What is Global MLCC Electronic Conductive Paste Market?

The Global MLCC (Multilayer Ceramic Capacitor) Electronic Conductive Paste Market is a specialized segment within the broader electronics industry. This market focuses on the production and distribution of conductive pastes used in the manufacturing of MLCCs, which are essential components in various electronic devices. Conductive pastes are materials that facilitate the flow of electricity within the MLCCs, ensuring their proper functioning. These pastes are typically composed of metal particles, such as silver or palladium, suspended in a resin or solvent. The demand for MLCCs has been on the rise due to their widespread application in consumer electronics, automotive electronics, telecommunications, and industrial equipment. As technology advances and the need for more compact and efficient electronic components grows, the importance of high-quality conductive pastes becomes even more critical. The market for these pastes is driven by the increasing production of electronic devices and the continuous innovation in electronic materials and manufacturing processes.

Internal Electrode Slurry, External Electrode Paste in the Global MLCC Electronic Conductive Paste Market:

Internal Electrode Slurry and External Electrode Paste are two critical components in the Global MLCC Electronic Conductive Paste Market. Internal Electrode Slurry is a type of conductive paste used to form the internal electrodes within an MLCC. These internal electrodes are crucial for the capacitor's ability to store and release electrical energy. The slurry typically contains fine metal particles, such as nickel or silver, dispersed in a liquid medium. This mixture is applied to the ceramic layers during the manufacturing process, creating the internal conductive pathways that allow the capacitor to function. The quality and composition of the internal electrode slurry directly impact the performance and reliability of the MLCC. On the other hand, External Electrode Paste is used to form the external electrodes of the MLCC. These external electrodes connect the internal structure of the capacitor to the external circuit, enabling the flow of electricity in and out of the component. The paste is usually made of metal particles, such as silver or copper, mixed with a binder and solvent. The application of external electrode paste is a critical step in the MLCC manufacturing process, as it ensures the proper electrical connection and mechanical stability of the capacitor. Both internal electrode slurry and external electrode paste play vital roles in the overall performance of MLCCs. The development and optimization of these conductive pastes are essential for improving the efficiency, reliability, and miniaturization of electronic devices. As the demand for smaller and more powerful electronic components continues to grow, the importance of high-quality conductive pastes in the MLCC market cannot be overstated.

Consumer Electronics, 5G Base Station, Automotive Electronics, Industry, Others in the Global MLCC Electronic Conductive Paste Market:

The usage of Global MLCC Electronic Conductive Paste Market spans across various sectors, including Consumer Electronics, 5G Base Stations, Automotive Electronics, Industry, and others. In Consumer Electronics, MLCCs are widely used in devices such as smartphones, tablets, laptops, and wearable technology. The conductive pastes used in these capacitors ensure efficient electrical performance, contributing to the overall functionality and reliability of the devices. As consumer electronics continue to evolve with more advanced features and higher performance requirements, the demand for high-quality MLCCs and conductive pastes is expected to increase. In the realm of 5G Base Stations, MLCCs play a crucial role in the infrastructure needed to support the next generation of wireless communication. The conductive pastes used in these capacitors help maintain the integrity and efficiency of the electrical connections, which is vital for the high-speed data transmission and low latency required by 5G technology. Automotive Electronics is another significant area where MLCCs and conductive pastes are extensively used. Modern vehicles are equipped with numerous electronic systems, including advanced driver-assistance systems (ADAS), infotainment systems, and electric powertrains. The reliability and performance of these systems depend on the quality of the MLCCs and the conductive pastes used in their construction. In the Industrial sector, MLCCs are used in various applications, such as industrial automation, robotics, and power supplies. The conductive pastes in these capacitors ensure stable and efficient electrical performance, which is critical for the smooth operation of industrial equipment. Other areas where MLCCs and conductive pastes are used include medical devices, aerospace, and telecommunications. The versatility and reliability of MLCCs make them an essential component in a wide range of electronic applications, driving the demand for high-quality conductive pastes in the global market.

Global MLCC Electronic Conductive Paste Market Outlook:

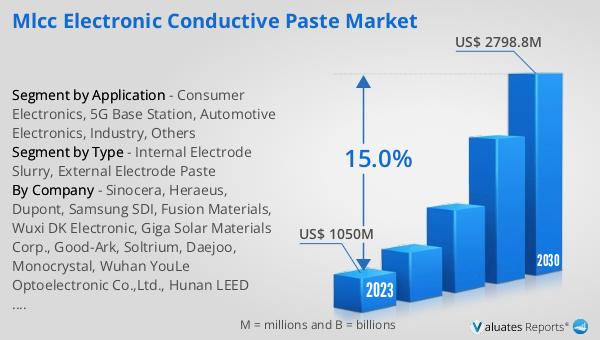

The global MLCC Electronic Conductive Paste market was valued at US$ 1050 million in 2023 and is anticipated to reach US$ 2798.8 million by 2030, witnessing a CAGR of 15.0% during the forecast period 2024-2030. This significant growth reflects the increasing demand for MLCCs across various industries, driven by advancements in technology and the need for more efficient and compact electronic components. The market's expansion is fueled by the continuous innovation in conductive paste formulations, which enhance the performance and reliability of MLCCs. As electronic devices become more sophisticated and their applications more diverse, the importance of high-quality conductive pastes in ensuring the optimal performance of MLCCs cannot be overstated. The projected growth of the MLCC Electronic Conductive Paste market underscores the critical role these materials play in the electronics industry, supporting the development of cutting-edge technologies and the production of high-performance electronic devices.

| Report Metric | Details |

| Report Name | MLCC Electronic Conductive Paste Market |

| Accounted market size in 2023 | US$ 1050 million |

| Forecasted market size in 2030 | US$ 2798.8 million |

| CAGR | 15.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Sinocera, Heraeus, Dupont, Samsung SDI, Fusion Materials, Wuxi DK Electronic, Giga Solar Materials Corp., Good-Ark, Soltrium, Daejoo, Monocrystal, Wuhan YouLe Optoelectronic Co.,Ltd., Hunan LEED Electronic Ink, Sumitomo Metal, Shoei Chemical Inc., Rutech, Fuji Chemical Research, Fukuda Metal Foil & Powde, Asahi Chemical Research Laboratory, Daiken Chemical, Kyoto Elex, Ningbo Jingxin Electronic Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |