What is Rigid Borescopes - Global Market?

Rigid borescopes are specialized optical instruments used for visual inspection in various industries. These devices consist of a rigid tube with an optical lens system that allows users to view areas that are otherwise inaccessible. The global market for rigid borescopes is driven by their application in industries where precision and accuracy are paramount. These instruments are particularly valued for their ability to provide high-resolution images, which are crucial for detailed inspections. The market is expanding as industries increasingly prioritize quality control and maintenance, necessitating reliable inspection tools. Rigid borescopes are preferred in scenarios where flexibility is not required, and a straight-line view is sufficient. Their robust construction makes them suitable for harsh environments, adding to their appeal across sectors such as automotive, aerospace, and power generation. As technology advances, the integration of features like digital imaging and enhanced lighting continues to enhance the functionality of rigid borescopes, further fueling their demand globally. The market's growth is also supported by the increasing adoption of non-destructive testing methods, which rely heavily on tools like borescopes for effective implementation. Overall, the global market for rigid borescopes is poised for steady growth, driven by technological advancements and the rising need for precise inspection solutions.

Semi Rigid, Rigid in the Rigid Borescopes - Global Market:

In the realm of rigid borescopes, the distinction between semi-rigid and rigid variants is crucial for understanding their applications and market dynamics. Semi-rigid borescopes offer a degree of flexibility, allowing them to navigate around slight bends and curves, which makes them suitable for applications where access paths are not perfectly straight. This flexibility is achieved through the use of materials that can bend without compromising the optical clarity or structural integrity of the device. On the other hand, rigid borescopes are constructed with a completely inflexible tube, providing a direct line of sight. This rigidity ensures that the optical path remains perfectly straight, which is essential for applications requiring high precision and accuracy. The choice between semi-rigid and rigid borescopes largely depends on the specific requirements of the inspection task. In industries like aerospace and automotive, where components often have complex geometries, semi-rigid borescopes are invaluable for inspecting areas that are otherwise difficult to access. However, in scenarios where the inspection path is straightforward and precision is critical, rigid borescopes are preferred due to their superior image quality and durability. The global market for these devices is influenced by factors such as technological advancements, industry-specific demands, and the increasing emphasis on quality control. As industries continue to evolve, the demand for both semi-rigid and rigid borescopes is expected to grow, driven by the need for reliable and efficient inspection tools. The integration of advanced features such as digital imaging and enhanced lighting systems further enhances the functionality of these devices, making them indispensable in modern industrial applications. Additionally, the trend towards miniaturization and portability is shaping the development of borescopes, allowing for more versatile and user-friendly designs. This evolution is particularly evident in the semi-rigid segment, where the ability to navigate complex pathways is increasingly important. Meanwhile, the rigid borescope market benefits from the ongoing advancements in optical technology, which continue to improve image resolution and clarity. As a result, both semi-rigid and rigid borescopes are becoming more sophisticated, offering users a wider range of capabilities and applications. The global market for these devices is characterized by a diverse range of products, catering to the specific needs of different industries. From basic models designed for routine inspections to advanced systems equipped with digital imaging and data recording capabilities, the market offers a comprehensive array of options for users. This diversity is a testament to the versatility and adaptability of borescopes, which continue to play a vital role in ensuring the quality and safety of industrial processes worldwide. As the demand for non-destructive testing methods grows, the market for semi-rigid and rigid borescopes is poised for sustained growth, driven by the need for effective and efficient inspection solutions.

Automotive Industry, Power Industry, Aerospace Industry, Construction Industry, Others in the Rigid Borescopes - Global Market:

Rigid borescopes are extensively used across various industries due to their ability to provide high-resolution images for inspection purposes. In the automotive industry, these devices are crucial for inspecting engine components, transmission systems, and other critical parts that require precise examination. The ability to detect defects or wear and tear early on helps in maintaining the performance and safety of vehicles. In the power industry, rigid borescopes are employed to inspect turbines, boilers, and other equipment where direct visual access is limited. This ensures that any potential issues are identified and addressed promptly, minimizing downtime and enhancing operational efficiency. The aerospace industry also relies heavily on rigid borescopes for inspecting aircraft engines, fuselage, and other components. The high precision and clarity offered by these devices are essential for maintaining the safety and reliability of aircraft. In the construction industry, rigid borescopes are used to inspect structural elements, plumbing systems, and other areas where visual access is challenging. This aids in ensuring the integrity and safety of buildings and infrastructure. Beyond these industries, rigid borescopes find applications in fields such as manufacturing, where they are used for quality control and inspection of machinery and equipment. The versatility and reliability of rigid borescopes make them indispensable tools in various sectors, contributing to improved safety, efficiency, and quality across industries.

Rigid Borescopes - Global Market Outlook:

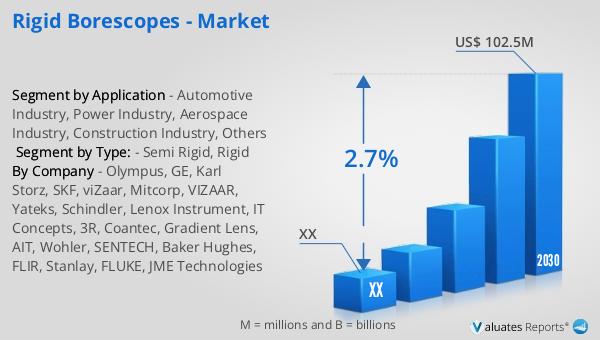

The global market for rigid borescopes was valued at approximately $85 million in 2023, with projections indicating a growth to around $102.5 million by 2030. This represents a compound annual growth rate (CAGR) of 2.7% over the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for precise and reliable inspection tools across various industries. In North America, the market for rigid borescopes is also expected to experience growth, although specific figures were not provided. The steady increase in market size reflects the ongoing advancements in technology and the rising emphasis on quality control and maintenance in industrial applications. As industries continue to prioritize non-destructive testing methods, the demand for rigid borescopes is likely to remain strong. The integration of advanced features such as digital imaging and enhanced lighting systems further enhances the appeal of these devices, making them indispensable in modern industrial applications. Overall, the global market for rigid borescopes is poised for steady growth, driven by technological advancements and the rising need for precise inspection solutions.

| Report Metric | Details |

| Report Name | Rigid Borescopes - Market |

| Forecasted market size in 2030 | US$ 102.5 million |

| CAGR | 2.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Olympus, GE, Karl Storz, SKF, viZaar, Mitcorp, VIZAAR, Yateks, Schindler, Lenox Instrument, IT Concepts, 3R, Coantec, Gradient Lens, AIT, Wohler, SENTECH, Baker Hughes, FLIR, Stanlay, FLUKE, JME Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |