What is Polyurethane Elastomers- Global Market?

Polyurethane elastomers are a versatile and widely used material in the global market, known for their exceptional elasticity, durability, and resistance to abrasion and chemicals. These elastomers are a type of polymer that combines the properties of rubber and plastic, making them ideal for a variety of applications. They are formed through the reaction of a polyol with a diisocyanate, resulting in a material that can be tailored to meet specific performance requirements. The global market for polyurethane elastomers is driven by their extensive use in industries such as automotive, construction, electronics, and footwear. Their ability to be molded into complex shapes and their excellent mechanical properties make them a preferred choice for manufacturers looking to enhance product performance and longevity. As industries continue to seek materials that offer both flexibility and strength, the demand for polyurethane elastomers is expected to grow, supported by ongoing innovations and advancements in production technologies. The adaptability of these elastomers to various environmental conditions further cements their position as a critical component in modern manufacturing processes.

Casting Polyurethane Elastomer (CPE), Thermoplastic Polyurethane Elastomer (TPE), Polyurethane Microcellular Elastomer, Mixed Polyurethane Elastomer(MPE) and Others in the Polyurethane Elastomers- Global Market:

Casting Polyurethane Elastomer (CPE) is a type of polyurethane elastomer that is known for its excellent load-bearing capacity and resistance to wear and tear. It is commonly used in applications where durability and resilience are paramount, such as in the production of wheels, rollers, and industrial parts. CPEs are valued for their ability to maintain performance under high-stress conditions, making them ideal for heavy-duty applications. Thermoplastic Polyurethane Elastomer (TPE), on the other hand, offers a unique combination of elasticity and processability. TPEs can be easily molded and reshaped, which makes them suitable for applications requiring flexibility and ease of manufacturing, such as in the production of hoses, seals, and gaskets. Their ability to be recycled and reused also adds to their appeal in environmentally conscious markets. Polyurethane Microcellular Elastomer is characterized by its lightweight and cushioning properties, making it an excellent choice for applications that require shock absorption and comfort, such as in footwear and automotive seating. These elastomers are designed to provide a balance between softness and support, enhancing user comfort and product performance. Mixed Polyurethane Elastomer (MPE) combines the properties of different types of polyurethane elastomers to create a material that offers a broader range of performance characteristics. MPEs are often used in applications that require a combination of strength, flexibility, and resistance to environmental factors. This versatility makes them suitable for a wide range of industries, from automotive to consumer goods. Other types of polyurethane elastomers include those specifically formulated for niche applications, such as those requiring high-temperature resistance or enhanced chemical stability. These specialized elastomers are developed to meet the unique demands of specific industries, ensuring that manufacturers have access to materials that can withstand the rigors of their particular applications. As the global market for polyurethane elastomers continues to expand, the development of new formulations and the refinement of existing ones will play a crucial role in meeting the evolving needs of various industries.

Automotive, Industrial Machinery, Electronics and Electrical Appliances, Medical Equipment, Sports and Leisure, Other in the Polyurethane Elastomers- Global Market:

Polyurethane elastomers find extensive usage across a variety of sectors due to their unique properties. In the automotive industry, they are used in the manufacturing of components such as bushings, gaskets, and seals, where their durability and resistance to wear are crucial. These elastomers help in reducing noise, vibration, and harshness, enhancing the overall driving experience. In industrial machinery, polyurethane elastomers are employed in the production of wheels, rollers, and conveyor belts, where their ability to withstand heavy loads and resist abrasion is highly valued. Their use in these applications helps in extending the lifespan of machinery and reducing maintenance costs. In the electronics and electrical appliances sector, polyurethane elastomers are used for insulating and protecting components from moisture and dust, ensuring the longevity and reliability of electronic devices. Their flexibility and ease of molding make them ideal for use in complex electronic assemblies. In the medical equipment industry, polyurethane elastomers are used in the production of medical tubing, catheters, and other devices that require biocompatibility and flexibility. Their non-reactive nature and ability to be sterilized make them suitable for use in sensitive medical applications. In the sports and leisure industry, polyurethane elastomers are used in the production of equipment such as skate wheels, protective gear, and footwear, where their cushioning properties and durability enhance performance and comfort. Other applications of polyurethane elastomers include their use in the construction industry for sealants and adhesives, where their resistance to environmental factors and ability to bond with various substrates are advantageous. As industries continue to seek materials that offer a balance of performance, durability, and cost-effectiveness, the demand for polyurethane elastomers is expected to grow, driven by their versatility and adaptability to a wide range of applications.

Polyurethane Elastomers- Global Market Outlook:

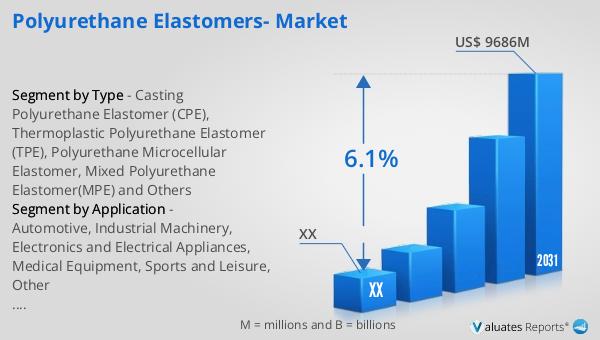

The global market for polyurethane elastomers is poised for significant growth in the coming years. In 2024, the market was valued at approximately US$ 6,453 million. By 2031, it is projected to reach an adjusted size of US$ 9,686 million, reflecting a compound annual growth rate (CAGR) of 6.1% during the forecast period from 2025 to 2031. This growth is driven by the increasing demand for durable and versatile materials across various industries, including automotive, construction, and electronics. The adaptability of polyurethane elastomers to different applications and their ability to enhance product performance make them a preferred choice for manufacturers looking to improve the quality and longevity of their products. As technological advancements continue to drive innovation in the production and application of polyurethane elastomers, the market is expected to witness sustained growth. The ongoing development of new formulations and the refinement of existing ones will play a crucial role in meeting the evolving needs of industries seeking materials that offer a balance of performance, durability, and cost-effectiveness. With their unique properties and wide range of applications, polyurethane elastomers are set to remain a key component in modern manufacturing processes, supporting the growth and development of various sectors worldwide.

| Report Metric | Details |

| Report Name | Polyurethane Elastomers- Market |

| Forecasted market size in 2031 | US$ 9686 million |

| CAGR | 6.1% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Huafeng Group, BASF, Lubrizol, Wanhua Chemical, Covestro, Yinoway, Merui New Materials, Huntsman, LANXESS, Zibo Huatian Rubber & Plastic Technology, Huide Technology, COIM Group, Epaflex, Trinseo, Hexpol, Avient, Zhongke Yourui |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |