What is Global Glass Droppers Market?

The Global Glass Droppers Market refers to the worldwide industry involved in the production, distribution, and sale of glass droppers. These droppers are small, precision tools used to dispense liquids in controlled amounts. They are commonly made from high-quality glass to ensure durability and chemical resistance. Glass droppers are widely used in various sectors, including pharmaceuticals, cosmetics, essential oils, and homeopathic remedies. The market encompasses a range of dropper sizes and designs to cater to different applications and consumer needs. The demand for glass droppers is driven by their precision, safety, and the growing awareness of the benefits of using glass over plastic due to environmental concerns. The market is characterized by a mix of established manufacturers and new entrants, all striving to innovate and meet the evolving needs of consumers. The global reach of this market means that trends and demands can vary significantly from one region to another, influenced by local regulations, consumer preferences, and industry standards.

Up to 2 ml, 2 ml – 6 ml, 6 ml – 10 ml, Above 10 ml in the Global Glass Droppers Market:

In the Global Glass Droppers Market, the products are categorized based on their capacity, which includes Up to 2 ml, 2 ml – 6 ml, 6 ml – 10 ml, and Above 10 ml. Each category serves different purposes and caters to various industries. Droppers with a capacity of Up to 2 ml are typically used for applications requiring very small, precise amounts of liquid, such as in pharmaceuticals for administering medication or in cosmetics for applying serums and essential oils. These small droppers are favored for their accuracy and ease of use, making them ideal for products that require careful dosage. The 2 ml – 6 ml range is versatile and commonly used in both pharmaceuticals and cosmetics. This size is suitable for products like eye drops, ear drops, and facial oils, providing a balance between portability and sufficient volume for multiple uses. Droppers in the 6 ml – 10 ml range are often used for products that need a slightly larger volume, such as certain medicinal syrups, larger cosmetic bottles, and essential oil blends. These droppers offer a good compromise between size and capacity, making them practical for both personal and professional use. Finally, droppers with a capacity Above 10 ml are used for products that require larger quantities of liquid, such as bulk essential oils, homeopathic remedies, and certain pharmaceutical preparations. These larger droppers are designed to handle more substantial volumes while still providing the precision and control needed for accurate dispensing. Each capacity category in the Global Glass Droppers Market addresses specific needs and preferences, ensuring that there is a suitable option for every application.

Pharmaceutical, Cosmetics, Essential Oils, Homeopathic in the Global Glass Droppers Market:

The usage of glass droppers in the Global Glass Droppers Market spans several key areas, including pharmaceuticals, cosmetics, essential oils, and homeopathic remedies. In the pharmaceutical industry, glass droppers are essential for administering precise doses of liquid medications, such as eye drops, ear drops, and certain oral medications. Their accuracy and chemical resistance make them ideal for ensuring that patients receive the correct dosage without contamination. In the cosmetics industry, glass droppers are widely used for products like facial serums, oils, and other skincare treatments. The ability to dispense small, controlled amounts of product helps consumers apply these often expensive and potent formulations efficiently and hygienically. Essential oils, known for their therapeutic properties, also rely heavily on glass droppers. These droppers allow users to measure and dispense the oils accurately, whether for aromatherapy, topical application, or blending with other oils. The use of glass ensures that the oils remain pure and uncontaminated, preserving their efficacy. In homeopathic medicine, glass droppers are used to dispense liquid remedies that require precise dosing. Homeopathic treatments often involve highly diluted substances, making the accuracy of glass droppers crucial for effective administration. Across all these areas, the use of glass droppers enhances the user experience by providing precision, safety, and reliability.

Global Glass Droppers Market Outlook:

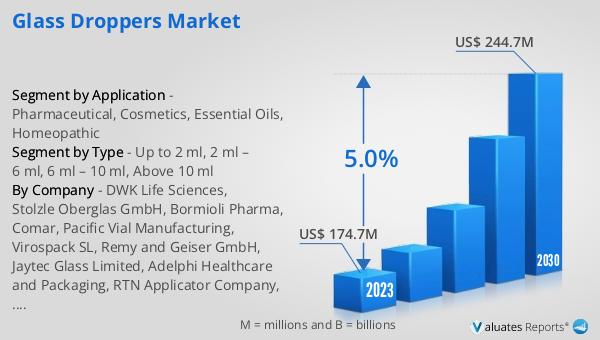

The global Glass Droppers market was valued at US$ 174.7 million in 2023 and is anticipated to reach US$ 244.7 million by 2030, witnessing a CAGR of 5.0% during the forecast period 2024-2030. This growth reflects the increasing demand for glass droppers across various industries, driven by their precision, safety, and environmental benefits. The market's expansion is supported by the rising awareness of the advantages of using glass over plastic, particularly in sectors like pharmaceuticals, cosmetics, essential oils, and homeopathic remedies. As consumers become more conscious of the environmental impact of plastic, the preference for glass droppers is expected to continue growing. This trend is further bolstered by innovations in dropper design and manufacturing, which enhance their functionality and appeal. The market's steady growth underscores the importance of glass droppers in ensuring accurate and safe dispensing of liquids, making them an indispensable tool in many applications.

| Report Metric | Details |

| Report Name | Glass Droppers Market |

| Accounted market size in 2023 | US$ 174.7 million |

| Forecasted market size in 2030 | US$ 244.7 million |

| CAGR | 5.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | DWK Life Sciences, Stolzle Oberglas GmbH, Bormioli Pharma, Comar, Pacific Vial Manufacturing, Virospack SL, Remy and Geiser GmbH, Jaytec Glass Limited, Adelphi Healthcare and Packaging, RTN Applicator Company, The Plasticoid Company, UD Pharma Rubber Products |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |