What is Global Ethylene Octene Copolymer Market?

The Global Ethylene Octene Copolymer Market refers to the worldwide industry involved in the production, distribution, and application of ethylene-octene copolymers. These copolymers are a type of polyolefin elastomer, which are known for their flexibility, durability, and resistance to various environmental factors. They are synthesized by copolymerizing ethylene with octene, resulting in materials that exhibit excellent impact resistance, low-temperature performance, and high elasticity. These properties make ethylene-octene copolymers highly desirable for a wide range of applications, including automotive parts, consumer products, wire and cable insulation, foams, footwear, and packaging products. The market for these copolymers is driven by the increasing demand for lightweight and durable materials in various industries, as well as advancements in polymer technology that enhance the performance characteristics of these materials. As industries continue to seek materials that offer a balance of strength, flexibility, and environmental resistance, the global ethylene-octene copolymer market is expected to grow steadily.

Injection Grade, General Grade, Extrusion Grade in the Global Ethylene Octene Copolymer Market:

Ethylene-octene copolymers are available in various grades, each tailored to specific applications and processing methods. Injection Grade ethylene-octene copolymers are designed for use in injection molding processes, where the material is melted and injected into molds to form complex shapes and components. This grade is characterized by its excellent flow properties, allowing it to fill molds efficiently and produce parts with fine details and smooth surfaces. Injection Grade copolymers are commonly used in the automotive industry for manufacturing interior and exterior components, as well as in consumer products such as toys, household items, and electronic housings. General Grade ethylene-octene copolymers, on the other hand, offer a balance of properties suitable for a wide range of applications. These copolymers are versatile and can be processed using various methods, including extrusion, blow molding, and thermoforming. They are used in the production of flexible packaging, films, and sheets, as well as in the construction of hoses, gaskets, and seals. General Grade copolymers provide good mechanical strength, flexibility, and resistance to environmental stress cracking, making them ideal for applications that require durability and reliability. Extrusion Grade ethylene-octene copolymers are specifically formulated for extrusion processes, where the material is forced through a die to create continuous shapes such as pipes, profiles, and cables. This grade exhibits excellent melt strength and stability, ensuring consistent extrusion performance and high-quality end products. Extrusion Grade copolymers are widely used in the wire and cable industry for insulation and jacketing, as well as in the production of foams for cushioning and packaging applications. The unique properties of ethylene-octene copolymers, combined with their availability in different grades, make them a valuable material for a diverse range of industries.

Automotive Parts, Consumer Products, Wire and Cable, Foams and Footwears, Packaging Products, Others in the Global Ethylene Octene Copolymer Market:

The usage of Global Ethylene Octene Copolymer Market spans across various industries, each benefiting from the unique properties of these copolymers. In the automotive industry, ethylene-octene copolymers are used to manufacture a variety of parts, including bumpers, dashboards, and interior trim components. Their excellent impact resistance and flexibility make them ideal for applications that require durability and the ability to withstand mechanical stress. Additionally, these copolymers contribute to the reduction of vehicle weight, which is crucial for improving fuel efficiency and reducing emissions. In the consumer products sector, ethylene-octene copolymers are used to produce items such as toys, household goods, and personal care products. Their non-toxic nature and ability to be molded into intricate shapes make them suitable for products that come into direct contact with consumers. The wire and cable industry also benefits from the use of ethylene-octene copolymers, particularly in insulation and jacketing applications. These copolymers provide excellent electrical insulation properties, along with resistance to heat, chemicals, and abrasion, ensuring the longevity and safety of cables. In the production of foams and footwear, ethylene-octene copolymers are used to create lightweight, flexible, and comfortable materials. These foams are used in a variety of applications, including cushioning for sports equipment, protective packaging, and insoles for shoes. The packaging industry utilizes ethylene-octene copolymers to produce flexible packaging materials that offer excellent barrier properties, durability, and the ability to be easily processed into films and sheets. This makes them ideal for packaging food, pharmaceuticals, and other sensitive products. Beyond these specific applications, ethylene-octene copolymers are also used in other industries, such as construction, agriculture, and healthcare, where their unique properties provide solutions to various material challenges.

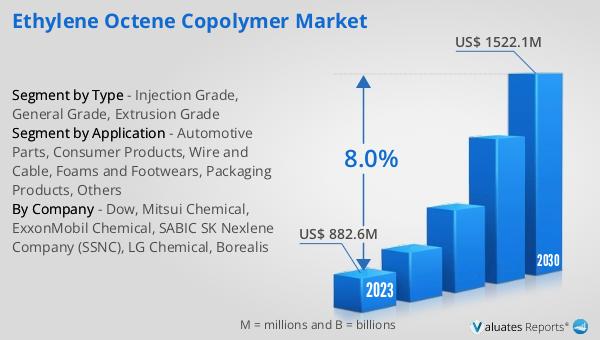

Global Ethylene Octene Copolymer Market Outlook:

The global Ethylene Octene Copolymer market is anticipated to grow significantly, with projections indicating it will reach US$ 1522.1 million by 2030, up from an estimated US$ 959.2 million in 2024, reflecting a compound annual growth rate (CAGR) of 8.0% during the period from 2024 to 2030. Leading companies in this industry include Dow, SABIC, SK Nexlene Company, SSNC, and LG Chemical, which collectively accounted for substantial portions of their revenues in 2019, specifically 55.29%, 17.83%, and 7.57%, respectively. In terms of regional distribution, China held the largest market share by value, reaching 35.6 percent in 2019. This growth is driven by the increasing demand for high-performance materials across various industries, advancements in polymer technology, and the rising need for lightweight and durable materials. The market's expansion is also supported by the continuous development of new applications and the enhancement of existing ones, ensuring that ethylene-octene copolymers remain a vital material in numerous industrial sectors.

| Report Metric | Details |

| Report Name | Ethylene Octene Copolymer Market |

| Accounted market size in 2024 | an estimated US$ 959.2 million |

| Forecasted market size in 2030 | US$ 1522.1 million |

| CAGR | 8.0% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Dow, Mitsui Chemical, ExxonMobil Chemical, SABIC SK Nexlene Company (SSNC), LG Chemical, Borealis |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |