What is Shape Memory Polymer (SMP) - Global Market?

Shape Memory Polymers (SMPs) are a fascinating class of materials that have the unique ability to return to a pre-defined shape when exposed to a specific stimulus, such as heat, light, or a magnetic field. These polymers are engineered to "remember" their original form, which allows them to be deformed and then revert back to their initial shape. This remarkable property makes SMPs highly valuable in various industries, including biomedical, automotive, aerospace, and textiles. The global market for SMPs is expanding rapidly due to their versatility and the growing demand for smart materials. As industries continue to innovate and seek materials that offer both functionality and adaptability, SMPs are becoming increasingly integral. Their applications range from medical devices that can change shape within the human body to automotive components that enhance vehicle performance and safety. The ability of SMPs to respond to environmental changes makes them a key player in the development of next-generation technologies. As research and development in this field advance, the potential for SMPs to revolutionize various sectors becomes more apparent, driving their global market growth.

Polyurethane (PU), Polyvinyl chloride (PVC), Acrylic, Epoxy, Other in the Shape Memory Polymer (SMP) - Global Market:

Shape Memory Polymers (SMPs) are categorized into several types based on their chemical composition, including Polyurethane (PU), Polyvinyl Chloride (PVC), Acrylic, Epoxy, and others. Each type of SMP offers distinct properties that make them suitable for specific applications. Polyurethane-based SMPs are known for their excellent elasticity and toughness, making them ideal for applications that require flexibility and durability. They are widely used in the automotive and textile industries, where materials need to withstand repeated deformation and stress. Polyvinyl Chloride (PVC) SMPs, on the other hand, are valued for their chemical resistance and ease of processing. These properties make PVC SMPs suitable for applications in harsh environments, such as in the construction and chemical industries. Acrylic SMPs are appreciated for their clarity and UV resistance, making them suitable for optical applications and outdoor use. They are often used in the production of lenses and protective coatings. Epoxy-based SMPs are known for their strong adhesive properties and high thermal stability, which make them ideal for aerospace and electronics applications where materials are exposed to extreme temperatures and require strong bonding capabilities. Other SMPs, which include a variety of specialized polymers, are developed to meet specific industry needs, such as biodegradable SMPs for environmentally friendly applications or electrically conductive SMPs for use in smart textiles and electronics. The diversity in SMP types allows for a wide range of applications, each tailored to the unique demands of different industries. As the global market for SMPs continues to grow, the development of new polymer formulations and the enhancement of existing ones are expected to drive further innovation and adoption across various sectors. The versatility of SMPs, combined with their ability to respond to external stimuli, positions them as a key material in the advancement of smart technologies and sustainable solutions.

Biomedical, Automotive, Aerospace, Textile, Others in the Shape Memory Polymer (SMP) - Global Market:

Shape Memory Polymers (SMPs) are finding increasing use across a variety of industries due to their unique ability to change shape in response to external stimuli. In the biomedical field, SMPs are revolutionizing medical devices and treatments. They are used in stents, sutures, and drug delivery systems, where their ability to change shape can improve patient outcomes and reduce the need for invasive procedures. For example, SMP-based stents can be inserted in a compact form and then expand to support blood vessels once inside the body. In the automotive industry, SMPs are used to create components that can adapt to changing conditions, such as temperature fluctuations or mechanical stress. This adaptability can enhance vehicle performance, safety, and fuel efficiency. In the aerospace sector, SMPs are employed in the development of lightweight, morphing structures that can improve aircraft aerodynamics and reduce fuel consumption. Their ability to withstand extreme temperatures and pressures makes them ideal for use in space exploration and satellite technology. In the textile industry, SMPs are used to create smart fabrics that can change their properties, such as color or texture, in response to environmental changes. This innovation is leading to the development of clothing that can adapt to different weather conditions or provide enhanced comfort and functionality. Beyond these industries, SMPs are also being explored for use in robotics, electronics, and construction, where their unique properties can lead to the development of new, innovative products and solutions. The versatility and adaptability of SMPs make them a valuable material in the pursuit of advanced technologies and sustainable practices across a wide range of applications.

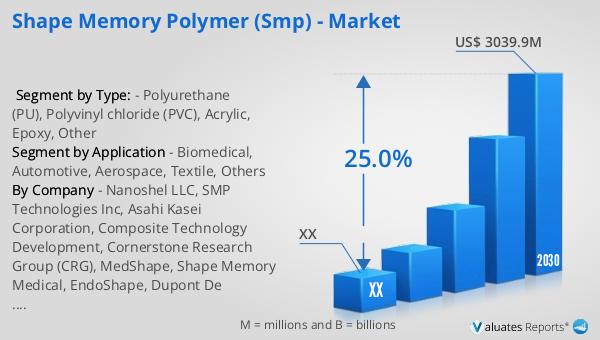

Shape Memory Polymer (SMP) - Global Market Outlook:

The global market for Shape Memory Polymers (SMPs) was valued at approximately $656.4 million in 2023. This market is projected to grow significantly, reaching an estimated size of $3,039.9 million by 2030, with a compound annual growth rate (CAGR) of 25.0% during the forecast period from 2024 to 2030. This impressive growth is driven by the increasing demand for smart materials across various industries, including biomedical, automotive, aerospace, and textiles. In North America, the SMP market is also expected to experience substantial growth, although specific figures for this region were not provided. The rapid expansion of the SMP market can be attributed to the material's unique properties, which allow it to change shape in response to external stimuli, making it highly versatile and suitable for a wide range of applications. As industries continue to innovate and seek materials that offer both functionality and adaptability, SMPs are becoming increasingly integral to the development of next-generation technologies. The ability of SMPs to respond to environmental changes makes them a key player in the advancement of smart technologies and sustainable solutions. As research and development in this field advance, the potential for SMPs to revolutionize various sectors becomes more apparent, driving their global market growth.

| Report Metric | Details |

| Report Name | Shape Memory Polymer (SMP) - Market |

| Forecasted market size in 2030 | US$ 3039.9 million |

| CAGR | 25.0% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Nanoshel LLC, SMP Technologies Inc, Asahi Kasei Corporation, Composite Technology Development, Cornerstone Research Group (CRG), MedShape, Shape Memory Medical, EndoShape, Dupont De Nemours, The Lubrizol Corporation; Covestro AG, Guangzhou Manborui Materials Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |