What is Global Hydro Anthracites Market?

The Global Hydro Anthracites Market refers to the worldwide industry focused on the production, distribution, and utilization of hydro anthracites. Hydro anthracites are a type of anthracite coal that has been processed to enhance its filtration properties, making it an essential component in various water treatment applications. This market encompasses a wide range of activities, from mining and refining anthracite coal to manufacturing and distributing hydro anthracite products. The demand for hydro anthracites is driven by their effectiveness in removing impurities from water, making them crucial for industries and municipalities that require high-quality water treatment solutions. The market is influenced by factors such as environmental regulations, technological advancements, and the increasing need for clean water across the globe. As water scarcity and pollution continue to be pressing global issues, the importance of efficient water treatment solutions like hydro anthracites is expected to grow, driving the market forward.

0.6 – 1.6 mm, 1.4 – 2.5 mm, 2.0 – 4.0 mm, 4.0 – 8.0 mm in the Global Hydro Anthracites Market:

In the Global Hydro Anthracites Market, the different size ranges of hydro anthracites, such as 0.6 – 1.6 mm, 1.4 – 2.5 mm, 2.0 – 4.0 mm, and 4.0 – 8.0 mm, play a crucial role in determining their specific applications and effectiveness in water treatment processes. The 0.6 – 1.6 mm size range is typically used for fine filtration, where it helps in removing smaller particles and impurities from water. This size range is particularly effective in applications that require high precision and thorough filtration, such as in the treatment of drinking water and in certain industrial processes where water purity is critical. The 1.4 – 2.5 mm size range is often used in intermediate filtration stages, providing a balance between fine and coarse filtration. This size range is versatile and can be used in a variety of water treatment applications, including municipal water treatment and swimming pool water treatment, where it helps in maintaining water clarity and quality. The 2.0 – 4.0 mm size range is generally used for coarse filtration, where it is effective in removing larger particles and sediments from water. This size range is commonly used in waste-water treatment and industrial water treatment processes, where the removal of larger contaminants is necessary to protect downstream equipment and processes. The 4.0 – 8.0 mm size range is used for very coarse filtration and is effective in applications where the removal of large particles and debris is required. This size range is often used in the initial stages of water treatment processes, where it helps in reducing the load on subsequent filtration stages and improving overall system efficiency. Each size range of hydro anthracites has its own unique properties and advantages, making them suitable for different water treatment applications. The choice of size range depends on the specific requirements of the water treatment process, including the type and size of contaminants to be removed, the desired level of water purity, and the overall system design. By selecting the appropriate size range of hydro anthracites, water treatment professionals can optimize the performance and efficiency of their filtration systems, ensuring the delivery of clean and safe water for various applications.

Drinking Water Treatment, Swimming pool Water Treatment, Waste-Water Treatment, Industrial Water Treatment, Municipal Water Treatment, Others in the Global Hydro Anthracites Market:

The Global Hydro Anthracites Market finds extensive usage in various water treatment applications, including drinking water treatment, swimming pool water treatment, waste-water treatment, industrial water treatment, and municipal water treatment. In drinking water treatment, hydro anthracites are used to remove impurities and contaminants from water, ensuring that it is safe for human consumption. The fine filtration properties of hydro anthracites make them effective in removing particles, sediments, and other impurities, resulting in clean and clear drinking water. In swimming pool water treatment, hydro anthracites are used to maintain water clarity and quality by removing debris, particles, and other contaminants. This helps in ensuring a safe and enjoyable swimming experience for pool users. In waste-water treatment, hydro anthracites are used to remove large particles and sediments from water, protecting downstream equipment and processes from damage and ensuring the efficient operation of the treatment system. In industrial water treatment, hydro anthracites are used to remove impurities and contaminants from water used in various industrial processes. This helps in protecting equipment, improving process efficiency, and ensuring the quality of the final product. In municipal water treatment, hydro anthracites are used to treat water supplied to communities and cities, ensuring that it meets the required quality standards for safe and clean water. The versatility and effectiveness of hydro anthracites make them an essential component in various water treatment applications, helping to address the growing need for clean and safe water across the globe.

Global Hydro Anthracites Market Outlook:

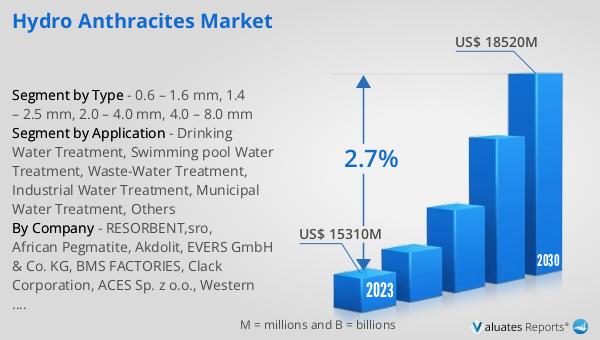

The global Hydro Anthracites market was valued at US$ 15310 million in 2023 and is anticipated to reach US$ 18520 million by 2030, witnessing a CAGR of 2.7% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the hydro anthracites market, driven by the increasing demand for efficient water treatment solutions. The market's growth is influenced by factors such as the rising need for clean water, stringent environmental regulations, and technological advancements in water treatment processes. As the global population continues to grow and industrial activities expand, the demand for high-quality water treatment solutions like hydro anthracites is expected to increase. This market outlook highlights the importance of hydro anthracites in addressing the global water crisis and ensuring the availability of clean and safe water for various applications.

| Report Metric | Details |

| Report Name | Hydro Anthracites Market |

| Accounted market size in 2023 | US$ 15310 million |

| Forecasted market size in 2030 | US$ 18520 million |

| CAGR | 2.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | RESORBENT,sro, African Pegmatite, Akdolit, EVERS GmbH & Co. KG, BMS FACTORIES, Clack Corporation, ACES Sp. z o.o., Western Carbons, Tohkemy Corporation, Pavement Materials Group, Pebblestone Drive |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |