What is Global PCB Processing Equipment Market?

The Global PCB Processing Equipment Market refers to the worldwide industry involved in the manufacturing and distribution of equipment used to produce printed circuit boards (PCBs). PCBs are essential components in virtually all electronic devices, providing the physical platform for mounting and interconnecting electronic components. The market encompasses a wide range of machinery and tools designed to handle various stages of PCB production, from initial design and prototyping to mass production and quality control. This includes equipment for drilling, etching, plating, and testing PCBs, among other processes. The demand for PCB processing equipment is driven by the growing electronics industry, advancements in technology, and the increasing complexity of electronic devices. As electronic devices become more sophisticated and miniaturized, the need for high-precision and efficient PCB processing equipment continues to rise. This market is crucial for ensuring the production of reliable and high-quality PCBs, which are fundamental to the functionality of modern electronic products.

PCB Exposure Equipment, AOI/AVI Equipment, Stripping Equipment, Etching Equipment, Developing Equipment, PCB Drilling Machine, PCB Depaneling Routers, Pretreatment Process Equipment, VCP Equipment, PTH, Flying Probe Tester and Others in the Global PCB Processing Equipment Market:

PCB Exposure Equipment is used in the photolithography process to transfer circuit patterns onto the PCB substrate. This equipment uses light to expose a photoresist-coated PCB to a patterned mask, creating the desired circuit layout. AOI (Automated Optical Inspection) and AVI (Automated Visual Inspection) Equipment are essential for quality control, as they automatically inspect PCBs for defects such as misalignments, short circuits, and open circuits. Stripping Equipment is used to remove unwanted materials from the PCB surface, such as photoresist or other coatings, ensuring a clean and precise circuit pattern. Etching Equipment is crucial for removing excess copper from the PCB, leaving behind the desired circuit traces. Developing Equipment is used to develop the exposed photoresist, revealing the circuit pattern on the PCB. PCB Drilling Machines are used to create precise holes in the PCB for component mounting and interconnections. PCB Depaneling Routers are used to separate individual PCBs from a larger panel, ensuring clean and accurate cuts. Pretreatment Process Equipment prepares the PCB surface for subsequent processing steps, such as cleaning and roughening. VCP (Vertical Continuous Plating) Equipment is used for electroplating the PCB, providing a conductive layer for electrical connections. PTH (Plated Through Hole) Equipment is used to create plated through-holes, which are essential for connecting different layers of the PCB. Flying Probe Testers are used for electrical testing of PCBs, ensuring that all connections are functioning correctly. Other equipment in the PCB processing market includes various tools and machines for specific tasks, such as soldering, laminating, and cutting. Each piece of equipment plays a vital role in the PCB manufacturing process, contributing to the production of high-quality and reliable PCBs.

IC Substrate, Flexible PCBs, HDI Board, Multilayer PCBs in the Global PCB Processing Equipment Market:

The Global PCB Processing Equipment Market finds extensive usage in various types of PCBs, including IC Substrates, Flexible PCBs, HDI Boards, and Multilayer PCBs. IC Substrates are specialized PCBs used as the base for integrated circuits (ICs), providing a platform for mounting and interconnecting ICs with other components. The precision and reliability of PCB processing equipment are crucial for producing high-quality IC substrates, which are essential for the performance of ICs. Flexible PCBs are designed to be bent and folded, making them ideal for applications where space is limited or where the PCB needs to conform to a specific shape. PCB processing equipment used for flexible PCBs must be capable of handling the unique properties of flexible materials, ensuring accurate and reliable production. HDI (High-Density Interconnect) Boards are advanced PCBs with a higher density of interconnections, allowing for more complex and compact designs. The production of HDI boards requires high-precision equipment to achieve the necessary level of detail and accuracy. Multilayer PCBs consist of multiple layers of circuitry stacked together, providing increased functionality and performance. The manufacturing of multilayer PCBs involves complex processes, including lamination, drilling, and plating, all of which require specialized equipment to ensure quality and reliability. The Global PCB Processing Equipment Market plays a critical role in the production of these various types of PCBs, enabling the development of advanced electronic devices with enhanced performance and functionality.

Global PCB Processing Equipment Market Outlook:

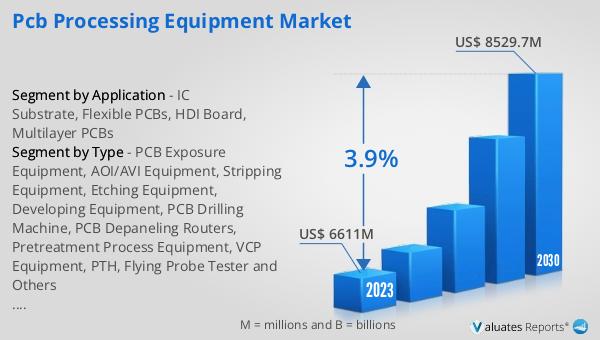

The global PCB Processing Equipment market was valued at US$ 6611 million in 2023 and is anticipated to reach US$ 8529.7 million by 2030, witnessing a CAGR of 3.9% during the forecast period 2024-2030. This market growth reflects the increasing demand for advanced PCB processing equipment driven by the rapid advancements in electronic devices and technology. As electronic devices become more complex and miniaturized, the need for high-precision and efficient PCB processing equipment continues to rise. The market encompasses a wide range of machinery and tools designed to handle various stages of PCB production, from initial design and prototyping to mass production and quality control. This includes equipment for drilling, etching, plating, and testing PCBs, among other processes. The demand for PCB processing equipment is driven by the growing electronics industry, advancements in technology, and the increasing complexity of electronic devices. This market is crucial for ensuring the production of reliable and high-quality PCBs, which are fundamental to the functionality of modern electronic products.

| Report Metric | Details |

| Report Name | PCB Processing Equipment Market |

| Accounted market size in 2023 | US$ 6611 million |

| Forecasted market size in 2030 | US$ 8529.7 million |

| CAGR | 3.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Ninomiya System CO., Ltd., Screen, Ishii Hyoki, Centrotherm, Hakuto.co.ltd, TONETS Corp., Notion Systems GmbH, Via Mechanics, Ltd., Orbotech (KLA), ADTEC, Chime Ball Technology, ORC Manufacturing, Manz (KLEO), Ofuna Technology Co., Ltd., Symtek Automation, C SUN, AMPOC, GROUP UP Industrial (GP), Gallant Precision Machining (GPM), Eclat Forever Company, Utechzone, Ta Liang Technology, MACHVISION Inc Co., LTD, GigaVis, CIMS, Favite, FUSEI MENIX, Trumpf, Mycronic (atg), INSPEC, Saki Corporation, Omron, Koh Young, Test Research, Inc(TRI), Viscom, Mek (Marantz Electronics), Nordson, ViTrox, CyberOptics, Machine Vision Products, CKD Corporation, SCHMID, Genitec, ASYS Group, MSTECH, Atotech (MKS), Advanced Engineering (AE), Amada, LPKF, Mitsubishi Electric, EO Technics, Trotec |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |