What is Surface Inspection System Based on Smart Camera - Global Market?

Surface Inspection Systems based on smart cameras are revolutionizing the global market by offering advanced solutions for quality control and defect detection across various industries. These systems utilize smart cameras equipped with sophisticated imaging technologies to inspect surfaces for defects, irregularities, or inconsistencies. The smart cameras are integrated with powerful processors and algorithms that enable real-time analysis and decision-making. This technology is particularly beneficial in manufacturing environments where precision and speed are crucial. By automating the inspection process, these systems reduce human error, increase efficiency, and ensure consistent product quality. The global market for these systems is expanding as industries recognize the value of integrating smart camera-based surface inspection into their production lines. The demand is driven by the need for high-quality products, stringent regulatory standards, and the push towards automation in manufacturing processes. As a result, industries such as automotive, electronics, pharmaceuticals, and food processing are increasingly adopting these systems to enhance their quality assurance processes. The versatility and adaptability of smart camera-based systems make them suitable for a wide range of applications, further fueling their market growth. With continuous advancements in camera technology and image processing algorithms, the capabilities of these systems are expected to expand, offering even more precise and efficient inspection solutions.

3D Surface Inspection System, 2D Surface Inspection System in the Surface Inspection System Based on Smart Camera - Global Market:

The 3D Surface Inspection System and 2D Surface Inspection System are two primary types of surface inspection technologies based on smart cameras, each offering unique advantages and applications in the global market. The 3D Surface Inspection System utilizes three-dimensional imaging to capture detailed surface profiles, allowing for the detection of complex surface defects such as dents, scratches, and texture variations. This system is particularly useful in industries where surface integrity is critical, such as automotive and aerospace, where even minor defects can impact performance and safety. The 3D system's ability to provide depth information enables it to detect defects that may not be visible with traditional 2D inspection methods. On the other hand, the 2D Surface Inspection System relies on two-dimensional imaging to identify surface defects. It is widely used in industries where surface appearance is crucial, such as electronics and packaging. The 2D system is effective in detecting surface anomalies like color variations, stains, and surface finish inconsistencies. Both systems leverage smart camera technology, which integrates advanced image processing algorithms and machine learning capabilities to enhance defect detection accuracy and speed. The choice between 3D and 2D systems depends on the specific requirements of the application, such as the type of defects to be detected, the material being inspected, and the desired inspection speed. In the global market, the adoption of these systems is driven by the increasing demand for high-quality products and the need to comply with stringent quality standards. As industries continue to automate their production processes, the integration of smart camera-based surface inspection systems is becoming a critical component of quality assurance strategies. The versatility of these systems allows them to be customized for various applications, making them an attractive option for manufacturers looking to enhance their inspection capabilities. Furthermore, advancements in camera technology and image processing are continuously improving the performance of these systems, enabling them to handle more complex inspection tasks with greater accuracy and efficiency. As a result, the global market for 3D and 2D Surface Inspection Systems based on smart cameras is poised for significant growth, driven by the increasing emphasis on quality control and the adoption of automation in manufacturing processes.

Automotive, Electrical & Electronics, Food & Pharmaceutical, Others in the Surface Inspection System Based on Smart Camera - Global Market:

Surface Inspection Systems based on smart cameras are extensively used across various industries, including automotive, electrical and electronics, food and pharmaceutical, and others, to ensure product quality and compliance with industry standards. In the automotive industry, these systems are employed to inspect components such as body panels, engine parts, and interior trims for defects like scratches, dents, and surface irregularities. The ability to detect such defects early in the production process helps manufacturers reduce waste, improve product quality, and enhance customer satisfaction. In the electrical and electronics industry, surface inspection systems are used to examine printed circuit boards (PCBs), semiconductor wafers, and electronic components for defects such as soldering errors, surface contamination, and alignment issues. The precision and speed of smart camera-based systems enable manufacturers to maintain high-quality standards and reduce the risk of product failures. In the food and pharmaceutical industries, surface inspection systems are utilized to ensure the quality and safety of products by detecting defects such as packaging errors, labeling issues, and surface contamination. These systems help manufacturers comply with stringent regulatory requirements and maintain consumer trust. Additionally, surface inspection systems are used in other industries such as textiles, packaging, and consumer goods to inspect products for surface defects and ensure consistent quality. The versatility and adaptability of smart camera-based systems make them suitable for a wide range of applications, allowing manufacturers to customize the inspection process to meet specific requirements. As industries continue to prioritize quality control and automation, the adoption of surface inspection systems based on smart cameras is expected to increase, driving market growth and innovation.

Surface Inspection System Based on Smart Camera - Global Market Outlook:

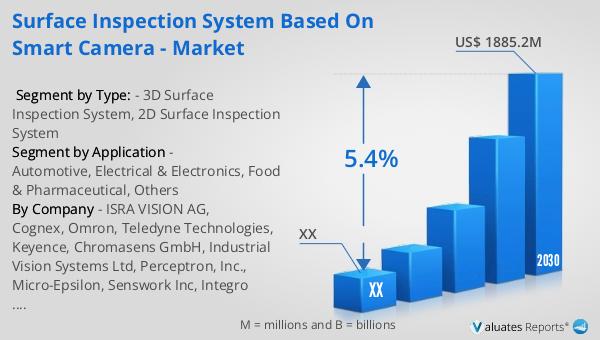

The global market for Surface Inspection Systems based on smart cameras was valued at approximately $1,298 million in 2023. It is projected to grow to a revised size of around $1,885.2 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.4% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced inspection solutions across various industries. In North America, the market for these systems was valued at a significant amount in 2023, with expectations of continued growth through 2030. The CAGR for the North American market during the forecast period is anticipated to align with global trends, driven by the region's strong focus on quality control and automation in manufacturing processes. The adoption of smart camera-based surface inspection systems in North America is fueled by the need for high-quality products, compliance with regulatory standards, and the push towards Industry 4.0. As industries in the region continue to embrace automation and advanced technologies, the demand for efficient and accurate inspection solutions is expected to rise, contributing to the market's growth. The versatility and adaptability of these systems make them an attractive option for manufacturers looking to enhance their quality assurance processes and remain competitive in the global market.

| Report Metric | Details |

| Report Name | Surface Inspection System Based on Smart Camera - Market |

| Forecasted market size in 2030 | US$ 1885.2 million |

| CAGR | 5.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | ISRA VISION AG, Cognex, Omron, Teledyne Technologies, Keyence, Chromasens GmbH, Industrial Vision Systems Ltd, Perceptron, Inc., Micro-Epsilon, Senswork Inc, Integro Technologies, Vantage Corporation, SLR Engineering GmbH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |