What is Rectilinear Combing Machine - Global Market?

The Rectilinear Combing Machine is a specialized piece of equipment used in the textile industry to enhance the quality of fibers by aligning them in a parallel fashion. This machine plays a crucial role in the preparation of fibers for spinning, ensuring that the final yarn is smooth and free from impurities. The global market for Rectilinear Combing Machines is witnessing significant growth due to the increasing demand for high-quality textiles. As of 2023, the market was valued at approximately US$ 41 million, with projections indicating a rise to US$ 59 million by 2030. This growth is driven by advancements in textile manufacturing technologies and the rising demand for premium textile products. The machine's ability to improve fiber quality makes it indispensable in the production of fine yarns, which are essential for high-end fabrics. The market's expansion is also supported by the growing textile industries in emerging economies, where there is a shift towards modernizing production facilities to meet international standards. As the demand for superior textile products continues to rise, the Rectilinear Combing Machine market is expected to maintain its upward trajectory, driven by technological innovations and the increasing emphasis on quality in the textile sector.

Front Swing Type, Back Swing Type, Others in the Rectilinear Combing Machine - Global Market:

Rectilinear Combing Machines are categorized into different types based on their operational mechanisms, with the Front Swing Type, Back Swing Type, and Others being the primary classifications. The Front Swing Type Rectilinear Combing Machine is designed to handle fibers with a forward motion, which helps in efficiently aligning the fibers and removing short fibers and impurities. This type is particularly favored in industries where precision and high-quality output are paramount. The forward motion ensures that the fibers are combed thoroughly, resulting in a smoother and more uniform yarn. On the other hand, the Back Swing Type operates with a backward motion, which is beneficial in certain textile processes where a different fiber alignment is required. This type is often used in applications where the fiber characteristics demand a unique combing approach to achieve the desired texture and quality. The Back Swing Type is known for its versatility and ability to handle a wide range of fiber types, making it a popular choice in diverse textile applications. Apart from these, there are other types of Rectilinear Combing Machines that cater to specific needs within the textile industry. These machines are designed to address unique challenges in fiber processing, offering customized solutions for different textile products. The "Others" category includes machines that incorporate advanced technologies and innovative features to enhance efficiency and output quality. These machines are often used in specialized textile applications where standard combing machines may not suffice. The global market for these machines is driven by the continuous evolution of textile manufacturing processes and the need for machines that can adapt to changing industry demands. As textile manufacturers strive to produce high-quality products, the demand for advanced Rectilinear Combing Machines is expected to grow, with each type offering distinct advantages that cater to specific production requirements. The choice between Front Swing, Back Swing, and other types of Rectilinear Combing Machines depends largely on the specific needs of the textile operation, the type of fibers being processed, and the desired characteristics of the final product. As the textile industry continues to evolve, these machines will play a pivotal role in ensuring that manufacturers can meet the increasing demand for high-quality textiles while maintaining efficiency and cost-effectiveness in their operations.

Cotton Textile Industry, Woolen Textile Industry, Others in the Rectilinear Combing Machine - Global Market:

The Rectilinear Combing Machine is extensively used in various sectors of the textile industry, including the Cotton Textile Industry, Woolen Textile Industry, and other specialized areas. In the Cotton Textile Industry, these machines are crucial for producing high-quality cotton yarns. The combing process removes short fibers and impurities, resulting in a smoother and stronger yarn that is ideal for producing fine cotton fabrics. This is particularly important in the production of luxury cotton products, where the quality of the yarn directly impacts the feel and durability of the final fabric. The use of Rectilinear Combing Machines in this sector is driven by the demand for premium cotton textiles, which require superior yarn quality. In the Woolen Textile Industry, Rectilinear Combing Machines are used to process wool fibers, ensuring that they are aligned and free from impurities. This is essential for producing high-quality woolen yarns that are used in a variety of applications, from clothing to home textiles. The combing process enhances the strength and uniformity of the wool fibers, resulting in a yarn that is both durable and aesthetically pleasing. The demand for high-quality woolen products is a key driver for the use of these machines in the woolen textile sector. Beyond cotton and wool, Rectilinear Combing Machines are also used in other areas of the textile industry, where they play a vital role in processing various types of fibers. These machines are adaptable to different fiber types, making them a versatile tool in the production of diverse textile products. Whether it's synthetic fibers, blends, or other natural fibers, the combing process ensures that the fibers are prepared to the highest standards, ready for spinning into yarn. The versatility of Rectilinear Combing Machines makes them an indispensable asset in the textile industry, where the demand for high-quality, diverse textile products continues to grow. As the industry evolves, these machines will remain a critical component in the production process, ensuring that manufacturers can meet the ever-increasing quality standards and consumer expectations.

Rectilinear Combing Machine - Global Market Outlook:

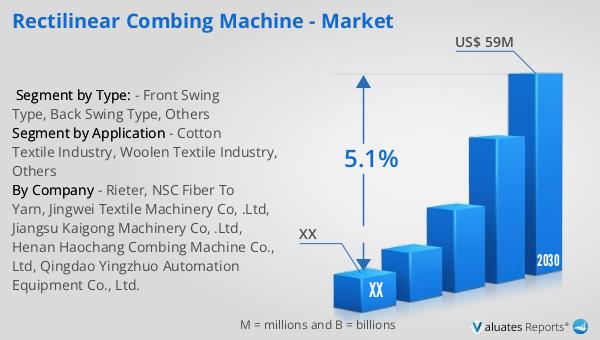

The global market for Rectilinear Combing Machines was valued at approximately US$ 41 million in 2023, with expectations to reach a revised size of US$ 59 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.1% during the forecast period from 2024 to 2030. This growth trajectory highlights the increasing demand for these machines, driven by advancements in textile manufacturing and the rising need for high-quality textile products. In North America, the market for Rectilinear Combing Machines was valued at a significant amount in 2023, with projections indicating continued growth through 2030. The region's market dynamics are influenced by the modernization of textile production facilities and the emphasis on producing superior textile products. The anticipated growth in the North American market underscores the importance of Rectilinear Combing Machines in enhancing the quality and efficiency of textile manufacturing processes. As the global textile industry continues to evolve, the demand for advanced combing machines is expected to rise, driven by the need for high-quality yarns and fabrics that meet international standards. The market outlook for Rectilinear Combing Machines reflects the broader trends in the textile industry, where innovation and quality are key drivers of growth.

| Report Metric | Details |

| Report Name | Rectilinear Combing Machine - Market |

| Forecasted market size in 2030 | US$ 59 million |

| CAGR | 5.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Rieter, NSC Fiber To Yarn, Jingwei Textile Machinery Co, .Ltd, Jiangsu Kaigong Machinery Co, .Ltd, Henan Haochang Combing Machine Co., Ltd, Qingdao Yingzhuo Automation Equipment Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |