What is Glycobiology & Glycomics - Global Market?

Glycobiology and glycomics are fascinating fields that delve into the study of carbohydrates, or glycans, which are complex sugar molecules found in every living organism. These sugars play crucial roles in various biological processes, including cell signaling, immune response, and protein stability. Glycobiology focuses on understanding the structure, function, and biology of these glycans, while glycomics is the comprehensive study of an organism's entire set of glycans. The global market for glycobiology and glycomics is expanding as researchers and companies recognize the potential of these fields in advancing medical and biotechnological applications. This market encompasses a wide range of products and services, including reagents, enzymes, kits, and instruments, all designed to facilitate the study and manipulation of glycans. As the understanding of glycans' roles in health and disease deepens, the demand for glycobiology and glycomics tools is expected to grow, driving innovation and investment in this promising area of research.

Eagents, Enzymes, Kits, Instruments in the Glycobiology & Glycomics - Global Market:

The global market for glycobiology and glycomics is characterized by a diverse array of products, each playing a vital role in advancing research and applications in this field. Reagents are essential components in glycobiology studies, providing the necessary chemicals and substances to facilitate experiments and analyses. These reagents are used in various applications, such as labeling glycans for detection, modifying glycan structures, and analyzing glycan-protein interactions. Enzymes, another critical product category, are proteins that catalyze biochemical reactions involving glycans. They are used to cleave, modify, or synthesize glycans, enabling researchers to study their structure and function in detail. Enzymes are indispensable in glycomics research, as they allow for the precise manipulation of glycans, aiding in the elucidation of their roles in biological processes. Kits, which often include a combination of reagents and enzymes, provide researchers with ready-to-use solutions for specific glycobiology applications. These kits are designed to streamline experiments, offering convenience and efficiency in studying glycans. They are available for various purposes, such as glycan profiling, glycan labeling, and glycan synthesis, catering to the diverse needs of researchers in the field. Instruments are perhaps the most significant segment in the glycobiology and glycomics market, accounting for a substantial share of the market. These instruments include advanced technologies such as mass spectrometers, chromatography systems, and microarray platforms, which are used to analyze and characterize glycans with high precision and accuracy. Mass spectrometry, for instance, is a powerful tool for identifying and quantifying glycans, providing detailed information on their structure and composition. Chromatography systems are used to separate and purify glycans, enabling researchers to study specific glycan species in isolation. Microarray platforms allow for high-throughput analysis of glycans, facilitating large-scale studies and the discovery of novel glycan biomarkers. The integration of these instruments with sophisticated software and data analysis tools further enhances their capabilities, allowing researchers to gain deeper insights into the complex world of glycans. As the demand for glycobiology and glycomics research continues to grow, the market for these products is expected to expand, driven by advancements in technology and the increasing recognition of glycans' importance in health and disease.

Oncology, Diagnostics, Immunology, Drug Discovery and Development, Others in the Glycobiology & Glycomics - Global Market:

Glycobiology and glycomics have significant applications in various areas of biomedical research and healthcare, including oncology, diagnostics, immunology, drug discovery and development, and other fields. In oncology, the study of glycans is crucial for understanding cancer biology, as changes in glycan structures are often associated with tumor progression and metastasis. Glycomics can help identify cancer-specific glycan biomarkers, which can be used for early detection, prognosis, and monitoring of cancer. Additionally, glycans play a role in modulating the immune response to tumors, making them potential targets for cancer immunotherapy. In diagnostics, glycobiology offers new avenues for developing more accurate and sensitive diagnostic tests. Glycan-based biomarkers can improve the detection of various diseases, including infectious diseases, autoimmune disorders, and metabolic conditions. The ability to analyze glycan patterns in biological samples can lead to the development of novel diagnostic tools that provide valuable insights into disease states and patient health. Immunology is another area where glycobiology and glycomics have a profound impact. Glycans are essential components of the immune system, influencing immune cell interactions, signaling, and responses. Understanding the glycan-mediated mechanisms in immune regulation can lead to the development of new therapies for autoimmune diseases, allergies, and inflammatory conditions. In drug discovery and development, glycobiology plays a pivotal role in identifying new drug targets and designing glycan-based therapeutics. Glycans are involved in drug metabolism, efficacy, and safety, making them critical considerations in the development of biopharmaceuticals. Glycomics can aid in the optimization of drug formulations and the assessment of drug-glycan interactions, ultimately improving drug design and delivery. Beyond these areas, glycobiology and glycomics have applications in fields such as regenerative medicine, where glycans are involved in cell differentiation and tissue regeneration. They also play a role in vaccine development, as glycans are key components of many pathogens and can be targeted to enhance vaccine efficacy. The expanding knowledge of glycans and their functions continues to drive innovation and discovery across multiple disciplines, highlighting the importance of glycobiology and glycomics in advancing healthcare and improving patient outcomes.

Glycobiology & Glycomics - Global Market Outlook:

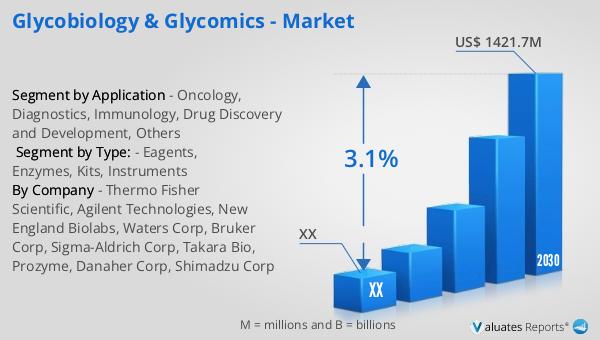

The global market for glycobiology and glycomics was valued at approximately $1,143 million in 2023. It is projected to grow to a revised size of around $1,421.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.1% during the forecast period from 2024 to 2030. This growth is driven by the increasing recognition of the importance of glycans in various biological processes and their potential applications in healthcare and biotechnology. Key players in the global glycobiology and glycomics market include prominent companies such as Thermo Fisher Scientific, Danaher, Shimadzu Corporation, and ProZyme. These companies are at the forefront of developing innovative products and technologies to advance glycobiology research and applications. The top four manufacturers in the market collectively hold a significant share of over 15%, indicating a competitive landscape with a few dominant players. Among the various product segments, instruments represent the largest category, accounting for approximately 34% of the market share. This highlights the critical role of advanced analytical tools and technologies in glycobiology and glycomics research. As the market continues to evolve, the demand for instruments, reagents, enzymes, and kits is expected to grow, driven by ongoing advancements in technology and the increasing recognition of glycans' importance in health and disease.

| Report Metric | Details |

| Report Name | Glycobiology & Glycomics - Market |

| Forecasted market size in 2030 | US$ 1421.7 million |

| CAGR | 3.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Thermo Fisher Scientific, Agilent Technologies, New England Biolabs, Waters Corp, Bruker Corp, Sigma-Aldrich Corp, Takara Bio, Prozyme, Danaher Corp, Shimadzu Corp |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |