What is Global Wire Drawing Lubricants Market?

The Global Wire Drawing Lubricants Market is a specialized segment within the broader industrial lubricants market. Wire drawing lubricants are essential in the wire drawing process, which involves reducing the diameter of a wire by pulling it through a series of dies. These lubricants play a crucial role in minimizing friction and heat generation, thereby extending the life of the dies and improving the quality of the finished wire. The market for these lubricants is driven by the demand from various industries such as automotive, construction, and electronics, which require high-quality wires for their applications. The global market is characterized by a mix of established players and new entrants, each offering a range of products tailored to specific wire drawing needs. The market is also influenced by technological advancements and the increasing focus on sustainable and eco-friendly lubricants. As industries continue to evolve, the demand for efficient and effective wire drawing lubricants is expected to grow, making this a dynamic and competitive market.

Dry Wire Drawing Lubricants, Wet Wire Drawing Lubricants in the Global Wire Drawing Lubricants Market:

Dry wire drawing lubricants and wet wire drawing lubricants are two primary types of lubricants used in the wire drawing process, each with its unique characteristics and applications. Dry wire drawing lubricants are typically in powder form and are applied to the wire before it enters the drawing die. These lubricants are particularly effective in high-speed drawing operations and are commonly used for drawing ferrous and non-ferrous wires. They provide excellent lubrication and cooling properties, which help in reducing friction and wear on the dies. Dry lubricants are also preferred for their ease of application and removal, making them suitable for a wide range of wire drawing operations. On the other hand, wet wire drawing lubricants are liquid-based and are applied to the wire during the drawing process. These lubricants are often used in conjunction with cooling systems to maintain optimal temperatures and prevent overheating. Wet lubricants are particularly effective in drawing fine wires and are commonly used in applications where high surface finish and precision are required. They offer superior cooling and lubrication properties, which help in achieving high-quality wire surfaces and reducing the risk of wire breakage. Both dry and wet wire drawing lubricants have their advantages and are chosen based on the specific requirements of the wire drawing operation. The choice between dry and wet lubricants depends on factors such as the type of wire being drawn, the drawing speed, and the desired surface finish. In the global wire drawing lubricants market, dry wire drawing lubricants hold a significant share due to their versatility and effectiveness in various applications. However, wet wire drawing lubricants are also gaining traction, especially in applications that require high precision and surface quality. As the demand for high-quality wires continues to grow, the market for both dry and wet wire drawing lubricants is expected to expand, driven by advancements in lubricant formulations and the increasing focus on sustainability and environmental compliance.

Carbon Steel Wire, Stainless Steel Wire, Tire Bead & Cord, Galvanized Wire, Aluminum & Alloy Wires, Copper Wires, Other Applications in the Global Wire Drawing Lubricants Market:

The usage of global wire drawing lubricants spans across various applications, including carbon steel wire, stainless steel wire, tire bead & cord, galvanized wire, aluminum & alloy wires, copper wires, and other specialized applications. In the case of carbon steel wire, wire drawing lubricants are essential for reducing friction and wear during the drawing process, ensuring the production of high-strength and durable wires used in construction, automotive, and industrial applications. For stainless steel wire, lubricants play a crucial role in maintaining the wire's surface quality and preventing oxidation, which is vital for applications in the medical, aerospace, and food processing industries. Tire bead & cord applications require lubricants that can withstand high drawing speeds and provide excellent cooling properties to ensure the production of strong and flexible wires used in tire manufacturing. Galvanized wire applications benefit from lubricants that offer superior corrosion resistance and surface finish, making them suitable for use in fencing, electrical conductors, and other outdoor applications. Aluminum & alloy wires require lubricants that can handle the unique properties of these materials, ensuring smooth drawing operations and high-quality wire surfaces for use in electrical, automotive, and aerospace industries. Copper wires, widely used in electrical and electronic applications, require lubricants that provide excellent conductivity and surface finish, ensuring the production of high-performance wires for use in power transmission, telecommunications, and electronic devices. Other specialized applications of wire drawing lubricants include the production of fine wires for use in medical devices, precision instruments, and other high-tech applications. In each of these applications, the choice of lubricant is critical to achieving the desired wire properties and performance. The global wire drawing lubricants market continues to evolve, driven by the increasing demand for high-quality wires across various industries and the ongoing advancements in lubricant formulations and technologies.

Global Wire Drawing Lubricants Market Outlook:

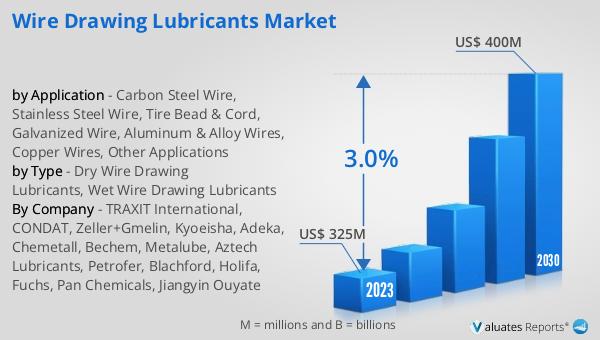

The global Wire Drawing Lubricants market is anticipated to grow from an estimated US$ 279.1 million in 2024 to US$ 327.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 2.7% during the forecast period from 2024 to 2030. The market is highly competitive, with the top two players accounting for approximately 43% of the total global market share. Among the different types of wire drawing lubricants, dry wire drawing lubricants dominate the market, holding about 60% of the total market share. This significant share can be attributed to the versatility and effectiveness of dry lubricants in various wire drawing applications. The market's growth is driven by the increasing demand for high-quality wires in industries such as automotive, construction, and electronics, which require efficient and effective lubrication solutions to ensure optimal wire drawing performance. As the market continues to evolve, the focus on sustainable and eco-friendly lubricants is expected to drive further innovations and advancements in lubricant formulations, contributing to the overall growth of the global wire drawing lubricants market.

| Report Metric | Details |

| Report Name | Wire Drawing Lubricants Market |

| Accounted market size in 2024 | an estimated US$ 279.1 million |

| Forecasted market size in 2030 | US$ 327.5 million |

| CAGR | 2.7% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | TRAXIT International, CONDAT, Zeller+Gmelin, Kyoeisha, Adeka, Chemetall, Bechem, Metalube, Aztech Lubricants, Petrofer, Blachford, Holifa, Fuchs, Pan Chemicals, Jiangyin Ouyate |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |