What is Global LED Lighting Driver ICs Market?

The Global LED Lighting Driver ICs Market is a crucial segment within the broader semiconductor industry, focusing on integrated circuits (ICs) that regulate the power to LED lighting systems. These driver ICs are essential for ensuring that LEDs operate efficiently and have a long lifespan. They manage the electrical current and voltage supplied to the LEDs, preventing issues such as flickering and overheating. The market for these components is driven by the increasing adoption of LED lighting across various sectors due to its energy efficiency, durability, and environmental benefits. As more industries and consumers shift towards sustainable lighting solutions, the demand for LED driver ICs continues to grow. This market encompasses a wide range of applications, from residential and commercial lighting to automotive and industrial uses. The technological advancements in LED driver ICs, such as improved dimming capabilities and smart lighting integration, further propel the market's expansion. With the global push towards energy conservation and the reduction of carbon footprints, the Global LED Lighting Driver ICs Market is poised for significant growth in the coming years, playing a pivotal role in the transition to greener lighting technologies.

SMD Type, Through Hole Type in the Global LED Lighting Driver ICs Market:

In the Global LED Lighting Driver ICs Market, two primary types of driver ICs are prevalent: Surface-Mount Device (SMD) Type and Through Hole Type. SMD Type driver ICs are designed to be mounted directly onto the surface of printed circuit boards (PCBs). This type of mounting allows for more compact and lightweight designs, which is particularly advantageous in applications where space is limited. SMD Type driver ICs are widely used in consumer electronics, automotive lighting, and general lighting applications due to their efficiency and ease of integration into complex circuits. They offer high reliability and are capable of supporting high-density circuit designs, making them ideal for modern LED lighting solutions that require compactness and efficiency. On the other hand, Through Hole Type driver ICs are mounted by inserting their leads through holes in the PCB and soldering them on the opposite side. This traditional method provides strong mechanical bonds and is often used in applications where durability and robustness are critical. Through Hole Type driver ICs are typically found in industrial and high-power applications where the physical strength of the connection is a priority. While they may not offer the same level of compactness as SMD Type ICs, they are valued for their reliability and ease of manual assembly, which can be beneficial in certain manufacturing processes. Both SMD and Through Hole Type driver ICs play vital roles in the Global LED Lighting Driver ICs Market, catering to different needs and preferences in various applications. As technology continues to evolve, manufacturers are constantly innovating to enhance the performance and capabilities of these driver ICs, ensuring they meet the growing demands of the LED lighting industry.

Automotive Lighting, General Lighting in the Global LED Lighting Driver ICs Market:

The Global LED Lighting Driver ICs Market finds significant usage in various areas, including automotive lighting and general lighting. In the automotive sector, LED lighting driver ICs are crucial for the development of advanced lighting systems that enhance vehicle safety and aesthetics. These ICs enable precise control over LED headlights, taillights, and interior lighting, allowing for features such as adaptive lighting, which adjusts the beam pattern based on driving conditions. The energy efficiency of LEDs, combined with the sophisticated control offered by driver ICs, contributes to reduced power consumption and extended battery life in electric vehicles. Moreover, the compact size of LED driver ICs allows for innovative lighting designs that can improve the overall look and feel of a vehicle. In general lighting, LED driver ICs are used in a wide range of applications, from residential and commercial lighting to streetlights and architectural lighting. They provide the necessary power regulation to ensure LEDs operate efficiently and with minimal flicker, which is essential for creating comfortable and visually appealing lighting environments. The ability to integrate smart lighting features, such as dimming and color tuning, is made possible by advanced driver ICs, enabling users to customize their lighting experience. As the demand for energy-efficient and sustainable lighting solutions continues to rise, the role of LED driver ICs in both automotive and general lighting becomes increasingly important. These components not only enhance the performance and longevity of LED systems but also contribute to the broader goals of energy conservation and environmental sustainability.

Global LED Lighting Driver ICs Market Outlook:

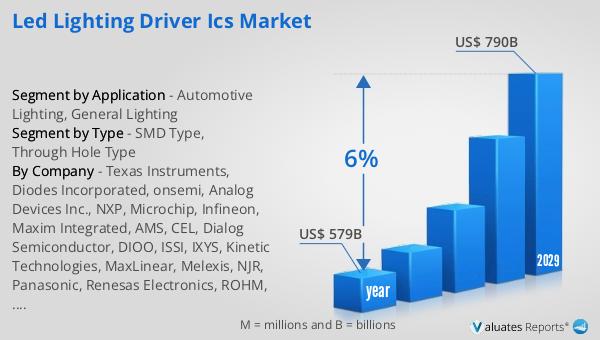

The global semiconductor market, which includes the LED Lighting Driver ICs Market, was valued at approximately $579 billion in 2022. This market is anticipated to grow significantly, reaching around $790 billion by 2029. This growth represents a compound annual growth rate (CAGR) of 6% over the forecast period. The expansion of the semiconductor market is driven by the increasing demand for electronic devices, advancements in technology, and the growing adoption of smart and energy-efficient solutions across various industries. As the world becomes more connected and reliant on digital technologies, the need for semiconductors, including LED driver ICs, continues to rise. These components are integral to the functioning of modern electronic devices, enabling innovations in areas such as artificial intelligence, the Internet of Things (IoT), and renewable energy. The projected growth of the semiconductor market underscores the importance of continued investment in research and development to drive technological advancements and meet the evolving needs of consumers and industries. As the market expands, companies within the semiconductor industry are poised to capitalize on new opportunities, contributing to economic growth and technological progress on a global scale.

| Report Metric | Details |

| Report Name | LED Lighting Driver ICs Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Texas Instruments, Diodes Incorporated, onsemi, Analog Devices Inc., NXP, Microchip, Infineon, Maxim Integrated, AMS, CEL, Dialog Semiconductor, DIOO, ISSI, IXYS, Kinetic Technologies, MaxLinear, Melexis, NJR, Panasonic, Renesas Electronics, ROHM, STM, Toshiba, Wurth Elektronik |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |