What is Global Product Design Apps Market?

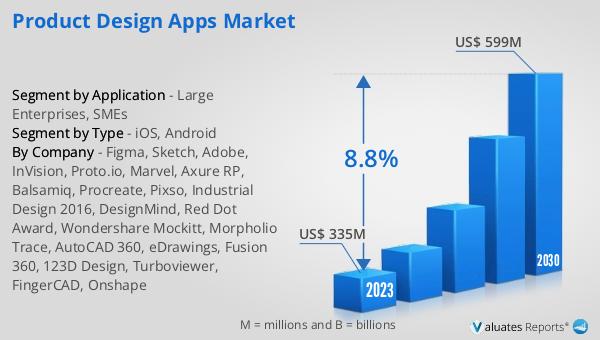

The global Product Design Apps market is a rapidly evolving sector that focuses on software applications used for designing products across various industries. These apps are essential tools for designers, engineers, and product developers, enabling them to create, modify, analyze, and optimize designs with precision and efficiency. The market encompasses a wide range of applications, from simple sketching tools to complex 3D modeling software. These apps are used in industries such as automotive, aerospace, consumer electronics, and fashion, among others. The increasing demand for innovative and customized products, coupled with advancements in technology, has significantly driven the growth of this market. Additionally, the integration of artificial intelligence and machine learning in these apps has further enhanced their capabilities, making them indispensable in the product development process. The global Product Design Apps market was valued at US$ 335 million in 2023 and is anticipated to reach US$ 599 million by 2030, witnessing a CAGR of 8.8% during the forecast period 2024-2030. This growth is attributed to the rising adoption of these apps by both large enterprises and small and medium-sized enterprises (SMEs) to streamline their design processes and improve productivity.

iOS, Android in the Global Product Design Apps Market:

iOS and Android platforms play a crucial role in the Global Product Design Apps market, catering to a diverse range of users with varying needs and preferences. iOS, developed by Apple Inc., is known for its robust security features, seamless integration with other Apple products, and a user-friendly interface. Product design apps on iOS are highly optimized for performance, offering smooth and responsive experiences. These apps leverage the powerful hardware capabilities of Apple devices, such as the iPad Pro and iPhone, to deliver high-quality graphics and efficient processing. Popular product design apps on iOS include Procreate, Shapr3D, and Concepts, which are widely used by designers for sketching, 3D modeling, and vector illustration. On the other hand, Android, developed by Google, offers a more open and customizable platform, which appeals to a broader audience. Android-based product design apps are compatible with a wide range of devices from various manufacturers, providing users with more options in terms of hardware and price points. This flexibility makes Android a popular choice among SMEs and individual designers who may have budget constraints. Some well-known product design apps on Android include AutoCAD, SketchBook, and Tinkercad. These apps offer a range of features, from basic drawing tools to advanced 3D modeling capabilities, catering to different levels of expertise and requirements. The availability of cloud-based services and cross-platform compatibility further enhances the usability of these apps, allowing designers to work seamlessly across different devices and operating systems. Both iOS and Android platforms continue to evolve, incorporating new technologies such as augmented reality (AR) and virtual reality (VR) to provide more immersive and interactive design experiences. The competition between these platforms drives innovation, resulting in continuous improvements in app performance, user experience, and functionality. As a result, the Global Product Design Apps market benefits from a diverse ecosystem of apps that cater to the needs of various users, from professional designers to hobbyists. The choice between iOS and Android ultimately depends on individual preferences, budget, and specific requirements, but both platforms offer powerful tools that significantly enhance the product design process.

Large Enterprises, SMEs in the Global Product Design Apps Market:

The usage of Global Product Design Apps in large enterprises and SMEs varies significantly, reflecting the distinct needs and resources of these organizations. Large enterprises, with their substantial budgets and extensive resources, often invest in high-end product design apps that offer advanced features and capabilities. These apps are integrated into their comprehensive product development workflows, enabling teams to collaborate efficiently and streamline the design process. For instance, large automotive or aerospace companies may use sophisticated 3D modeling and simulation tools to design complex components and systems. These tools allow for detailed analysis and optimization, reducing the time and cost associated with physical prototyping. Additionally, large enterprises often leverage cloud-based solutions to facilitate collaboration among geographically dispersed teams, ensuring that all stakeholders have access to the latest design iterations and can provide real-time feedback. On the other hand, SMEs typically operate with more limited budgets and resources, which influences their choice of product design apps. These organizations often prioritize cost-effective solutions that offer a good balance between functionality and affordability. Many SMEs opt for subscription-based or freemium models, which allow them to access essential design tools without significant upfront investment. For example, a small fashion design studio might use apps like Adobe Illustrator or CorelDRAW for creating digital sketches and patterns. These apps provide the necessary features for designing and visualizing products while being accessible to smaller teams with limited financial resources. Furthermore, SMEs often benefit from the flexibility and scalability of cloud-based design apps, which enable them to scale their usage according to their needs and budget. The ability to collaborate remotely and access designs from any location is particularly advantageous for SMEs, as it allows them to work with clients and partners across different regions without the need for extensive infrastructure. In summary, while large enterprises and SMEs both utilize Global Product Design Apps to enhance their design processes, their specific needs and constraints shape their choices and usage patterns. Large enterprises focus on advanced features, integration, and collaboration, while SMEs prioritize cost-effectiveness, flexibility, and scalability. Despite these differences, the overarching goal remains the same: to leverage technology to create innovative and high-quality products efficiently.

Global Product Design Apps Market Outlook:

The global Product Design Apps market, valued at US$ 335 million in 2023, is on a growth trajectory, with expectations to reach US$ 599 million by 2030. This impressive growth, marked by a compound annual growth rate (CAGR) of 8.8% from 2024 to 2030, underscores the increasing adoption and reliance on these apps across various industries. The market's expansion is driven by the rising demand for innovative and customized products, which necessitates the use of advanced design tools. Both large enterprises and SMEs are recognizing the value of these apps in streamlining their design processes, enhancing productivity, and reducing time-to-market. The integration of cutting-edge technologies such as artificial intelligence, machine learning, augmented reality, and virtual reality into product design apps is further propelling their adoption. These technologies enable designers to create more sophisticated and optimized designs, improving overall product quality and performance. Additionally, the shift towards cloud-based solutions is facilitating better collaboration and accessibility, allowing teams to work seamlessly across different locations and devices. As a result, the global Product Design Apps market is poised for significant growth, reflecting the critical role these tools play in modern product development.

| Report Metric | Details |

| Report Name | Product Design Apps Market |

| Accounted market size in 2023 | US$ 335 million |

| Forecasted market size in 2030 | US$ 599 million |

| CAGR | 8.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Figma, Sketch, Adobe, InVision, Proto.io, Marvel, Axure RP, Balsamiq, Procreate, Pixso, Industrial Design 2016, DesignMind, Red Dot Award, Wondershare Mockitt, Morpholio Trace, AutoCAD 360, eDrawings, Fusion 360, 123D Design, Turboviewer, FingerCAD, Onshape |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |