What is Global Automotive Brake System and Components Market?

The Global Automotive Brake System and Components Market encompasses a wide range of products and technologies designed to ensure the safety and performance of vehicles. This market includes various types of brake systems such as disc brakes, drum brakes, and other advanced braking technologies. These components are essential for the effective functioning of vehicles, providing the necessary stopping power and control. The market is driven by the increasing demand for vehicles, advancements in automotive technology, and stringent safety regulations. Manufacturers in this market are continuously innovating to develop more efficient and reliable braking systems. The market is also influenced by factors such as the growing popularity of electric and hybrid vehicles, which require specialized braking systems. Overall, the Global Automotive Brake System and Components Market plays a crucial role in the automotive industry, ensuring the safety and reliability of vehicles on the road.

Disc Brake, Drum Brake, Others in the Global Automotive Brake System and Components Market:

Disc brakes, drum brakes, and other types of braking systems are integral components of the Global Automotive Brake System and Components Market. Disc brakes are widely used in modern vehicles due to their superior performance and efficiency. They consist of a brake disc, caliper, and brake pads. When the brake pedal is pressed, hydraulic fluid forces the caliper to squeeze the brake pads against the disc, creating friction that slows down the vehicle. Disc brakes are known for their ability to dissipate heat quickly, making them ideal for high-performance and heavy-duty applications. On the other hand, drum brakes are more commonly found in older vehicles and some modern vehicles' rear wheels. They consist of a brake drum, brake shoes, and wheel cylinder. When the brake pedal is pressed, hydraulic fluid pushes the brake shoes against the drum, creating friction that slows down the vehicle. Drum brakes are generally less expensive to manufacture and maintain but are not as efficient as disc brakes in terms of heat dissipation and stopping power. Other types of braking systems in the market include regenerative braking systems, which are commonly used in electric and hybrid vehicles. These systems convert the kinetic energy generated during braking into electrical energy, which is then stored in the vehicle's battery. This not only improves the vehicle's efficiency but also reduces wear and tear on the braking components. Additionally, advanced braking technologies such as anti-lock braking systems (ABS), electronic stability control (ESC), and brake-by-wire systems are becoming increasingly popular. ABS prevents the wheels from locking up during hard braking, ensuring better control and stability. ESC helps maintain the vehicle's stability by automatically applying brakes to individual wheels when necessary. Brake-by-wire systems replace traditional hydraulic braking systems with electronic controls, offering more precise and responsive braking. Overall, the Global Automotive Brake System and Components Market is characterized by a wide range of products and technologies, each with its own advantages and applications.

Passenger Car, Commercial Car in the Global Automotive Brake System and Components Market:

The usage of Global Automotive Brake System and Components Market in passenger cars and commercial vehicles is essential for ensuring safety and performance. In passenger cars, braking systems are designed to provide a smooth and comfortable driving experience while ensuring the safety of the occupants. Disc brakes are commonly used in passenger cars due to their superior performance and efficiency. They offer better stopping power and heat dissipation, making them ideal for high-speed and high-performance vehicles. Additionally, advanced braking technologies such as ABS and ESC are widely used in passenger cars to enhance safety and control. ABS prevents the wheels from locking up during hard braking, ensuring better control and stability. ESC helps maintain the vehicle's stability by automatically applying brakes to individual wheels when necessary. These technologies are especially important in passenger cars, where safety and comfort are top priorities. In commercial vehicles, braking systems are designed to handle heavier loads and more demanding driving conditions. Drum brakes are commonly used in commercial vehicles due to their durability and cost-effectiveness. They are capable of handling the high loads and frequent braking required in commercial applications. However, disc brakes are also becoming increasingly popular in commercial vehicles due to their superior performance and efficiency. Advanced braking technologies such as ABS and ESC are also widely used in commercial vehicles to enhance safety and control. ABS prevents the wheels from locking up during hard braking, ensuring better control and stability. ESC helps maintain the vehicle's stability by automatically applying brakes to individual wheels when necessary. Additionally, regenerative braking systems are becoming more common in commercial vehicles, especially in electric and hybrid models. These systems convert the kinetic energy generated during braking into electrical energy, which is then stored in the vehicle's battery. This not only improves the vehicle's efficiency but also reduces wear and tear on the braking components. Overall, the usage of Global Automotive Brake System and Components Market in passenger cars and commercial vehicles is essential for ensuring safety, performance, and efficiency.

Global Automotive Brake System and Components Market Outlook:

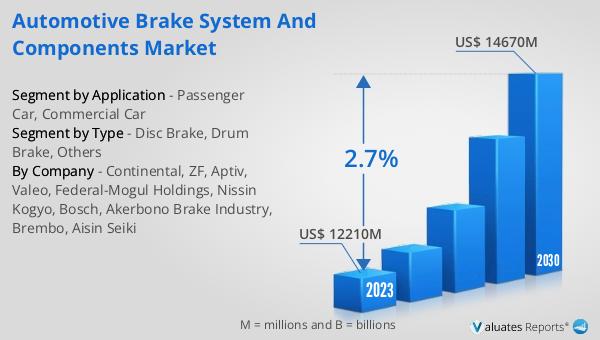

The global Automotive Brake System and Components market was valued at US$ 12,210 million in 2023 and is anticipated to reach US$ 14,670 million by 2030, witnessing a CAGR of 2.7% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the automotive brake system and components industry. The increasing demand for vehicles, advancements in automotive technology, and stringent safety regulations are some of the key factors driving this growth. Manufacturers are continuously innovating to develop more efficient and reliable braking systems, which is expected to further boost the market. The growing popularity of electric and hybrid vehicles, which require specialized braking systems, is also contributing to the market's growth. Additionally, the adoption of advanced braking technologies such as ABS, ESC, and brake-by-wire systems is expected to drive the market. These technologies offer enhanced safety and control, making them increasingly popular among consumers. Overall, the global Automotive Brake System and Components market is expected to witness steady growth in the coming years, driven by increasing demand, technological advancements, and stringent safety regulations.

| Report Metric | Details |

| Report Name | Automotive Brake System and Components Market |

| Accounted market size in 2023 | US$ 12210 million |

| Forecasted market size in 2030 | US$ 14670 million |

| CAGR | 2.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Continental, ZF, Aptiv, Valeo, Federal-Mogul Holdings, Nissin Kogyo, Bosch, Akerbono Brake Industry, Brembo, Aisin Seiki |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |