What is Silicon Carbide Fibers- Global Market?

Silicon carbide fibers are a key component in the global market, known for their exceptional properties and wide-ranging applications. These fibers are made from silicon carbide, a compound of silicon and carbon, and are renowned for their high strength, lightweight nature, and resistance to heat and corrosion. The global market for silicon carbide fibers is driven by their increasing use in industries such as aerospace, military, nuclear, and others. These fibers are particularly valued for their ability to withstand extreme temperatures and harsh environments, making them ideal for use in high-performance applications. As industries continue to seek materials that offer superior performance and durability, the demand for silicon carbide fibers is expected to grow. This growth is further supported by advancements in manufacturing technologies that enhance the quality and reduce the cost of these fibers, making them more accessible to a broader range of industries. The global market for silicon carbide fibers is poised for significant expansion as more sectors recognize the benefits of incorporating these advanced materials into their products and processes.

Continuous Fiber, Whisker in the Silicon Carbide Fibers- Global Market:

Continuous fiber and whisker-based silicon carbide fibers are two distinct forms of silicon carbide fibers that play a crucial role in the global market. Continuous fibers are long, thin strands of silicon carbide that are used to reinforce composite materials. These fibers are known for their high tensile strength and are often used in applications where durability and resistance to extreme conditions are paramount. Continuous silicon carbide fibers are commonly used in the aerospace industry, where they are incorporated into composite materials to enhance the performance of aircraft components. The high strength-to-weight ratio of these fibers makes them ideal for use in structural applications, where reducing weight without compromising strength is critical. In addition to aerospace, continuous silicon carbide fibers are also used in the automotive industry, where they help improve fuel efficiency and reduce emissions by enabling the production of lighter, more efficient vehicles. Whisker-based silicon carbide fibers, on the other hand, are short, rod-like structures that are used to reinforce ceramics and other materials. These whiskers are known for their ability to improve the toughness and thermal stability of materials, making them ideal for use in high-temperature applications. Whisker-based silicon carbide fibers are often used in the production of cutting tools, where they enhance the wear resistance and longevity of the tools. They are also used in the electronics industry, where they help improve the performance and reliability of electronic components. The global market for silicon carbide fibers is driven by the increasing demand for high-performance materials in various industries. As manufacturers continue to seek materials that offer superior performance and durability, the demand for both continuous and whisker-based silicon carbide fibers is expected to grow. This growth is further supported by advancements in manufacturing technologies that enhance the quality and reduce the cost of these fibers, making them more accessible to a broader range of industries. The global market for silicon carbide fibers is poised for significant expansion as more sectors recognize the benefits of incorporating these advanced materials into their products and processes.

Aerospace, Military Weapons and Equipment, Nuclear, Others in the Silicon Carbide Fibers- Global Market:

Silicon carbide fibers are increasingly being used in a variety of industries due to their exceptional properties, including high strength, lightweight nature, and resistance to heat and corrosion. In the aerospace industry, these fibers are used to reinforce composite materials, enhancing the performance of aircraft components. The high strength-to-weight ratio of silicon carbide fibers makes them ideal for use in structural applications, where reducing weight without compromising strength is critical. This is particularly important in the aerospace industry, where lighter aircraft can lead to improved fuel efficiency and reduced emissions. In the military sector, silicon carbide fibers are used in the production of weapons and equipment. Their high strength and resistance to extreme conditions make them ideal for use in applications where durability and reliability are paramount. Silicon carbide fibers are used to reinforce armor and other protective equipment, providing enhanced protection for military personnel. In the nuclear industry, silicon carbide fibers are used in the production of fuel cladding and other components. Their resistance to heat and corrosion makes them ideal for use in the harsh environments found in nuclear reactors. Silicon carbide fibers help improve the safety and efficiency of nuclear power plants by providing enhanced protection against radiation and other hazards. In addition to these industries, silicon carbide fibers are also used in a variety of other applications, including the production of cutting tools, electronics, and automotive components. The global market for silicon carbide fibers is driven by the increasing demand for high-performance materials in these and other industries. As manufacturers continue to seek materials that offer superior performance and durability, the demand for silicon carbide fibers is expected to grow. This growth is further supported by advancements in manufacturing technologies that enhance the quality and reduce the cost of these fibers, making them more accessible to a broader range of industries. The global market for silicon carbide fibers is poised for significant expansion as more sectors recognize the benefits of incorporating these advanced materials into their products and processes.

Silicon Carbide Fibers- Global Market Outlook:

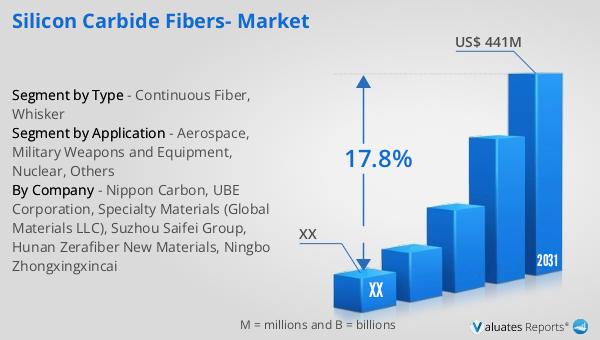

The global market for silicon carbide fibers is experiencing significant growth, with its value projected to increase substantially over the coming years. In 2024, the market was valued at approximately $142 million. However, by 2031, it is expected to reach an adjusted size of $441 million, reflecting a compound annual growth rate (CAGR) of 17.8% during the forecast period from 2025 to 2031. This impressive growth rate underscores the increasing demand for silicon carbide fibers across various industries. The market's expansion is driven by the growing need for high-performance materials that offer superior strength, lightweight properties, and resistance to extreme conditions. As industries such as aerospace, military, nuclear, and automotive continue to seek materials that enhance the performance and durability of their products, the demand for silicon carbide fibers is expected to rise. Additionally, advancements in manufacturing technologies are making these fibers more accessible and cost-effective, further fueling market growth. The global market for silicon carbide fibers is poised for significant expansion as more sectors recognize the benefits of incorporating these advanced materials into their products and processes. This growth presents opportunities for manufacturers and suppliers to capitalize on the increasing demand for silicon carbide fibers and expand their market presence.

| Report Metric | Details |

| Report Name | Silicon Carbide Fibers- Market |

| Forecasted market size in 2031 | US$ 441 million |

| CAGR | 17.8% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Nippon Carbon, UBE Corporation, Specialty Materials (Global Materials LLC), Suzhou Saifei Group, Hunan Zerafiber New Materials, Ningbo Zhongxingxincai |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |