What is Global Programmable Logic Devices Market?

The Global Programmable Logic Devices (PLD) Market is a dynamic and rapidly evolving sector within the broader electronics industry. Programmable Logic Devices are semiconductor devices used to build reconfigurable digital circuits. Unlike fixed-function logic gates, PLDs can be programmed to perform specific functions, making them highly versatile and adaptable to various applications. This flexibility allows engineers to design and implement complex logic functions without the need for custom-designed chips, significantly reducing development time and cost. The market for PLDs is driven by the increasing demand for advanced electronic devices across various industries, including telecommunications, consumer electronics, automotive, and industrial sectors. As technology continues to advance, the need for more sophisticated and efficient electronic components grows, further propelling the demand for PLDs. The global market for these devices is characterized by continuous innovation and development, with manufacturers striving to enhance the performance, capacity, and efficiency of their products to meet the ever-evolving needs of their customers. As a result, the Global Programmable Logic Devices Market is poised for significant growth in the coming years, offering numerous opportunities for businesses and investors alike.

Simple Programmable Logic Devices (SPLDs), Complex Programmable Logic Devices (CPLDs), Field-Programmable Gate Arrays (FPGAs) in the Global Programmable Logic Devices Market:

Simple Programmable Logic Devices (SPLDs), Complex Programmable Logic Devices (CPLDs), and Field-Programmable Gate Arrays (FPGAs) are the three main types of programmable logic devices that play a crucial role in the Global Programmable Logic Devices Market. SPLDs are the most basic form of programmable logic devices, typically consisting of a small number of logic gates and flip-flops. They are used for simple logic functions and are ideal for applications that require minimal logic complexity. SPLDs are cost-effective and easy to use, making them a popular choice for small-scale projects and educational purposes. On the other hand, CPLDs are more advanced than SPLDs and offer greater logic capacity and complexity. They consist of multiple SPLD-like blocks interconnected by a programmable interconnect matrix, allowing for more complex logic functions to be implemented. CPLDs are suitable for medium-scale applications that require moderate logic complexity and are often used in telecommunications, consumer electronics, and automotive industries. FPGAs are the most advanced type of programmable logic devices, offering the highest logic capacity and complexity. They consist of an array of programmable logic blocks and interconnects, allowing for highly complex logic functions to be implemented. FPGAs are ideal for large-scale applications that require high performance and flexibility, such as data centers, military and aerospace, and industrial automation. The versatility and adaptability of FPGAs make them a popular choice for applications that require frequent updates and modifications. In the Global Programmable Logic Devices Market, these three types of devices cater to a wide range of applications and industries, each offering unique advantages and capabilities. As technology continues to advance, the demand for more sophisticated and efficient programmable logic devices is expected to grow, driving further innovation and development in this market.

Telecom, Consumer Electronics, Automotive, Industrial, Military and Aerospace, Data Center, Others in the Global Programmable Logic Devices Market:

The Global Programmable Logic Devices Market finds extensive usage across various industries, each benefiting from the unique capabilities and advantages offered by these devices. In the telecommunications sector, programmable logic devices are used to develop and implement complex communication protocols and signal processing algorithms. They enable the rapid deployment of new communication standards and technologies, ensuring that telecom networks remain efficient and up-to-date. In consumer electronics, programmable logic devices are used to design and implement advanced features in devices such as smartphones, tablets, and smart TVs. They enable manufacturers to quickly adapt to changing consumer preferences and technological advancements, ensuring that their products remain competitive in the market. In the automotive industry, programmable logic devices are used to develop and implement advanced driver assistance systems (ADAS), infotainment systems, and other electronic control units (ECUs). They enable automakers to enhance the safety, performance, and user experience of their vehicles, meeting the growing demand for smarter and more connected cars. In the industrial sector, programmable logic devices are used to develop and implement automation and control systems for manufacturing processes. They enable manufacturers to improve efficiency, reduce downtime, and enhance product quality, driving productivity and competitiveness. In the military and aerospace sector, programmable logic devices are used to develop and implement advanced avionics, radar, and communication systems. They enable defense contractors to meet the stringent performance and reliability requirements of military and aerospace applications, ensuring mission success and safety. In data centers, programmable logic devices are used to develop and implement high-performance computing and networking solutions. They enable data center operators to optimize resource utilization, reduce energy consumption, and enhance service delivery, meeting the growing demand for cloud computing and data-driven applications. In other industries, programmable logic devices are used to develop and implement a wide range of applications, from medical devices to renewable energy systems. The versatility and adaptability of programmable logic devices make them an essential component in the development of innovative and efficient solutions across various sectors.

Global Programmable Logic Devices Market Outlook:

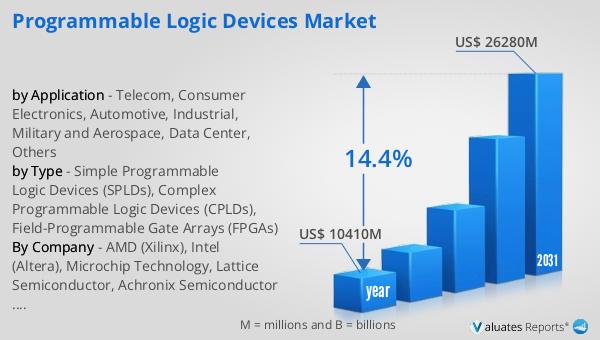

In 2024, the global market for Programmable Logic Devices was valued at approximately $10.41 billion. This market is anticipated to experience significant growth over the coming years, with projections indicating that it will reach an estimated size of $26.28 billion by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 14.4% during the forecast period. The robust expansion of this market can be attributed to several factors, including the increasing demand for advanced electronic devices across various industries, such as telecommunications, consumer electronics, automotive, and industrial sectors. As technology continues to evolve, the need for more sophisticated and efficient electronic components grows, further driving the demand for programmable logic devices. Additionally, the continuous innovation and development within the programmable logic devices market, with manufacturers striving to enhance the performance, capacity, and efficiency of their products, contribute to the market's growth. This dynamic and rapidly evolving sector offers numerous opportunities for businesses and investors alike, as the demand for programmable logic devices continues to rise in response to the ever-changing technological landscape. The projected growth of the global programmable logic devices market underscores the importance of these devices in the development of innovative and efficient solutions across various industries.

| Report Metric | Details |

| Report Name | Programmable Logic Devices Market |

| Accounted market size in year | US$ 10410 million |

| Forecasted market size in 2031 | US$ 26280 million |

| CAGR | 14.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | AMD (Xilinx), Intel (Altera), Microchip Technology, Lattice Semiconductor, Achronix Semiconductor Corporation, Shanghai Anlogic Infotech, Fudan Microelectronics, Ziguang Tongchuang, Gowin Semiconductor, Hercules Microelectronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |