What is Global Reusable Surgical Gown Market?

The Global Reusable Surgical Gown Market refers to the worldwide industry focused on the production, distribution, and utilization of surgical gowns that can be sterilized and reused multiple times. These gowns are essential in maintaining a sterile environment during surgical procedures, protecting both healthcare professionals and patients from infections. Unlike disposable gowns, reusable surgical gowns are designed to withstand multiple cycles of washing and sterilization, making them a more sustainable and cost-effective option in the long run. The market encompasses various types of gowns made from different materials, each offering unique benefits in terms of durability, comfort, and protection. With the increasing emphasis on sustainability and cost-efficiency in healthcare, the demand for reusable surgical gowns is expected to grow, driven by advancements in material technology and stringent infection control protocols. The market is also influenced by factors such as the rising number of surgical procedures, growing awareness about hospital-acquired infections, and the need for high-quality protective apparel in healthcare settings.

PP Non-woven material, SMS Non-woven material, Others in the Global Reusable Surgical Gown Market:

In the Global Reusable Surgical Gown Market, materials play a crucial role in determining the quality and effectiveness of the gowns. One of the primary materials used is PP (Polypropylene) Non-woven material. This material is known for its lightweight, breathable, and water-resistant properties, making it an ideal choice for surgical gowns. PP Non-woven material is also cost-effective and provides a good balance between protection and comfort. It is commonly used in the production of single-use gowns but has also found applications in reusable gowns due to its durability and ease of sterilization. Another significant material in this market is SMS (Spunbond-Meltblown-Spunbond) Non-woven material. SMS is a composite fabric that combines the strengths of spunbond and meltblown layers, offering excellent barrier properties against fluids and microorganisms. The spunbond layers provide strength and durability, while the meltblown layer acts as a filter, enhancing the gown's protective capabilities. SMS Non-woven material is highly regarded for its superior protection, comfort, and breathability, making it a popular choice for high-risk surgical procedures. Additionally, there are other materials used in the production of reusable surgical gowns, such as polyester and cotton blends. These materials are known for their softness, comfort, and ability to withstand multiple washing and sterilization cycles. Polyester, in particular, is valued for its strength, durability, and resistance to shrinking and wrinkling. Cotton blends, on the other hand, offer a natural feel and are highly breathable, ensuring comfort for healthcare professionals during long surgical procedures. The choice of material depends on various factors, including the level of protection required, the type of surgical procedure, and the preferences of healthcare professionals. Each material has its unique advantages and limitations, and manufacturers often use a combination of materials to achieve the desired balance of protection, comfort, and durability. The continuous advancements in material technology are expected to further enhance the performance and usability of reusable surgical gowns, driving their adoption in healthcare settings worldwide.

Hospitals, Ambulatory Surgical Centers, Diagnostic Centers, Clinics, Others in the Global Reusable Surgical Gown Market:

The usage of reusable surgical gowns in various healthcare settings is extensive and multifaceted. In hospitals, these gowns are a staple in operating rooms, where they are used by surgeons, nurses, and other medical staff to maintain a sterile environment during surgical procedures. The gowns provide a barrier against blood, bodily fluids, and other contaminants, reducing the risk of infections. Hospitals benefit from the cost-effectiveness of reusable gowns, as they can be sterilized and reused multiple times, leading to significant savings in the long run. In Ambulatory Surgical Centers (ASCs), which perform outpatient surgeries, reusable surgical gowns are equally important. ASCs often handle a high volume of surgeries, and the use of reusable gowns helps in managing costs while ensuring high standards of infection control. The gowns' durability and ability to withstand repeated sterilization cycles make them a practical choice for these centers. Diagnostic Centers, which conduct various medical tests and procedures, also utilize reusable surgical gowns. These centers require gowns that provide adequate protection during invasive diagnostic procedures, such as biopsies and endoscopies. The use of reusable gowns in diagnostic centers not only ensures patient and staff safety but also aligns with the growing emphasis on sustainable healthcare practices. Clinics, which offer a range of medical services, from minor surgeries to routine check-ups, also rely on reusable surgical gowns. The versatility and cost-effectiveness of these gowns make them suitable for clinics of all sizes. They provide the necessary protection during procedures while being a more environmentally friendly option compared to disposable gowns. Other healthcare settings, such as nursing homes, dental offices, and veterinary clinics, also benefit from the use of reusable surgical gowns. In nursing homes, where residents may require medical care and minor surgical procedures, reusable gowns offer a reliable and cost-effective solution. Dental offices use these gowns during oral surgeries and other invasive procedures to maintain a sterile environment. Veterinary clinics, which perform surgeries on animals, also utilize reusable surgical gowns to ensure the safety of both the animals and the veterinary staff. The widespread adoption of reusable surgical gowns across various healthcare settings underscores their importance in maintaining high standards of infection control while promoting sustainability and cost-efficiency.

Global Reusable Surgical Gown Market Outlook:

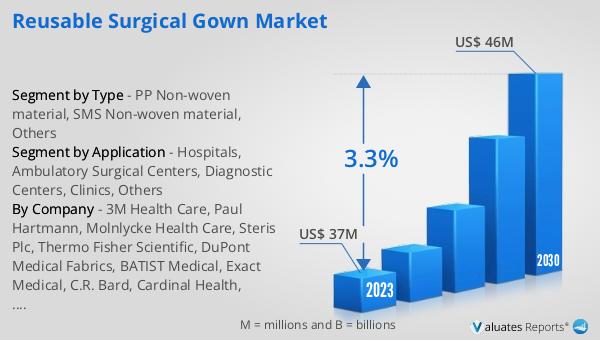

The global market for reusable surgical gowns was valued at $37 million in 2023 and is projected to reach $46 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.3% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for sustainable and cost-effective solutions in healthcare. According to our research, the broader global market for medical devices is estimated at $603 billion in 2023 and is expected to grow at a CAGR of 5% over the next six years. This data highlights the significant role that reusable surgical gowns play within the larger medical device market. The rising awareness about hospital-acquired infections and the need for high-quality protective apparel are key factors driving the growth of the reusable surgical gown market. As healthcare facilities continue to prioritize infection control and sustainability, the demand for reusable surgical gowns is expected to rise, contributing to the overall growth of the medical device market. The advancements in material technology and the increasing emphasis on cost-efficiency are also expected to further propel the market's growth.

| Report Metric | Details |

| Report Name | Reusable Surgical Gown Market |

| Accounted market size in 2023 | US$ 37 million |

| Forecasted market size in 2030 | US$ 46 million |

| CAGR | 3.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | 3M Health Care, Paul Hartmann, Molnlycke Health Care, Steris Plc, Thermo Fisher Scientific, DuPont Medical Fabrics, BATIST Medical, Exact Medical, C.R. Bard, Cardinal Health, Halyard Health, Hartmann, Johnson & Johnson, Lohmann & Rauscher, Medline, Molnlycke, Stryker, Welmed Inc, Biolife, Ecolab, Henry Schein |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |