What is Global Wood TV Cabinet Market?

The Global Wood TV Cabinet Market refers to the worldwide industry involved in the production, distribution, and sale of TV cabinets made from wood. These cabinets are essential pieces of furniture designed to support and house television sets, along with other entertainment equipment such as gaming consoles, DVD players, and sound systems. The market encompasses a wide range of styles, sizes, and finishes to cater to diverse consumer preferences and interior design trends. Wood TV cabinets are favored for their durability, aesthetic appeal, and ability to blend seamlessly with various home decor styles. The market includes both mass-produced and custom-made options, with manufacturers and retailers operating at local, regional, and international levels. Factors such as rising disposable incomes, increasing urbanization, and the growing trend of home entertainment systems are driving the demand for wood TV cabinets globally. Additionally, the market is influenced by changing consumer preferences towards eco-friendly and sustainable furniture options, leading to innovations in materials and production processes.

Wall-mounted, Floor-mounted in the Global Wood TV Cabinet Market:

In the Global Wood TV Cabinet Market, there are primarily two types of installations: wall-mounted and floor-mounted cabinets. Wall-mounted wood TV cabinets are designed to be affixed directly to the wall, offering a sleek and modern look that saves floor space and provides a clean, uncluttered appearance. These cabinets are particularly popular in contemporary and minimalist interior designs, where the emphasis is on maximizing space and creating an open, airy feel. Wall-mounted cabinets often come with additional features such as cable management systems, adjustable shelves, and integrated lighting to enhance functionality and aesthetics. They are ideal for smaller living spaces, apartments, and homes where floor space is at a premium. On the other hand, floor-mounted wood TV cabinets are traditional pieces of furniture that rest on the floor and provide ample storage space for various entertainment equipment and accessories. These cabinets are available in a wide range of styles, from classic and rustic to modern and industrial, catering to different tastes and preferences. Floor-mounted cabinets are known for their sturdiness and ability to support larger and heavier television sets. They often come with multiple compartments, drawers, and shelves, offering versatile storage solutions for media collections, gaming consoles, and other electronic devices. The choice between wall-mounted and floor-mounted wood TV cabinets largely depends on the available space, interior design style, and personal preferences of the consumers. Both types have their unique advantages and can significantly enhance the functionality and aesthetics of a living room or entertainment area. Manufacturers in the Global Wood TV Cabinet Market are continually innovating to offer a diverse range of products that meet the evolving needs and preferences of consumers. This includes the use of sustainable materials, advanced manufacturing techniques, and customizable options to cater to the growing demand for eco-friendly and personalized furniture solutions.

Commercial, Household in the Global Wood TV Cabinet Market:

The usage of wood TV cabinets in commercial and household settings varies significantly, reflecting the diverse needs and preferences of different consumer segments. In commercial settings, wood TV cabinets are commonly found in hotels, offices, restaurants, and retail stores. In hotels, these cabinets are used to enhance the aesthetic appeal of guest rooms and provide a functional solution for housing televisions and other entertainment equipment. They are often designed to match the overall decor of the room, offering a cohesive and stylish look. In offices, wood TV cabinets are used in conference rooms and break areas to support televisions used for presentations, video conferencing, and employee entertainment. Restaurants and retail stores also utilize wood TV cabinets to create an inviting atmosphere for customers, displaying promotional content, menus, or entertainment programs. The durability and aesthetic appeal of wood make it a preferred choice for commercial applications, where the furniture needs to withstand frequent use and complement the interior design. In household settings, wood TV cabinets serve as a central piece of furniture in living rooms, family rooms, and bedrooms. They provide a practical solution for organizing and storing entertainment equipment, media collections, and other accessories. Wood TV cabinets are available in various styles, sizes, and finishes, allowing homeowners to choose a piece that matches their interior decor and personal preferences. In addition to their functional benefits, wood TV cabinets add warmth and character to a home, creating a cozy and inviting atmosphere. They are often chosen for their durability and timeless appeal, making them a long-lasting investment for homeowners. The versatility of wood TV cabinets allows them to be used in different rooms and settings, offering a flexible and stylish solution for modern homes. Overall, the usage of wood TV cabinets in both commercial and household settings highlights their importance as a functional and aesthetic piece of furniture that enhances the overall experience of the space.

Global Wood TV Cabinet Market Outlook:

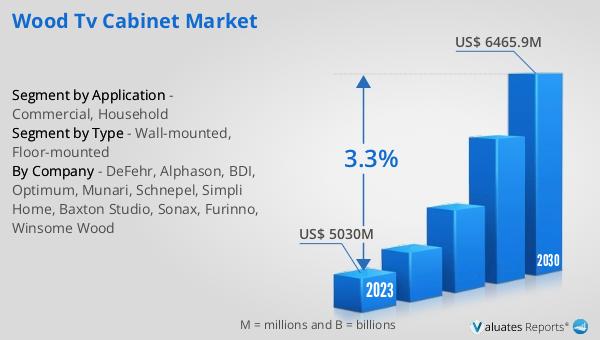

The global Wood TV Cabinet market was valued at US$ 5030 million in 2023 and is anticipated to reach US$ 6465.9 million by 2030, witnessing a CAGR of 3.3% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the wood TV cabinet industry, driven by factors such as increasing consumer demand for stylish and functional furniture, rising disposable incomes, and the growing trend of home entertainment systems. The market's valuation reflects the significant role that wood TV cabinets play in both residential and commercial settings, offering a blend of durability, aesthetic appeal, and practicality. As consumers continue to seek eco-friendly and sustainable furniture options, the wood TV cabinet market is expected to witness further innovations in materials and design, catering to the evolving preferences of a global audience. The projected growth in market value underscores the importance of wood TV cabinets as a key component of modern interior design, providing versatile and stylish solutions for organizing and displaying entertainment equipment.

| Report Metric | Details |

| Report Name | Wood TV Cabinet Market |

| Accounted market size in 2023 | US$ 5030 million |

| Forecasted market size in 2030 | US$ 6465.9 million |

| CAGR | 3.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | DeFehr, Alphason, BDI, Optimum, Munari, Schnepel, Simpli Home, Baxton Studio, Sonax, Furinno, Winsome Wood |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |