What is Global CMP Silica-Based Slurry Market?

The Global CMP Silica-Based Slurry Market is a specialized segment within the semiconductor industry, focusing on the production and application of chemical mechanical planarization (CMP) slurries that utilize silica as a primary abrasive material. CMP slurries are essential in the manufacturing process of semiconductor devices, as they help in the planarization or smoothing of wafer surfaces, ensuring that layers of materials are uniformly flat. This uniformity is crucial for the subsequent photolithography steps in semiconductor fabrication. The market for CMP silica-based slurries is driven by the increasing demand for advanced electronic devices, which require highly precise and efficient manufacturing processes. The growth in the semiconductor industry, coupled with advancements in technology, has led to a rise in the adoption of CMP silica-based slurries. These slurries are preferred due to their effectiveness in achieving the desired surface finish and their compatibility with various materials used in semiconductor manufacturing. The market is characterized by continuous innovation and development, with companies investing in research and development to improve slurry formulations and enhance performance.

Colloidal Silica Slurry, Fumed Silica Slurry in the Global CMP Silica-Based Slurry Market:

Colloidal Silica Slurry and Fumed Silica Slurry are two primary types of CMP silica-based slurries used in the semiconductor industry. Colloidal silica slurry consists of silica particles suspended in a liquid medium, typically water. These particles are usually in the nanometer size range, providing a high surface area that enhances the slurry's polishing efficiency. Colloidal silica slurries are known for their stability, uniform particle size distribution, and ability to achieve a high degree of planarization with minimal defects. They are widely used in the polishing of silicon wafers, where achieving a smooth and defect-free surface is critical for the performance of semiconductor devices. On the other hand, fumed silica slurry is made from fumed silica, which is produced by the flame hydrolysis of silicon tetrachloride. Fumed silica particles are typically smaller and have a higher surface area compared to colloidal silica particles. This results in a slurry that can achieve a higher removal rate and better surface finish. Fumed silica slurries are often used in applications where a higher degree of material removal is required, such as in the polishing of harder materials like silicon carbide (SiC) wafers. Both types of slurries have their unique advantages and are chosen based on the specific requirements of the polishing process. The choice between colloidal and fumed silica slurries depends on factors such as the material being polished, the desired surface finish, and the specific application within the semiconductor manufacturing process.

Silicon Wafer Slurry, SiC Wafer Slurry, IC CMP Slurry, Others in the Global CMP Silica-Based Slurry Market:

The Global CMP Silica-Based Slurry Market finds extensive usage in various areas, including silicon wafer slurry, SiC wafer slurry, IC CMP slurry, and others. Silicon wafer slurry is primarily used in the planarization of silicon wafers, which are the foundational substrates for semiconductor devices. The slurry helps in achieving a smooth and defect-free surface, which is essential for the subsequent photolithography steps in semiconductor fabrication. SiC wafer slurry, on the other hand, is used in the polishing of silicon carbide wafers. SiC is a harder material compared to silicon, and its wafers are used in high-power and high-frequency electronic devices. The slurry used for SiC wafers needs to have a higher removal rate and better surface finish to meet the stringent requirements of these advanced applications. IC CMP slurry is used in the planarization of integrated circuits (ICs). The slurry helps in smoothing the surface of the ICs, ensuring that the various layers of materials are uniformly flat. This uniformity is crucial for the performance and reliability of the ICs. Other applications of CMP silica-based slurries include the polishing of various materials used in semiconductor manufacturing, such as metals and dielectrics. These slurries help in achieving the desired surface finish and ensuring the performance and reliability of the semiconductor devices. The versatility and effectiveness of CMP silica-based slurries make them an essential component in the semiconductor manufacturing process.

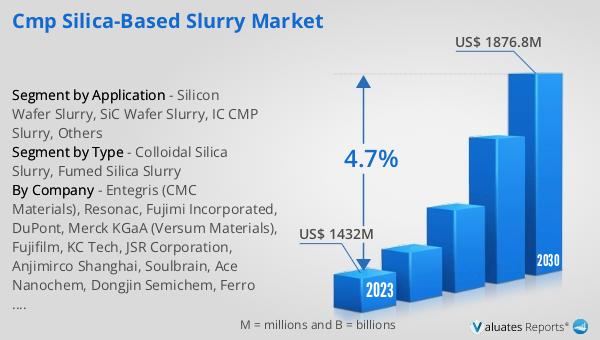

Global CMP Silica-Based Slurry Market Outlook:

The global CMP Silica-Based Slurry market was valued at US$ 1432 million in 2023 and is anticipated to reach US$ 1876.8 million by 2030, witnessing a CAGR of 4.7% during the forecast period 2024-2030. The global market for semiconductors was estimated at US$ 579 billion in the year 2022 and is projected to reach US$ 790 billion by 2029, growing at a CAGR of 6% during the forecast period. This growth in the semiconductor market is expected to drive the demand for CMP silica-based slurries, as they are essential in the manufacturing process of semiconductor devices. The increasing demand for advanced electronic devices, coupled with advancements in technology, is expected to further boost the market for CMP silica-based slurries. Companies in this market are investing in research and development to improve slurry formulations and enhance performance, ensuring that they meet the evolving needs of the semiconductor industry. The continuous innovation and development in this market are expected to drive its growth in the coming years.

| Report Metric | Details |

| Report Name | CMP Silica-Based Slurry Market |

| Accounted market size in 2023 | US$ 1432 million |

| Forecasted market size in 2030 | US$ 1876.8 million |

| CAGR | 4.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Entegris (CMC Materials), Resonac, Fujimi Incorporated, DuPont, Merck KGaA (Versum Materials), Fujifilm, KC Tech, JSR Corporation, Anjimirco Shanghai, Soulbrain, Ace Nanochem, Dongjin Semichem, Ferro (UWiZ Technology), WEC Group, SKC, Shanghai Xinanna Electronic Technology, Hubei Dinglong, Beijing Hangtian Saide |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |