What is Medical Operating Microscope - Global Market?

Medical operating microscopes are specialized optical instruments used in various surgical procedures to provide magnified and illuminated views of small and intricate structures within the human body. These microscopes are crucial in enhancing the precision and accuracy of surgeries, allowing surgeons to perform complex procedures with greater confidence and reduced risk of errors. The global market for medical operating microscopes is driven by advancements in healthcare technology, increasing demand for minimally invasive surgeries, and the growing prevalence of chronic diseases that require surgical intervention. These microscopes are widely used in fields such as neurosurgery, ophthalmology, ENT (ear, nose, and throat) surgery, and dentistry, among others. The market is characterized by continuous innovation, with manufacturers focusing on developing microscopes with improved optics, ergonomic designs, and integrated digital imaging systems. As healthcare systems worldwide strive to improve surgical outcomes and patient safety, the demand for high-quality medical operating microscopes is expected to rise, making this market a vital component of the broader medical devices industry.

Neurosurgery Microscope, ENT Surgery Microscope, Others in the Medical Operating Microscope - Global Market:

Neurosurgery microscopes are a critical component in the field of neurosurgery, where precision is paramount. These microscopes provide neurosurgeons with a clear and magnified view of the brain and spinal cord, enabling them to perform delicate procedures with enhanced accuracy. The use of neurosurgery microscopes has revolutionized the way brain tumors, aneurysms, and other neurological conditions are treated. With features such as high magnification, superior illumination, and advanced imaging capabilities, these microscopes allow surgeons to navigate complex anatomical structures with ease. ENT surgery microscopes, on the other hand, are designed to assist surgeons in procedures involving the ear, nose, and throat. These microscopes offer excellent visualization of the intricate structures within the ENT region, facilitating precise surgical interventions. They are commonly used in procedures such as sinus surgeries, cochlear implantations, and vocal cord surgeries. The demand for ENT surgery microscopes is driven by the increasing prevalence of ENT disorders and the growing preference for minimally invasive surgical techniques. In addition to neurosurgery and ENT surgery, medical operating microscopes find applications in various other surgical specialties. For instance, in ophthalmology, these microscopes are used for cataract surgeries, retinal surgeries, and corneal transplants. In dentistry, they aid in procedures such as root canal treatments and periodontal surgeries. The versatility of medical operating microscopes makes them indispensable tools in modern surgical practice. As the global market for medical operating microscopes continues to expand, manufacturers are focusing on developing innovative solutions that cater to the specific needs of different surgical specialties. This includes the integration of digital imaging technologies, ergonomic designs, and enhanced optical systems to improve surgical outcomes and patient safety. The ongoing advancements in medical operating microscopes are expected to drive their adoption across various surgical fields, further fueling the growth of the global market.

Hospital, Clinic, Others in the Medical Operating Microscope - Global Market:

Medical operating microscopes are extensively used in hospitals, clinics, and other healthcare settings to enhance the precision and effectiveness of surgical procedures. In hospitals, these microscopes are integral to the operating rooms, where they are used in a wide range of surgeries, including neurosurgery, ophthalmology, ENT, and orthopedics. The high demand for medical operating microscopes in hospitals is driven by the need for advanced surgical equipment that can improve patient outcomes and reduce the risk of complications. Hospitals invest in state-of-the-art microscopes to ensure that their surgical teams have access to the best tools available, thereby enhancing their ability to perform complex procedures with confidence. In clinics, medical operating microscopes are used in outpatient surgeries and minor procedures that require magnification and illumination. These microscopes are particularly valuable in specialties such as dermatology, dentistry, and gynecology, where precision is crucial. Clinics benefit from the portability and versatility of modern operating microscopes, which can be easily integrated into various clinical settings. The use of medical operating microscopes in clinics allows healthcare providers to offer high-quality care and improve patient satisfaction. Beyond hospitals and clinics, medical operating microscopes are also used in research institutions and educational settings. In research, these microscopes are employed in studies that require detailed visualization of biological structures, contributing to advancements in medical science. In educational institutions, they are used to train medical students and residents, providing them with hands-on experience in surgical techniques. The widespread use of medical operating microscopes across different healthcare settings underscores their importance in modern medicine. As the global market for these microscopes continues to grow, healthcare providers are increasingly recognizing the value of investing in advanced optical technologies to enhance surgical precision and improve patient care.

Medical Operating Microscope - Global Market Outlook:

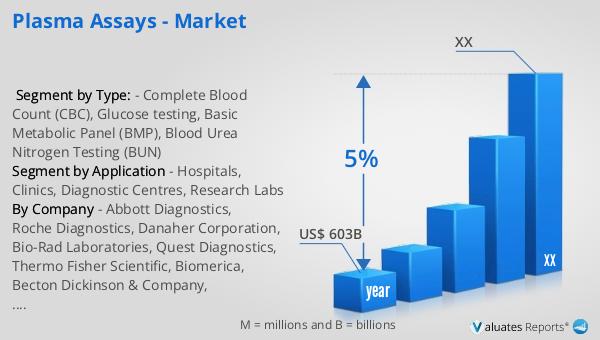

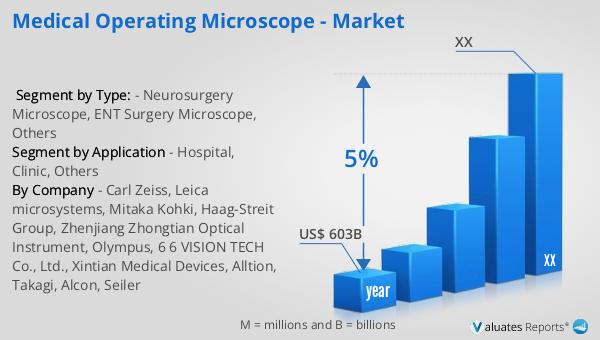

Based on our research, the global market for medical devices, which includes medical operating microscopes, is projected to reach approximately $603 billion in 2023. This market is anticipated to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing demand for advanced medical technologies, the rising prevalence of chronic diseases, and the growing emphasis on improving surgical outcomes. As healthcare systems worldwide continue to evolve, there is a heightened focus on adopting innovative medical devices that can enhance patient care and safety. Medical operating microscopes, with their ability to provide high magnification and illumination, play a crucial role in this landscape by enabling surgeons to perform complex procedures with greater precision. The continuous advancements in optical technologies and the integration of digital imaging systems are expected to further propel the growth of the medical operating microscope market. As a result, healthcare providers are increasingly investing in these advanced tools to improve surgical precision and patient outcomes. The global market outlook for medical operating microscopes is promising, with significant opportunities for growth and innovation in the coming years.

| Report Metric | Details |

| Report Name | Medical Operating Microscope - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Carl Zeiss, Leica microsystems, Mitaka Kohki, Haag-Streit Group, Zhenjiang Zhongtian Optical Instrument, Olympus, 6 6 VISION TECH Co., Ltd., Xintian Medical Devices, Alltion, Takagi, Alcon, Seiler |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |