What is Global Professional Grade Panoramic Photography Equipment Market?

The Global Professional Grade Panoramic Photography Equipment Market refers to the worldwide industry focused on the production and distribution of high-quality equipment designed for capturing panoramic images. This market encompasses a range of products, including cameras, lenses, tripods, and other accessories that enable photographers to capture wide-angle images with exceptional clarity and detail. The demand for such equipment is driven by both professional photographers and hobbyists who seek to create immersive visual experiences. As technology advances, the market continues to evolve, offering more sophisticated and user-friendly products that cater to the diverse needs of its consumers. The growth of this market is fueled by the increasing popularity of panoramic photography in various fields such as real estate, tourism, and virtual reality, where capturing expansive views is essential. Additionally, the rise of social media platforms and the growing trend of sharing visually appealing content have further propelled the demand for professional-grade panoramic photography equipment. As a result, manufacturers are continually innovating to provide cutting-edge solutions that enhance the quality and ease of panoramic photography, making it accessible to a broader audience.

Panoramic Camera, Accessories in the Global Professional Grade Panoramic Photography Equipment Market:

Panoramic cameras and their accessories are integral components of the Global Professional Grade Panoramic Photography Equipment Market. These cameras are specifically designed to capture wide-angle images that encompass a larger field of view than traditional cameras. They achieve this by using specialized lenses and sensors that can capture a 360-degree view or a wide panoramic shot. The technology behind these cameras has advanced significantly, allowing for higher resolution images and more precise stitching of multiple shots to create seamless panoramic photos. Accessories play a crucial role in enhancing the functionality and versatility of panoramic cameras. Tripods, for instance, are essential for stabilizing the camera during shooting, ensuring that images are sharp and free from motion blur. Some tripods are equipped with panoramic heads that allow for smooth rotation, making it easier to capture a full 360-degree view. Additionally, remote controls and smartphone apps have become popular accessories, enabling photographers to control their cameras wirelessly and preview shots in real-time. This is particularly useful for capturing panoramic images in challenging environments or from difficult angles. Another important accessory is the panoramic lens, which is designed to capture a wider field of view than standard lenses. These lenses are often used in conjunction with panoramic cameras to achieve the desired effect. They come in various focal lengths and apertures, allowing photographers to choose the best lens for their specific needs. Filters are also commonly used with panoramic lenses to enhance image quality by reducing glare and improving color saturation. In recent years, the development of virtual reality (VR) technology has further expanded the applications of panoramic photography equipment. VR headsets and software allow users to experience panoramic images in an immersive 3D environment, making them feel as though they are actually present in the scene. This has opened up new possibilities for panoramic photography in fields such as real estate, tourism, and entertainment. As the demand for high-quality panoramic images continues to grow, manufacturers are investing in research and development to create more advanced and user-friendly equipment. This includes the integration of artificial intelligence (AI) and machine learning technologies, which can automate the process of capturing and stitching panoramic images, making it easier for photographers to achieve professional results. Furthermore, the rise of social media platforms and the increasing popularity of sharing visually stunning content have contributed to the growth of the panoramic photography equipment market. Photographers and content creators are constantly seeking new ways to engage their audiences, and panoramic images offer a unique and captivating perspective that stands out in a crowded digital landscape. As a result, the market for panoramic cameras and accessories is expected to continue expanding, driven by the demand for innovative and high-quality products that cater to the evolving needs of photographers and consumers alike.

Personal Use, Commercial Use in the Global Professional Grade Panoramic Photography Equipment Market:

The usage of Global Professional Grade Panoramic Photography Equipment Market spans across various areas, including personal and commercial use. For personal use, panoramic photography equipment allows individuals to capture stunning wide-angle images that showcase their surroundings in a unique and immersive way. This is particularly appealing to photography enthusiasts and hobbyists who enjoy exploring new techniques and pushing the boundaries of traditional photography. With the rise of social media platforms, individuals are increasingly sharing their panoramic images online, seeking to engage their followers with visually captivating content. This has led to a growing interest in panoramic photography among amateur photographers, who are eager to experiment with new equipment and techniques to enhance their skills. On the commercial side, panoramic photography equipment is widely used in industries such as real estate, tourism, and advertising. In real estate, panoramic images provide potential buyers with a comprehensive view of a property, allowing them to explore the space virtually before making a decision. This is particularly useful for showcasing large properties or those with unique architectural features that may not be fully appreciated through traditional photographs. In the tourism industry, panoramic photography is used to capture the beauty and grandeur of destinations, enticing travelers to visit and experience the location for themselves. Tour operators and travel agencies often use panoramic images in their marketing materials to highlight the attractions and experiences available at a destination. Additionally, panoramic photography is employed in the advertising industry to create eye-catching visuals that grab the attention of consumers. Brands and businesses use panoramic images in their campaigns to showcase their products or services in a dynamic and engaging way. This is particularly effective for industries such as automotive, where panoramic images can highlight the design and features of a vehicle from multiple angles. Furthermore, the integration of virtual reality (VR) technology has expanded the commercial applications of panoramic photography equipment. VR experiences allow users to explore panoramic images in an immersive 3D environment, making them feel as though they are actually present in the scene. This has opened up new possibilities for industries such as real estate and tourism, where virtual tours and experiences can provide potential customers with a more interactive and engaging way to explore properties or destinations. As the demand for high-quality panoramic images continues to grow, the Global Professional Grade Panoramic Photography Equipment Market is expected to see continued expansion in both personal and commercial sectors. Manufacturers are investing in research and development to create more advanced and user-friendly equipment that caters to the diverse needs of photographers and consumers alike. This includes the integration of artificial intelligence (AI) and machine learning technologies, which can automate the process of capturing and stitching panoramic images, making it easier for photographers to achieve professional results. Overall, the usage of panoramic photography equipment in personal and commercial applications highlights the versatility and appeal of this technology, as it continues to capture the imagination of photographers and consumers around the world.

Global Professional Grade Panoramic Photography Equipment Market Outlook:

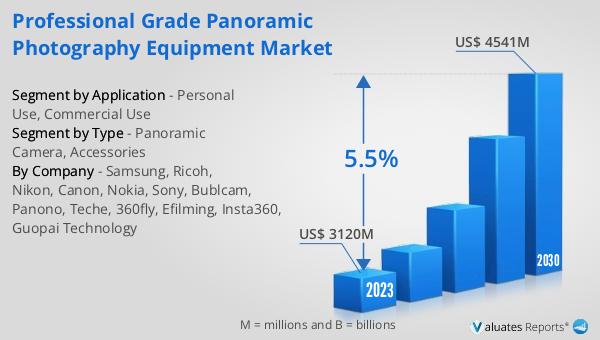

The outlook for the Global Professional Grade Panoramic Photography Equipment Market indicates a promising growth trajectory. The market is anticipated to expand from a valuation of US$ 3,292 million in 2024 to US$ 4,766 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.5% between 2025 and 2031. The expansion of this market is largely attributed to the increasing demand for high-quality panoramic photography equipment across various sectors. Key product segments within this market, such as panoramic cameras, lenses, and accessories, are driving this growth by offering innovative solutions that cater to the evolving needs of photographers and consumers. Additionally, the diverse end-use applications of panoramic photography equipment, ranging from personal use to commercial industries like real estate, tourism, and advertising, are contributing to the market's expansion. As technology continues to advance, manufacturers are focusing on developing more sophisticated and user-friendly products that enhance the quality and ease of panoramic photography. This includes the integration of artificial intelligence (AI) and machine learning technologies, which are expected to further streamline the process of capturing and stitching panoramic images. The growing popularity of social media platforms and the trend of sharing visually appealing content have also played a significant role in driving the demand for professional-grade panoramic photography equipment. As more individuals and businesses seek to create immersive visual experiences, the market is poised for continued growth and innovation. Overall, the outlook for the Global Professional Grade Panoramic Photography Equipment Market is positive, with significant opportunities for expansion and development in the coming years.

| Report Metric | Details |

| Report Name | Professional Grade Panoramic Photography Equipment Market |

| Accounted market size in 2024 | US$ 3292 in million |

| Forecasted market size in 2031 | US$ 4766 million |

| CAGR | 5.5% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Sales by Region |

|

| By Company | Samsung, Ricoh, Nikon, Canon, Nokia, Sony, Bublcam, Panono, Teche, 360fly, Efilming, Insta360, Guopai Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |