What is Global Digital Door Lock System Market?

The Global Digital Door Lock System Market is a rapidly evolving sector that focuses on providing advanced security solutions for various types of doors. These systems are designed to replace traditional mechanical locks with digital alternatives that offer enhanced security features and convenience. The market encompasses a wide range of products, including keypad locks, biometric locks, and smart locks that can be controlled remotely via smartphones or other devices. The increasing demand for smart homes and the growing awareness of security issues are driving the expansion of this market. Additionally, technological advancements and the integration of Internet of Things (IoT) technologies are further propelling the growth of digital door lock systems. These systems are not only used in residential settings but also in commercial, governmental, and other sectors, providing a versatile solution for modern security needs. As the world becomes more connected and security concerns rise, the Global Digital Door Lock System Market is poised to play a crucial role in shaping the future of access control and security solutions.

Keypad Locks, Biometrics Locks in the Global Digital Door Lock System Market:

Keypad locks and biometric locks are two prominent types of digital door lock systems that have gained significant traction in the Global Digital Door Lock System Market. Keypad locks are electronic locks that require a numerical code to unlock the door. They offer a convenient and secure way to manage access without the need for physical keys. Users can easily change the access code, making it simple to manage who can enter a property. Keypad locks are particularly popular in settings where multiple people need access, such as office buildings or shared residential spaces. They are also favored for their durability and ease of installation. On the other hand, biometric locks use unique biological traits, such as fingerprints or facial recognition, to grant access. These locks offer a higher level of security as they rely on individual characteristics that are difficult to replicate or steal. Biometric locks are increasingly being used in high-security areas, such as government buildings or research facilities, where unauthorized access could have serious consequences. The integration of biometric technology into digital door locks represents a significant advancement in security solutions, providing a seamless and secure way to manage access. Both keypad and biometric locks are part of a broader trend towards smart security solutions that leverage technology to enhance safety and convenience. As the Global Digital Door Lock System Market continues to grow, these types of locks are expected to become even more prevalent, offering innovative solutions to meet the evolving security needs of consumers and businesses alike.

Residential, Commercial, Government, Other in the Global Digital Door Lock System Market:

The usage of Global Digital Door Lock System Market products varies across different sectors, each with its unique requirements and challenges. In residential areas, digital door locks offer homeowners a convenient and secure way to manage access to their homes. With features like remote access and real-time notifications, homeowners can monitor who enters and exits their property, enhancing their sense of security. In commercial settings, digital door locks provide businesses with a reliable way to control access to their premises. They can be integrated with existing security systems to offer a comprehensive solution that protects valuable assets and sensitive information. For government buildings, where security is of utmost importance, digital door locks offer a robust solution that can be tailored to meet specific security protocols. These locks can be programmed to allow access only to authorized personnel, reducing the risk of unauthorized entry. In other sectors, such as healthcare or education, digital door locks offer a flexible solution that can be adapted to meet the unique needs of each environment. For example, in hospitals, digital door locks can be used to secure areas with sensitive medical equipment or patient records, while in schools, they can help manage access to classrooms and administrative offices. Overall, the Global Digital Door Lock System Market provides a versatile range of products that can be customized to meet the diverse security needs of different sectors, offering a modern solution to traditional security challenges.

Global Digital Door Lock System Market Outlook:

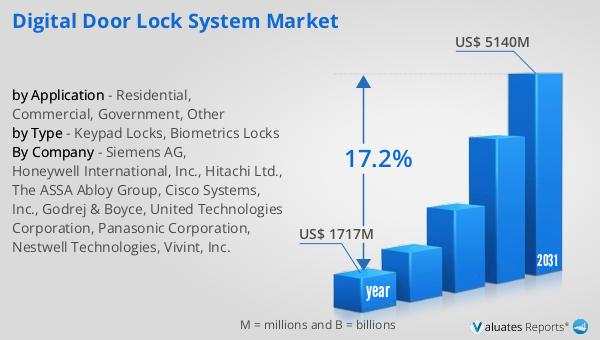

The outlook for the Global Digital Door Lock System Market is promising, with significant growth expected in the coming years. In 2024, the market was valued at approximately US$ 1717 million, and it is anticipated to expand to a revised size of US$ 5140 million by 2031. This growth represents a compound annual growth rate (CAGR) of 17.2% during the forecast period. This impressive growth can be attributed to several factors, including the increasing demand for smart home solutions, advancements in technology, and the growing awareness of security issues. As more consumers and businesses recognize the benefits of digital door lock systems, the market is expected to continue its upward trajectory. The integration of IoT technologies and the development of new, innovative products are also expected to drive growth in the market. As the market expands, it will provide new opportunities for manufacturers and suppliers to develop and offer cutting-edge security solutions that meet the evolving needs of consumers and businesses. The Global Digital Door Lock System Market is poised to play a crucial role in shaping the future of security solutions, offering a modern and effective way to manage access and protect valuable assets.

| Report Metric | Details |

| Report Name | Digital Door Lock System Market |

| Accounted market size in year | US$ 1717 million |

| Forecasted market size in 2031 | US$ 5140 million |

| CAGR | 17.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Siemens AG, Honeywell International, Inc., Hitachi Ltd., The ASSA Abloy Group, Cisco Systems, Inc., Godrej & Boyce, United Technologies Corporation, Panasonic Corporation, Nestwell Technologies, Vivint, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |