What is Global Railway Connectors Market?

The Global Railway Connectors Market refers to the industry that produces and supplies connectors specifically designed for railway applications. These connectors are crucial components in the railway system, ensuring reliable and efficient electrical and data connections between various parts of the train and railway infrastructure. They are used in a wide range of applications, including traction systems, signaling and control systems, lighting and electrical systems, and data communication. The market for railway connectors is driven by the increasing demand for advanced and reliable railway systems, the need for efficient and safe transportation, and the growing investments in railway infrastructure across the globe. The market is characterized by the presence of several key players who offer a variety of connectors designed to meet the specific requirements of the railway industry. These connectors are designed to withstand harsh environmental conditions, including extreme temperatures, vibrations, and mechanical stresses, ensuring the safety and reliability of railway operations. The market is also influenced by technological advancements, such as the development of high-speed trains and the integration of advanced communication and control systems, which require more sophisticated and reliable connectors.

Plug and Socket Connectors, Cable Connectors, Power Connectors, Signal and Data Connectors, Others in the Global Railway Connectors Market:

Plug and socket connectors, cable connectors, power connectors, signal and data connectors, and other types of connectors play a vital role in the Global Railway Connectors Market. Plug and socket connectors are commonly used for connecting various electrical components within the train, providing a secure and reliable connection that can withstand the vibrations and mechanical stresses encountered during operation. These connectors are designed to be easily connected and disconnected, facilitating maintenance and repair activities. Cable connectors, on the other hand, are used to connect different sections of electrical cables, ensuring a continuous and reliable electrical connection throughout the train. These connectors are designed to withstand harsh environmental conditions, including extreme temperatures and exposure to moisture and dust. Power connectors are specifically designed to handle high voltage and current levels, providing a reliable connection for power distribution systems within the train. These connectors are crucial for ensuring the safe and efficient operation of the train's electrical systems, including traction systems, lighting, and other electrical components. Signal and data connectors are used to transmit control signals and data between various components of the train and the railway infrastructure. These connectors are designed to provide a high level of signal integrity and reliability, ensuring the accurate and timely transmission of control signals and data. Other types of connectors used in the railway industry include coaxial connectors, fiber optic connectors, and RF connectors, each designed to meet specific requirements and applications within the railway system. The choice of connectors depends on various factors, including the type of application, environmental conditions, and the specific requirements of the railway system. The development of advanced connectors with improved performance and reliability is a key focus area for manufacturers in the Global Railway Connectors Market, driven by the increasing demand for advanced and reliable railway systems.

Traction Systems, Signaling and Control Systems, Lighting and Electrical Systems, Data Communication, Others in the Global Railway Connectors Market:

The usage of connectors in the Global Railway Connectors Market spans several critical areas, including traction systems, signaling and control systems, lighting and electrical systems, data communication, and other applications. In traction systems, connectors are used to ensure reliable electrical connections between the various components of the traction system, including the traction motors, power converters, and control units. These connectors are designed to handle high voltage and current levels, ensuring the efficient and safe operation of the traction system. In signaling and control systems, connectors are used to transmit control signals and data between the various components of the signaling and control system, including the train control units, signaling equipment, and communication systems. These connectors are designed to provide a high level of signal integrity and reliability, ensuring the accurate and timely transmission of control signals and data. In lighting and electrical systems, connectors are used to connect various electrical components, including lighting fixtures, power distribution units, and control units. These connectors are designed to withstand harsh environmental conditions, including extreme temperatures, vibrations, and mechanical stresses, ensuring the reliable operation of the lighting and electrical systems. In data communication, connectors are used to transmit data between the various components of the train and the railway infrastructure, including communication systems, control units, and data processing units. These connectors are designed to provide a high level of data integrity and reliability, ensuring the accurate and timely transmission of data. Other applications of connectors in the railway industry include the connection of various sensors, actuators, and other electronic components, ensuring the reliable operation of the train and the railway infrastructure. The choice of connectors depends on various factors, including the type of application, environmental conditions, and the specific requirements of the railway system. The development of advanced connectors with improved performance and reliability is a key focus area for manufacturers in the Global Railway Connectors Market, driven by the increasing demand for advanced and reliable railway systems.

Global Railway Connectors Market Outlook:

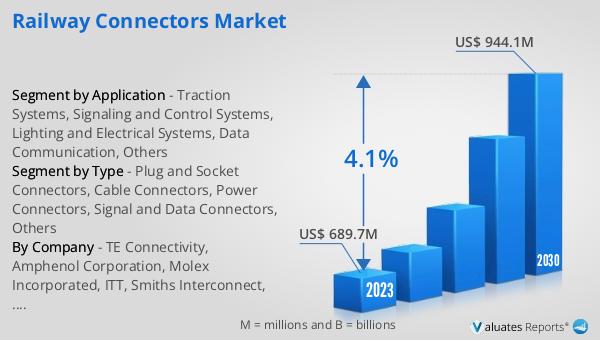

The global Railway Connectors market was valued at US$ 689.7 million in 2023 and is anticipated to reach US$ 944.1 million by 2030, witnessing a CAGR of 4.1% during the forecast period 2024-2030. This growth is driven by the increasing demand for advanced and reliable railway systems, the need for efficient and safe transportation, and the growing investments in railway infrastructure across the globe. The market is characterized by the presence of several key players who offer a variety of connectors designed to meet the specific requirements of the railway industry. These connectors are designed to withstand harsh environmental conditions, including extreme temperatures, vibrations, and mechanical stresses, ensuring the safety and reliability of railway operations. The market is also influenced by technological advancements, such as the development of high-speed trains and the integration of advanced communication and control systems, which require more sophisticated and reliable connectors. The development of advanced connectors with improved performance and reliability is a key focus area for manufacturers in the Global Railway Connectors Market, driven by the increasing demand for advanced and reliable railway systems.

| Report Metric | Details |

| Report Name | Railway Connectors Market |

| Accounted market size in 2023 | US$ 689.7 million |

| Forecasted market size in 2030 | US$ 944.1 million |

| CAGR | 4.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TE Connectivity, Amphenol Corporation, Molex Incorporated, ITT, Smiths Interconnect, Fischer Connectors, Esterline Technologies, Schaltbau, Sichuan Yonggui Science And Technology, TT Electronics, Nexans, Staubli Electrical Connectors, Harting Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |