What is Global Left-handed Edition Ergonomic Mouses Market?

The Global Left-handed Edition Ergonomic Mouses Market is a specialized segment within the broader computer peripherals industry, focusing on the design and production of ergonomic mice tailored specifically for left-handed users. These products are engineered to provide comfort and efficiency, reducing strain and the risk of repetitive strain injuries (RSIs) that can occur from prolonged use of standard mice. The market caters to a niche audience, including left-handed individuals who often face challenges finding suitable ergonomic devices. Companies in this market invest in research and development to create innovative designs that align with the natural hand posture of left-handed users. This market is driven by the increasing awareness of ergonomic health, the growing number of left-handed individuals seeking specialized products, and advancements in technology that allow for more customizable and user-friendly designs. The Global Left-handed Edition Ergonomic Mouses Market is expected to see steady growth as more consumers prioritize ergonomic health and as manufacturers continue to innovate and expand their product offerings.

Wired, Wireless in the Global Left-handed Edition Ergonomic Mouses Market:

When it comes to the Global Left-handed Edition Ergonomic Mouses Market, the products can be broadly categorized into wired and wireless variants. Wired ergonomic mice are connected to the computer via a cable, usually through a USB port. These mice are often preferred by users who prioritize a stable and uninterrupted connection, as they do not rely on batteries and are less susceptible to interference. Wired mice are particularly popular among gamers and professionals who require high precision and responsiveness. On the other hand, wireless ergonomic mice offer the convenience of mobility and a clutter-free workspace. These mice connect to the computer via Bluetooth or a wireless USB receiver. They are powered by batteries, which can be either rechargeable or disposable. Wireless mice are favored by users who value portability and a clean desk setup. Both wired and wireless left-handed ergonomic mice are designed to reduce strain on the hand and wrist, featuring contoured shapes, customizable buttons, and adjustable sensitivity settings. The choice between wired and wireless often comes down to personal preference and specific use cases. For instance, a graphic designer might prefer a wireless mouse for its flexibility, while a competitive gamer might opt for a wired mouse for its reliability. The market for these products is expanding as more left-handed users seek ergonomic solutions that cater to their specific needs. Manufacturers are continuously innovating to improve the functionality, comfort, and aesthetic appeal of both wired and wireless ergonomic mice.

Online, Offline in the Global Left-handed Edition Ergonomic Mouses Market:

The usage of Global Left-handed Edition Ergonomic Mouses Market products can be divided into online and offline channels. Online channels include e-commerce platforms, company websites, and online marketplaces where consumers can browse, compare, and purchase ergonomic mice from the comfort of their homes. The online market offers a wide range of options, detailed product descriptions, customer reviews, and often competitive pricing. This convenience has made online shopping increasingly popular among consumers. Additionally, online platforms often provide educational content about the benefits of ergonomic products, helping consumers make informed decisions. On the other hand, offline channels include physical retail stores, electronics shops, and specialty ergonomic stores where consumers can physically interact with the products before making a purchase. This tactile experience is crucial for many buyers who want to feel the comfort and fit of the mouse in their hand. Offline shopping also allows for immediate purchase and use, without the wait time associated with shipping. Both online and offline channels play a significant role in the distribution of left-handed ergonomic mice. While online channels offer convenience and a broader selection, offline channels provide a hands-on experience and immediate gratification. The choice between online and offline shopping often depends on the consumer's preference for convenience versus the need for a tactile experience. As the market continues to grow, both channels are expected to evolve, offering more personalized and seamless shopping experiences for left-handed users seeking ergonomic solutions.

Global Left-handed Edition Ergonomic Mouses Market Outlook:

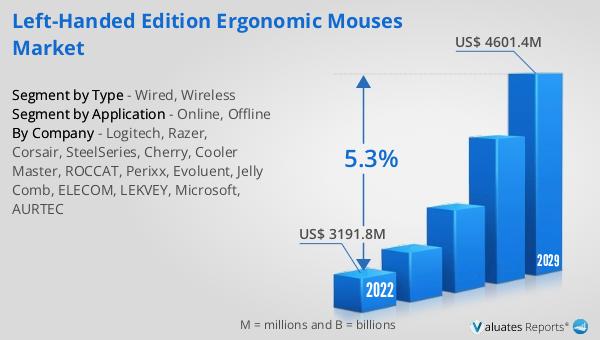

The Global PC Gaming Peripheral market is anticipated to grow significantly, with projections indicating it will reach approximately US$ 4601.4 million by the year 2029. This marks an increase from US$ 3191.8 million in 2022, reflecting a compound annual growth rate (CAGR) of 5.3% over the period from 2023 to 2029. This growth can be attributed to several factors, including the rising popularity of PC gaming, advancements in gaming technology, and the increasing demand for high-performance gaming peripherals such as mice, keyboards, and headsets. As the gaming community continues to expand, driven by both casual and professional gamers, the need for specialized and high-quality peripherals is expected to rise. Companies in this market are likely to focus on innovation, offering products that enhance the gaming experience through improved ergonomics, precision, and customization options. The projected growth underscores the dynamic nature of the PC gaming peripheral market and its potential for continued expansion in the coming years.

| Report Metric | Details |

| Report Name | Left-handed Edition Ergonomic Mouses Market |

| Accounted market size in 2022 | US$ 3191.8 million |

| Forecasted market size in 2029 | US$ 4601.4 million |

| CAGR | 5.3% |

| Base Year | 2022 |

| Forecasted years | 2024 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Logitech, Razer, Corsair, SteelSeries, Cherry, Cooler Master, ROCCAT, Perixx, Evoluent, Jelly Comb, ELECOM, LEKVEY, Microsoft, AURTEC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |