What is Global Glass Mat Thermoplastics (GMT) Market?

The global Glass Mat Thermoplastics (GMT) market is a specialized segment within the broader thermoplastics industry. GMTs are composite materials made by combining glass fibers with thermoplastic resins, resulting in a product that is both lightweight and highly durable. These materials are particularly valued for their excellent mechanical properties, including high impact resistance and stiffness, making them suitable for a variety of demanding applications. GMTs are used in industries such as automotive, construction, and marine, where their unique properties can significantly enhance performance and longevity. The market for GMTs is driven by the increasing demand for lightweight and high-strength materials, particularly in the automotive sector, where reducing vehicle weight is crucial for improving fuel efficiency and reducing emissions. Additionally, advancements in manufacturing technologies and the development of new resin formulations are expected to further boost the adoption of GMTs across various industries. The global GMT market is characterized by a high level of competition, with several key players continuously innovating to maintain their market positions.

Polypropylene (PP) GMT, Polyamide (PA) GMT, Others in the Global Glass Mat Thermoplastics (GMT) Market:

Polypropylene (PP) GMT, Polyamide (PA) GMT, and other types of GMTs each have distinct characteristics and applications within the global Glass Mat Thermoplastics (GMT) market. Polypropylene (PP) GMT is the most widely used type, primarily due to its excellent balance of mechanical properties, cost-effectiveness, and ease of processing. PP GMTs are known for their high impact resistance, good chemical resistance, and low density, making them ideal for automotive applications such as bumper beams, underbody shields, and interior components. The lightweight nature of PP GMTs helps in reducing the overall weight of vehicles, thereby enhancing fuel efficiency and reducing emissions. Polyamide (PA) GMT, on the other hand, offers superior mechanical properties compared to PP GMT. PA GMTs are characterized by their high strength, stiffness, and thermal stability, making them suitable for more demanding applications where higher performance is required. These materials are often used in automotive structural components, electrical housings, and under-the-hood applications where exposure to high temperatures and harsh environments is common. The superior performance of PA GMTs comes at a higher cost, which limits their use to applications where their unique properties are essential. Other types of GMTs include those made with different thermoplastic resins such as polycarbonate (PC), polyphenylene sulfide (PPS), and polyethylene terephthalate (PET). These GMTs are used in specialized applications where specific properties such as flame retardancy, chemical resistance, or transparency are required. For instance, PC GMTs are used in applications requiring high impact resistance and optical clarity, such as in the construction of safety helmets and transparent panels. PPS GMTs are known for their excellent chemical resistance and high-temperature performance, making them suitable for applications in the chemical processing and electronics industries. PET GMTs, with their good mechanical properties and recyclability, are used in applications such as packaging and consumer goods. The choice of resin in GMTs is largely determined by the specific requirements of the application, including mechanical performance, environmental resistance, and cost considerations. The global GMT market is continuously evolving, with ongoing research and development efforts aimed at improving the performance and expanding the applications of these materials. Innovations in resin formulations, fiber reinforcements, and manufacturing processes are expected to drive the growth of the GMT market, enabling the development of new and improved products that meet the ever-changing demands of various industries.

Automotive, Building and Construction, Marine, Others in the Global Glass Mat Thermoplastics (GMT) Market:

The usage of Global Glass Mat Thermoplastics (GMT) in various sectors such as automotive, building and construction, marine, and others highlights the versatility and high performance of these materials. In the automotive industry, GMTs are extensively used due to their lightweight and high-strength properties. They are employed in manufacturing various components such as bumper beams, underbody shields, and interior parts. The use of GMTs in automotive applications helps in reducing the overall weight of vehicles, which in turn improves fuel efficiency and reduces emissions. Additionally, GMTs offer excellent impact resistance and durability, making them ideal for safety-critical components. In the building and construction sector, GMTs are used in applications such as roofing, cladding, and structural components. Their high strength-to-weight ratio, corrosion resistance, and ease of installation make them suitable for use in both residential and commercial buildings. GMTs are also used in the construction of bridges, tunnels, and other infrastructure projects where their durability and resistance to environmental factors are crucial. In the marine industry, GMTs are used in the construction of boat hulls, decks, and other structural components. The lightweight nature of GMTs helps in improving the fuel efficiency and performance of marine vessels. Additionally, GMTs offer excellent resistance to water and corrosion, making them ideal for use in harsh marine environments. Other applications of GMTs include their use in the production of consumer goods, sports equipment, and industrial components. The versatility of GMTs, combined with their excellent mechanical properties, makes them suitable for a wide range of applications across various industries. The continuous advancements in manufacturing technologies and the development of new resin formulations are expected to further expand the usage of GMTs in different sectors, driving the growth of the global GMT market.

Global Glass Mat Thermoplastics (GMT) Market Outlook:

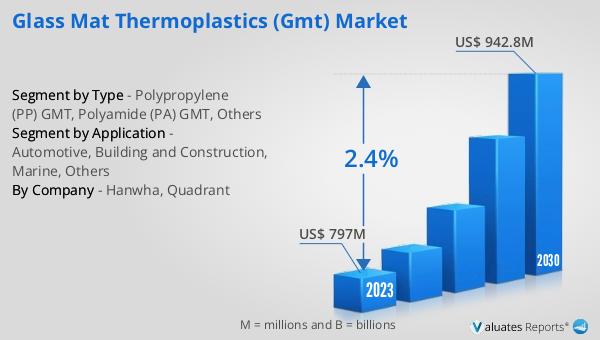

The global Glass Mat Thermoplastics (GMT) market is anticipated to grow from an estimated US$ 817.8 million in 2024 to US$ 942.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 2.4% during the forecast period from 2024 to 2030. Key manufacturers in the GMT market, such as Hanwha and Quadrant, dominate the industry, accounting for approximately 70% and 30% of the market share, respectively. Europe stands out as the largest regional market, holding a share of over 46%. Among the different types of GMTs, Polypropylene (PP) GMT is the most prevalent, capturing a significant share of over 92%. The automotive sector is the largest end-user segment for GMTs, also holding a share of over 92%. This dominance is driven by the increasing demand for lightweight and high-strength materials in the automotive industry, aimed at improving fuel efficiency and reducing emissions. The continuous advancements in manufacturing technologies and the development of new resin formulations are expected to further boost the adoption of GMTs across various industries, driving the growth of the global GMT market.

| Report Metric | Details |

| Report Name | Glass Mat Thermoplastics (GMT) Market |

| Accounted market size in 2024 | an estimated US$ 817.8 million |

| Forecasted market size in 2030 | US$ 942.8 million |

| CAGR | 2.4% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Hanwha, Quadrant |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |