What is Global Diagnostic Audiometer Market?

The Global Diagnostic Audiometer Market refers to the worldwide industry focused on the production, distribution, and utilization of diagnostic audiometers. These devices are essential tools in the field of audiology, used to evaluate hearing acuity and diagnose hearing loss. Audiometers are employed in various settings, including hospitals, audiology centers, and research institutions, to conduct hearing tests and assess the auditory health of patients. The market encompasses a range of audiometers, from basic models to advanced systems with sophisticated features. The growing prevalence of hearing disorders, coupled with advancements in audiometric technology, has fueled the demand for these devices globally. Additionally, increasing awareness about the importance of early detection and treatment of hearing impairments has further propelled market growth. The Global Diagnostic Audiometer Market is characterized by continuous innovation, with manufacturers striving to develop more accurate, user-friendly, and portable devices to meet the diverse needs of healthcare professionals and patients.

Stand-alone Audiometer, Hybrid Audiometer, PC-Based Audiometer in the Global Diagnostic Audiometer Market:

In the Global Diagnostic Audiometer Market, there are three main types of audiometers: Stand-alone Audiometers, Hybrid Audiometers, and PC-Based Audiometers. Stand-alone Audiometers are independent devices that do not require any external computer or software to operate. They are typically used in clinical settings where portability and ease of use are crucial. These audiometers come with built-in displays and controls, allowing audiologists to perform hearing tests directly on the device. They are highly reliable and often used in environments where quick and efficient testing is needed. Hybrid Audiometers, on the other hand, combine the features of stand-alone and PC-based audiometers. They can function independently or be connected to a computer for enhanced functionality. This versatility makes them suitable for a wide range of applications, from basic hearing assessments to more complex diagnostic procedures. Hybrid audiometers often come with advanced features such as data storage, patient management systems, and integration with electronic health records (EHR). PC-Based Audiometers are designed to work in conjunction with a computer, utilizing specialized software to conduct hearing tests and analyze results. These audiometers offer the highest level of flexibility and customization, as the software can be regularly updated to include new testing protocols and features. PC-based systems are ideal for research settings and advanced clinical applications where detailed analysis and comprehensive data management are required. They also allow for remote testing and tele-audiology, expanding access to hearing care services. Each type of audiometer has its unique advantages and is chosen based on the specific needs of the healthcare provider and the patient population they serve. The continuous development and integration of new technologies in these devices ensure that the Global Diagnostic Audiometer Market remains dynamic and responsive to the evolving demands of the audiology field.

Hospitals, Audiology Centers, Research Communities in the Global Diagnostic Audiometer Market:

The usage of diagnostic audiometers in hospitals, audiology centers, and research communities is integral to the effective management and treatment of hearing disorders. In hospitals, diagnostic audiometers are essential tools in the ENT (Ear, Nose, and Throat) departments. They are used to conduct routine hearing screenings, diagnose various types of hearing loss, and monitor the auditory health of patients undergoing treatments that may affect hearing, such as chemotherapy. Hospitals often rely on advanced audiometers with comprehensive testing capabilities to ensure accurate diagnosis and effective treatment planning. Audiology centers, which specialize in hearing care, utilize diagnostic audiometers extensively for both diagnostic and rehabilitative purposes. These centers conduct detailed hearing assessments to identify the type and degree of hearing loss, allowing audiologists to recommend appropriate interventions such as hearing aids, cochlear implants, or other assistive listening devices. Audiology centers often use a combination of stand-alone, hybrid, and PC-based audiometers to cater to the diverse needs of their patients. In research communities, diagnostic audiometers play a crucial role in advancing the understanding of auditory health and hearing disorders. Researchers use these devices to conduct studies on hearing loss prevalence, the effectiveness of various treatments, and the impact of environmental factors on hearing health. PC-based audiometers are particularly valuable in research settings due to their ability to provide detailed data analysis and support complex testing protocols. The integration of diagnostic audiometers in these areas ensures that patients receive timely and accurate hearing assessments, leading to better outcomes and improved quality of life.

Global Diagnostic Audiometer Market Outlook:

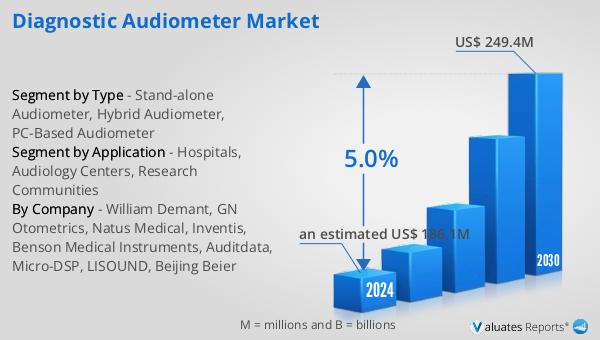

The global Diagnostic Audiometer market is anticipated to grow significantly, with projections indicating it will reach approximately US$ 249.4 million by 2030, up from an estimated US$ 186.1 million in 2024. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.0% between 2024 and 2030. Europe is a notable region within this market, holding a revenue market share of 26%. This growth can be attributed to several factors, including the increasing prevalence of hearing disorders, advancements in audiometric technology, and heightened awareness about the importance of early detection and treatment of hearing impairments. The market's expansion is also driven by the continuous innovation from manufacturers who are developing more accurate, user-friendly, and portable diagnostic audiometers to meet the diverse needs of healthcare professionals and patients. As the demand for effective hearing assessment tools continues to rise, the Global Diagnostic Audiometer Market is poised to play a crucial role in improving auditory health outcomes worldwide.

| Report Metric | Details |

| Report Name | Diagnostic Audiometer Market |

| Accounted market size in 2024 | an estimated US$ 186.1 million |

| Forecasted market size in 2030 | US$ 249.4 million |

| CAGR | 5.0% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | William Demant, GN Otometrics, Natus Medical, Inventis, Benson Medical Instruments, Auditdata, Micro-DSP, LISOUND, Beijing Beier |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |