What is Visitor Identify and Checking System - Global Market?

The Visitor Identify and Checking System (VICS) is a sophisticated technology designed to enhance security and streamline the process of identifying and verifying individuals in various settings. This system is crucial in environments where monitoring and controlling access is essential, such as airports, hotels, government agencies, and other high-security areas. VICS employs a combination of advanced technologies, including biometric recognition, radio frequency identification (RFID), and other identification methods, to accurately verify the identity of visitors. By integrating these technologies, VICS ensures that only authorized individuals gain access to restricted areas, thereby enhancing security and reducing the risk of unauthorized entry. The global market for VICS is expanding as organizations increasingly recognize the importance of robust security measures in protecting sensitive information and assets. As technology continues to evolve, VICS is expected to incorporate even more advanced features, further improving its effectiveness and reliability. The demand for VICS is driven by the growing need for enhanced security solutions across various sectors, making it a vital component of modern security infrastructure.

Radio Frequency Identification, Fingerprint Biometric, Other in the Visitor Identify and Checking System - Global Market:

Radio Frequency Identification (RFID) is a key component of the Visitor Identify and Checking System, offering a seamless and efficient way to track and manage visitor access. RFID technology uses electromagnetic fields to automatically identify and track tags attached to objects or individuals. In the context of VICS, RFID tags can be embedded in visitor badges or cards, allowing for quick and contactless identification as visitors enter or exit a facility. This technology is particularly useful in high-traffic areas where speed and efficiency are paramount. By using RFID, organizations can maintain a real-time log of visitor movements, enhancing security and providing valuable data for analysis. Fingerprint biometric technology is another critical element of VICS, providing a highly secure method of verifying an individual's identity. Fingerprint recognition systems capture and store the unique patterns of an individual's fingerprints, allowing for quick and accurate identification. This technology is widely regarded as one of the most reliable forms of biometric identification, as fingerprints are unique to each individual and difficult to replicate. In VICS, fingerprint biometrics can be used to grant or deny access to secure areas, ensuring that only authorized personnel can enter. Other identification methods used in VICS include facial recognition, iris scanning, and voice recognition. These technologies offer additional layers of security by analyzing unique physical or behavioral characteristics of individuals. Facial recognition systems, for example, use algorithms to compare captured images with stored data, allowing for quick and accurate identification. Iris scanning analyzes the unique patterns in the colored part of the eye, while voice recognition systems analyze vocal characteristics to verify identity. Each of these technologies has its own strengths and can be used in combination to create a comprehensive and robust visitor identification system. The integration of these technologies in VICS not only enhances security but also improves the overall visitor experience by reducing wait times and streamlining the check-in process. As the global market for VICS continues to grow, the adoption of these advanced identification technologies is expected to increase, driven by the need for more secure and efficient visitor management solutions.

Airport, Hotel, Station, Government Agency, Other in the Visitor Identify and Checking System - Global Market:

The usage of Visitor Identify and Checking System in airports is crucial for maintaining high levels of security and efficiency. Airports are bustling hubs of activity, with thousands of passengers passing through each day. VICS helps streamline the process of identifying and verifying passengers, ensuring that only authorized individuals gain access to secure areas. By using technologies such as RFID and biometric recognition, airports can quickly and accurately verify the identity of passengers, reducing wait times and enhancing the overall travel experience. In hotels, VICS plays a vital role in ensuring the safety and security of guests and staff. By implementing a robust visitor identification system, hotels can monitor and control access to guest rooms and other restricted areas, preventing unauthorized entry and enhancing the overall security of the premises. VICS also allows hotels to maintain a detailed log of visitor movements, providing valuable data for security and operational purposes. At train stations, VICS is used to manage the flow of passengers and ensure that only ticketed individuals gain access to platforms and trains. By using technologies such as RFID and biometric recognition, stations can quickly and efficiently verify the identity of passengers, reducing congestion and improving the overall travel experience. In government agencies, VICS is essential for protecting sensitive information and ensuring that only authorized personnel gain access to secure areas. By implementing a comprehensive visitor identification system, agencies can enhance security and prevent unauthorized access to confidential data. VICS also allows agencies to maintain a detailed log of visitor movements, providing valuable data for security and operational purposes. Other areas where VICS is used include corporate offices, educational institutions, and healthcare facilities. In these settings, VICS helps ensure the safety and security of employees, students, and patients by monitoring and controlling access to restricted areas. By using advanced identification technologies, organizations can enhance security, improve operational efficiency, and provide a better overall experience for visitors. As the global market for VICS continues to grow, the adoption of these systems is expected to increase across various sectors, driven by the need for enhanced security and efficient visitor management solutions.

Visitor Identify and Checking System - Global Market Outlook:

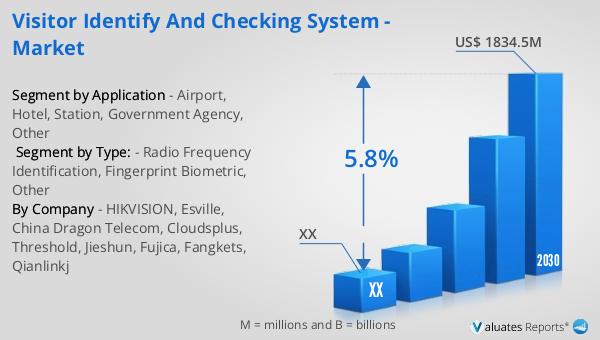

The global market for Visitor Identify and Checking System was valued at approximately US$ 1269 million in 2023. It is projected to grow to a revised size of US$ 1834.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced security solutions across various sectors. The North American market for Visitor Identify and Checking System was also valued at a significant amount in 2023, with expectations of continued growth through 2030. The CAGR for this region during the forecast period is anticipated to be robust, reflecting the region's strong focus on security and technological advancements. As organizations in North America and globally continue to prioritize security and efficiency, the adoption of Visitor Identify and Checking Systems is expected to rise. This growth is driven by the need to protect sensitive information, enhance operational efficiency, and provide a seamless experience for visitors. The market outlook for Visitor Identify and Checking Systems is positive, with continued advancements in technology expected to further drive growth and adoption across various sectors.

| Report Metric | Details |

| Report Name | Visitor Identify and Checking System - Market |

| Forecasted market size in 2030 | US$ 1834.5 million |

| CAGR | 5.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | HIKVISION, Esville, China Dragon Telecom, Cloudsplus, Threshold, Jieshun, Fujica, Fangkets, Qianlinkj |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |