What is Global Solenoid Cartridge Valves Market?

The Global Solenoid Cartridge Valves Market refers to the worldwide industry focused on the production, distribution, and application of solenoid cartridge valves. These valves are essential components in various hydraulic and pneumatic systems, controlling the flow and direction of fluids through an electromagnetic solenoid mechanism. The market encompasses a wide range of industries, including construction, agriculture, automotive, and industrial machinery, where these valves are used to enhance efficiency, precision, and automation. The demand for solenoid cartridge valves is driven by the need for advanced fluid control solutions that can operate reliably under diverse conditions. As industries continue to modernize and adopt more sophisticated machinery, the global solenoid cartridge valves market is expected to grow, offering innovative solutions to meet the evolving needs of different sectors.

Manual, Electric, Pneumatic in the Global Solenoid Cartridge Valves Market:

Solenoid cartridge valves can be categorized based on their actuation methods: manual, electric, and pneumatic. Manual solenoid cartridge valves are operated by hand, requiring physical effort to control the flow of fluids. These valves are typically used in applications where automation is not necessary or where manual control is preferred for safety or simplicity. They are common in basic hydraulic systems and small-scale machinery where precise control is not critical. Electric solenoid cartridge valves, on the other hand, use an electromagnetic solenoid to control the valve's operation. When an electric current passes through the solenoid, it creates a magnetic field that moves a plunger, opening or closing the valve. These valves are widely used in automated systems due to their precision, reliability, and ease of integration with electronic control systems. They are found in various applications, from automotive fuel systems to industrial automation, where precise fluid control is essential. Pneumatic solenoid cartridge valves operate using compressed air to actuate the valve mechanism. These valves are favored in environments where electrical components might pose a risk, such as in explosive atmospheres or where electrical interference could be problematic. Pneumatic valves are also used in systems where air pressure is readily available and can be harnessed for efficient valve operation. They are common in industrial machinery, material handling equipment, and other applications where robust and reliable fluid control is required. Each type of solenoid cartridge valve offers unique advantages and is chosen based on the specific requirements of the application, including factors like control precision, environmental conditions, and safety considerations.

Construction Machinery, Material Handling Equipment, Agricultural Machinery, Others in the Global Solenoid Cartridge Valves Market:

The usage of solenoid cartridge valves in various sectors highlights their versatility and importance. In construction machinery, these valves are integral to the hydraulic systems that power equipment such as excavators, loaders, and cranes. They enable precise control of fluid flow, ensuring smooth and efficient operation of heavy machinery. This precision is crucial for tasks that require fine control, such as lifting, digging, and material handling. In material handling equipment, solenoid cartridge valves are used to control the movement of goods and materials. Forklifts, conveyor systems, and automated storage and retrieval systems rely on these valves to manage the flow of hydraulic fluid, enabling accurate and reliable operation. The ability to control fluid flow precisely ensures that materials are handled safely and efficiently, reducing the risk of damage and improving productivity. Agricultural machinery also benefits from the use of solenoid cartridge valves. Tractors, harvesters, and irrigation systems use these valves to control various functions, from steering and braking to the operation of attachments like plows and sprayers. The reliability and precision of solenoid cartridge valves help farmers optimize their operations, improving crop yields and reducing labor costs. Beyond these specific applications, solenoid cartridge valves are used in a wide range of other industries. They are found in automotive systems, where they control fuel injection, transmission, and braking systems. In industrial automation, they are used to control the movement of robotic arms, conveyor belts, and other machinery. The versatility of solenoid cartridge valves makes them an essential component in many different types of equipment, contributing to improved efficiency, safety, and performance across various sectors.

Global Solenoid Cartridge Valves Market Outlook:

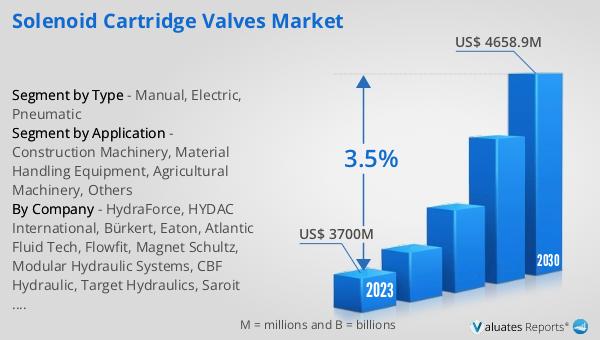

The global Solenoid Cartridge Valves market was valued at US$ 3700 million in 2023 and is anticipated to reach US$ 4658.9 million by 2030, witnessing a CAGR of 3.5% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the solenoid cartridge valves industry, driven by increasing demand across various sectors. The projected growth reflects the ongoing advancements in technology and the rising need for efficient fluid control solutions in industries such as construction, agriculture, automotive, and industrial machinery. As these industries continue to evolve and adopt more sophisticated equipment, the demand for reliable and precise solenoid cartridge valves is expected to rise. The market's growth is also supported by the expanding applications of these valves in emerging markets and the continuous development of new and innovative valve technologies. This positive outlook underscores the importance of solenoid cartridge valves in modern industrial applications and highlights the potential for continued growth and innovation in this sector.

| Report Metric | Details |

| Report Name | Solenoid Cartridge Valves Market |

| Accounted market size in 2023 | US$ 3700 million |

| Forecasted market size in 2030 | US$ 4658.9 million |

| CAGR | 3.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | HydraForce, HYDAC International, Bürkert, Eaton, Atlantic Fluid Tech, Flowfit, Magnet Schultz, Modular Hydraulic Systems, CBF Hydraulic, Target Hydraulics, Saroit Hydraulics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |