What is Hyperspectral Imaging for Environmental Monitoring - Global Market?

Hyperspectral imaging is a cutting-edge technology used in environmental monitoring to capture and analyze a wide spectrum of light beyond what the human eye can see. Unlike traditional imaging, which captures images in three primary colors (red, green, and blue), hyperspectral imaging collects data across numerous spectral bands. This allows for the identification and analysis of materials based on their spectral signatures. In environmental monitoring, this technology is invaluable as it can detect subtle changes in the environment, such as variations in vegetation health, water quality, and soil composition. By providing detailed information about the chemical and physical properties of objects, hyperspectral imaging helps scientists and researchers monitor and manage natural resources more effectively. The global market for hyperspectral imaging in environmental monitoring is growing as more industries recognize its potential to provide precise and comprehensive data for sustainable environmental management.

Visible + Near Infrared Light, Short-Wavelength Infrared, Others in the Hyperspectral Imaging for Environmental Monitoring - Global Market:

Hyperspectral imaging technology operates across various segments of the electromagnetic spectrum, each offering unique insights for environmental monitoring. The visible and near-infrared (VNIR) range, spanning approximately 400 to 1000 nanometers, is particularly useful for assessing vegetation health and land cover. This range captures the light reflected by plants, allowing for the analysis of chlorophyll content and plant stress levels. By monitoring these factors, researchers can assess the impact of environmental changes on ecosystems and agricultural productivity. The short-wavelength infrared (SWIR) range, covering wavelengths from about 1000 to 2500 nanometers, provides additional information on soil and mineral composition. SWIR is sensitive to moisture content and can detect variations in soil properties, making it valuable for soil pollution monitoring and land degradation assessments. Beyond VNIR and SWIR, hyperspectral imaging can also extend into other spectral regions, such as the mid-wave infrared (MWIR) and long-wave infrared (LWIR). These ranges are particularly effective for detecting thermal emissions and identifying chemical compounds, which can be crucial for monitoring industrial pollution and assessing air quality. By leveraging the full spectrum of hyperspectral imaging, environmental scientists can gain a comprehensive understanding of the Earth's surface and atmosphere, enabling more informed decision-making for environmental protection and resource management.

Water Pollution Monitoring, Soil Pollution Monitoring, Other in the Hyperspectral Imaging for Environmental Monitoring - Global Market:

Hyperspectral imaging is increasingly being used for environmental monitoring, particularly in areas such as water pollution monitoring, soil pollution monitoring, and other environmental assessments. In water pollution monitoring, hyperspectral imaging can detect and quantify pollutants such as algae blooms, oil spills, and chemical contaminants. By analyzing the spectral signatures of water bodies, researchers can identify changes in water quality and track the spread of pollutants over time. This information is crucial for managing water resources and ensuring the safety of drinking water supplies. In soil pollution monitoring, hyperspectral imaging can identify contaminated areas by detecting changes in soil composition and moisture content. This technology can help pinpoint sources of pollution, such as industrial waste or agricultural runoff, and assess the effectiveness of remediation efforts. Additionally, hyperspectral imaging can be used for other environmental monitoring applications, such as assessing air quality and detecting deforestation. By providing detailed information about the chemical and physical properties of the environment, hyperspectral imaging enables more effective monitoring and management of natural resources. As the global market for hyperspectral imaging continues to grow, its applications in environmental monitoring are expected to expand, providing valuable insights for sustainable development and environmental protection.

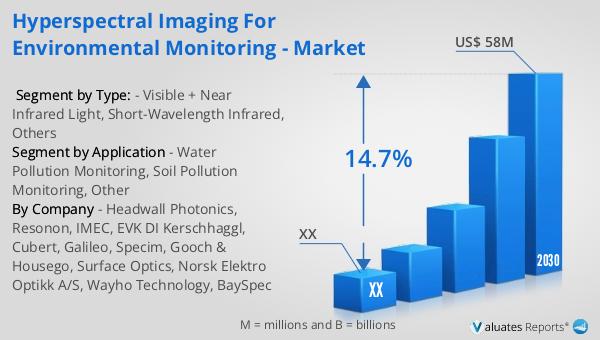

Hyperspectral Imaging for Environmental Monitoring - Global Market Outlook:

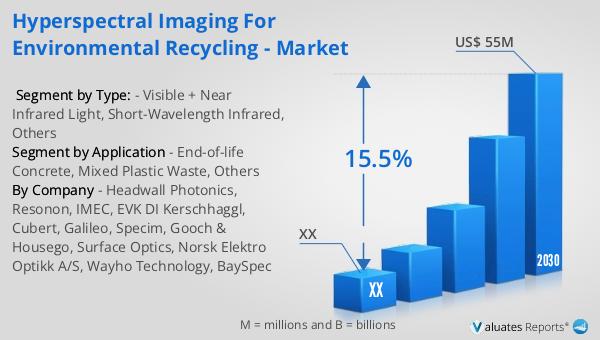

The global market for hyperspectral imaging in environmental monitoring was valued at approximately $23 million in 2023. This market is projected to grow significantly, reaching an estimated $58 million by 2030, with a compound annual growth rate (CAGR) of 14.7% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for precise and comprehensive environmental data, as well as advancements in hyperspectral imaging technology. In North America, the market for hyperspectral imaging in environmental monitoring is also expected to expand, although specific figures for this region were not provided. The adoption of hyperspectral imaging in environmental monitoring is being fueled by the need for more accurate and efficient methods of assessing environmental changes and managing natural resources. As industries and governments recognize the value of hyperspectral imaging for environmental monitoring, the market is poised for continued growth and innovation. This technology offers the potential to revolutionize the way we monitor and protect the environment, providing critical insights for sustainable development and resource management.

| Report Metric | Details |

| Report Name | Hyperspectral Imaging for Environmental Monitoring - Market |

| Forecasted market size in 2030 | US$ 58 million |

| CAGR | 14.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Headwall Photonics, Resonon, IMEC, EVK DI Kerschhaggl, Cubert, Galileo, Specim, Gooch & Housego, Surface Optics, Norsk Elektro Optikk A/S, Wayho Technology, BaySpec |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |