and technological advancements in the automotive industry. The car rear bumper market is poised for substantial growth, driven by these regional contributions and the continuous evolution of automotive design and safety standards.

Plastic Bumper, Others in the Car Rear Bumper - Global Market:

Plastic bumpers are a significant segment within the car rear bumper market, offering a blend of durability, cost-effectiveness, and design flexibility. These bumpers are typically made from materials such as polypropylene, polycarbonate, and ABS (Acrylonitrile Butadiene Styrene), which provide excellent impact resistance and lightweight properties. The use of plastic bumpers is prevalent due to their ability to absorb minor impacts without significant damage, thus reducing repair costs and enhancing vehicle safety. Additionally, plastic bumpers can be easily molded into various shapes and sizes, allowing for greater design freedom and customization options for automakers. This versatility is particularly appealing in the global market, where consumer preferences and regulatory requirements vary significantly across regions. The demand for plastic bumpers is further driven by the automotive industry's shift towards lightweight materials to improve fuel efficiency and reduce emissions. As environmental concerns continue to rise, manufacturers are increasingly focusing on sustainable production practices, including the use of recycled plastics and eco-friendly materials in bumper manufacturing. This trend aligns with the broader industry movement towards sustainability and green technologies, positioning plastic bumpers as a key component in the future of automotive design. In addition to plastic bumpers, the market also includes other materials such as metal and composite bumpers, each offering unique advantages and applications. Metal bumpers, typically made from steel or aluminum, provide superior strength and durability, making them ideal for heavy-duty vehicles and commercial applications. However, they are generally heavier and more expensive than plastic alternatives, which can impact vehicle performance and cost. Composite bumpers, on the other hand, combine the benefits of both plastic and metal, offering a balance of strength, weight, and cost. These bumpers are often used in high-performance vehicles where weight reduction is critical, and they can be engineered to meet specific performance criteria. The choice of bumper material is influenced by various factors, including vehicle type, intended use, and regional regulations. For instance, in regions with stringent safety standards, manufacturers may opt for composite or metal bumpers to meet crash test requirements. Conversely, in markets where cost and fuel efficiency are prioritized, plastic bumpers may be more prevalent. The global car rear bumper market is characterized by a diverse range of materials and technologies, each catering to different segments and consumer needs. As the automotive industry continues to evolve, the demand for innovative and sustainable bumper solutions is expected to grow, driven by advancements in material science and manufacturing processes. This evolution presents opportunities for manufacturers to differentiate their products and capture market share by offering advanced bumper solutions that meet the changing demands of consumers and regulators alike.

Passenger Vehicle, Commercial Vehicle in the Car Rear Bumper - Global Market:

The usage of car rear bumpers varies significantly between passenger vehicles and commercial vehicles, reflecting the distinct needs and priorities of these segments. In passenger vehicles, rear bumpers primarily serve as a safety feature, designed to protect the vehicle's rear end and its occupants in the event of a collision. They are engineered to absorb impact energy, minimizing damage to the vehicle's structure and reducing the risk of injury to passengers. In addition to safety, aesthetics play a crucial role in the design of rear bumpers for passenger vehicles. Automakers strive to create visually appealing designs that complement the overall look of the vehicle, often incorporating features such as integrated sensors and cameras to enhance functionality and convenience. The demand for advanced safety features and stylish designs is a key driver of innovation in the passenger vehicle segment, with manufacturers continually seeking to improve bumper performance and aesthetics. In contrast, the primary focus for rear bumpers in commercial vehicles is durability and functionality. Commercial vehicles, such as trucks and vans, are often used for transporting goods and materials, requiring robust bumpers that can withstand heavy use and frequent impacts. These bumpers are typically made from stronger materials, such as metal or reinforced composites, to provide the necessary strength and durability. Additionally, commercial vehicle bumpers may include features such as towing hooks and step plates to facilitate loading and unloading operations. The emphasis on functionality and durability in the commercial vehicle segment reflects the practical needs of businesses and fleet operators, who prioritize reliability and cost-effectiveness over aesthetics. Despite these differences, both passenger and commercial vehicle segments are influenced by broader industry trends, such as the shift towards lightweight materials and sustainable manufacturing practices. As environmental concerns continue to shape the automotive industry, manufacturers are increasingly exploring innovative materials and technologies to enhance bumper performance while reducing weight and environmental impact. This trend is evident in both passenger and commercial vehicle segments, with manufacturers seeking to balance safety, functionality, and sustainability in their bumper designs. The global car rear bumper market is thus characterized by a diverse range of products and applications, each tailored to meet the specific needs of different vehicle types and consumer preferences. As the market continues to evolve, the demand for advanced and sustainable bumper solutions is expected to grow, driven by technological advancements and changing regulatory requirements.

Car Rear Bumper - Global Market Outlook:

The global car rear bumper market was valued at approximately US$ 7,858 million in 2023, with projections indicating a growth to US$ 12,350 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.5% from 2024 to 2030. This growth is largely attributed to the increasing production and sales of automobiles worldwide, driven by factors such as economic growth, urbanization, and technological advancements in the automotive industry. Currently, over 90% of the world's automobiles are concentrated in Asia, Europe, and North America, with Asia leading in automobile production, accounting for 56% of the global output. Europe and North America follow, contributing 20% and 16% respectively. This geographical distribution highlights the significant role these regions play in shaping the market dynamics, influenced by factors such as consumer preferences, regulatory requirements, and technological advancements. The market is characterized by a diverse range of materials and technologies, each catering to different segments and consumer needs. As the automotive industry continues to evolve, the demand for innovative and sustainable bumper solutions is expected to grow, driven by advancements in material science and manufacturing processes. This evolution presents opportunities for manufacturers to differentiate their products and capture market share by offering advanced bumper solutions that meet the changing demands of consumers and regulators alike.

| Report Metric | Details |

| Report Name | Car Rear Bumper - Market |

| Forecasted market size in 2030 | US$ 12350 million |

| CAGR | 6.5% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Tong Yang Group, Hyundai Mobis, Plastic Omnium, HuaYu Automotive, Seoyon E-Hwa, Jiangnan MPT, Ecoplastic, SMP Automotive, Zhejiang Yuanchi, Benteler, Magna |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |