What is Global AI Architecture Design Software Market?

The Global AI Architecture Design Software Market refers to the worldwide industry focused on the development and distribution of software solutions that leverage artificial intelligence (AI) to aid in architectural design. These software tools utilize advanced algorithms and machine learning techniques to assist architects, engineers, and designers in creating more efficient, innovative, and sustainable building designs. By automating complex calculations, optimizing resource usage, and providing predictive analytics, AI architecture design software enhances the overall design process, making it faster and more accurate. This market encompasses a variety of software products, ranging from those that offer basic design assistance to highly sophisticated platforms capable of generating complete architectural plans. The growing demand for smart buildings, sustainable construction practices, and the integration of IoT (Internet of Things) in architecture are key drivers propelling the expansion of this market. As technology continues to evolve, the Global AI Architecture Design Software Market is expected to play a crucial role in shaping the future of architectural design.

On Premises, Cloud-based in the Global AI Architecture Design Software Market:

On-premises and cloud-based solutions are two primary deployment models in the Global AI Architecture Design Software Market, each offering distinct advantages and catering to different user needs. On-premises AI architecture design software is installed and run on computers within the user's organization. This model provides greater control over data security and privacy, as all information is stored locally. It is particularly beneficial for large firms with robust IT infrastructure and stringent data protection requirements. On-premises solutions often offer higher performance and customization options, allowing organizations to tailor the software to their specific needs. However, they require significant upfront investment in hardware and ongoing maintenance costs, which can be a barrier for smaller firms. In contrast, cloud-based AI architecture design software is hosted on remote servers and accessed via the internet. This model offers several advantages, including lower initial costs, as there is no need for expensive hardware. Users can access the software from anywhere with an internet connection, making it ideal for remote work and collaboration. Cloud-based solutions are also scalable, allowing organizations to easily adjust their usage based on demand. Additionally, updates and maintenance are handled by the service provider, reducing the burden on the user's IT department. However, cloud-based solutions may raise concerns about data security and privacy, as sensitive information is stored off-site. Despite these concerns, the flexibility and cost-effectiveness of cloud-based AI architecture design software make it an attractive option for many organizations. Both on-premises and cloud-based solutions have their own set of challenges and benefits. On-premises solutions offer greater control and customization but come with higher costs and maintenance requirements. Cloud-based solutions provide flexibility, scalability, and lower upfront costs but may pose data security risks. The choice between these two deployment models depends on the specific needs and resources of the organization. For instance, a large architectural firm with a dedicated IT team and strict data security requirements might prefer an on-premises solution. In contrast, a smaller firm or a startup with limited resources might opt for a cloud-based solution to take advantage of its lower costs and ease of access. The Global AI Architecture Design Software Market is witnessing a growing trend towards hybrid solutions that combine the best of both worlds. Hybrid solutions allow organizations to store sensitive data on-premises while leveraging the scalability and flexibility of the cloud for other functions. This approach provides a balanced solution that addresses both security concerns and the need for cost-effective, scalable software. As technology continues to evolve, we can expect to see further innovations in deployment models, offering even more options for organizations looking to leverage AI in their architectural design processes. In conclusion, the choice between on-premises and cloud-based AI architecture design software depends on various factors, including the organization's size, budget, and specific needs. Both models offer unique advantages and challenges, and the decision should be based on a careful assessment of these factors. As the Global AI Architecture Design Software Market continues to grow, we can expect to see more diverse and innovative solutions that cater to the evolving needs of architects, engineers, and designers worldwide.

Builders, Developers, Others in the Global AI Architecture Design Software Market:

The usage of Global AI Architecture Design Software Market spans across various sectors, including builders, developers, and others, each benefiting uniquely from these advanced tools. Builders, for instance, utilize AI architecture design software to streamline the construction process. By leveraging AI, builders can optimize resource allocation, reduce waste, and enhance project timelines. The software can predict potential issues before they arise, allowing builders to address them proactively. This not only saves time and money but also improves the overall quality of the construction. Additionally, AI-powered tools can assist in ensuring compliance with building codes and regulations, reducing the risk of costly legal issues. Developers, on the other hand, use AI architecture design software to create innovative and sustainable building designs. The software's ability to analyze vast amounts of data and generate predictive models allows developers to design buildings that are not only aesthetically pleasing but also energy-efficient and environmentally friendly. AI can help developers identify the best materials and construction methods to achieve their sustainability goals. Furthermore, the software can simulate various design scenarios, enabling developers to make informed decisions and optimize their designs for maximum efficiency and cost-effectiveness. This is particularly important in today's market, where there is a growing demand for green buildings and sustainable construction practices. Other sectors, such as urban planners and interior designers, also benefit from AI architecture design software. Urban planners can use the software to design smart cities that are efficient, sustainable, and resilient. AI can analyze data on traffic patterns, population growth, and environmental factors to create urban designs that optimize space and resources. This can lead to more livable and sustainable cities that meet the needs of their residents. Interior designers, meanwhile, can use AI tools to create personalized and functional interior spaces. The software can analyze a client's preferences and lifestyle to generate design recommendations that are tailored to their needs. This not only enhances the client experience but also allows designers to create more innovative and customized interior spaces. In addition to these specific sectors, the Global AI Architecture Design Software Market also benefits other stakeholders, such as investors and policymakers. Investors can use AI tools to assess the feasibility and profitability of construction projects. The software can analyze market trends, financial data, and other relevant factors to provide insights into the potential return on investment. This can help investors make more informed decisions and reduce the risk of financial losses. Policymakers, on the other hand, can use AI architecture design software to develop and implement policies that promote sustainable and efficient construction practices. The software can provide data-driven insights into the impact of various policies, helping policymakers create regulations that support the growth of the construction industry while also protecting the environment. In conclusion, the Global AI Architecture Design Software Market offers a wide range of benefits to various sectors, including builders, developers, urban planners, interior designers, investors, and policymakers. By leveraging AI, these stakeholders can optimize their processes, reduce costs, and create more innovative and sustainable designs. As the market continues to grow, we can expect to see even more applications of AI architecture design software, further transforming the construction and design industries.

Global AI Architecture Design Software Market Outlook:

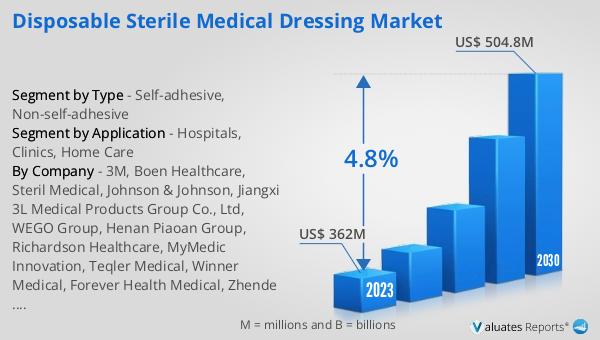

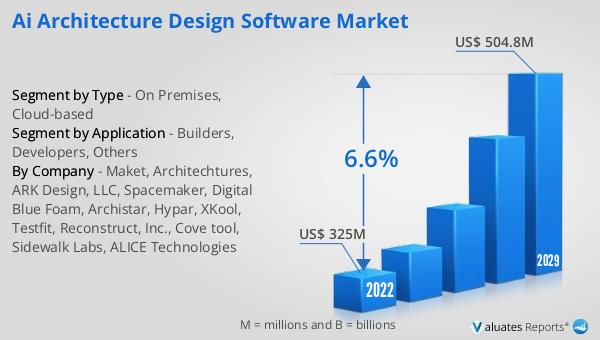

The global AI Architecture Design Software market was valued at US$ 325 million in 2023 and is anticipated to reach US$ 504.8 million by 2030, witnessing a CAGR of 6.6% during the forecast period 2024-2030. To maintain its leading position, the United States will increase its investment in artificial intelligence research and development in non-defense fields from US$1.6 billion to US$1.7 billion in 2022. This significant investment underscores the growing importance of AI in various sectors, including architecture and design. By boosting funding for AI research and development, the United States aims to foster innovation and maintain its competitive edge in the global market. This increased investment is expected to drive advancements in AI architecture design software, leading to more sophisticated and efficient tools that can further enhance the design process. As a result, the market is poised for substantial growth, with more organizations adopting AI-powered solutions to improve their architectural designs and construction practices. This trend highlights the critical role of AI in shaping the future of the architecture and design industries, as well as the broader impact of AI on the global economy.

| Report Metric | Details |

| Report Name | AI Architecture Design Software Market |

| Accounted market size in 2023 | US$ 325 million |

| Forecasted market size in 2030 | US$ 504.8 million |

| CAGR | 6.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Maket, Architechtures, ARK Design, LLC, Spacemaker, Digital Blue Foam, Archistar, Hypar, XKool, Testfit, Reconstruct, Inc., Cove tool, Sidewalk Labs, ALICE Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |