What is Global Flame Retardant Chemicals Market?

The global flame retardant chemicals market is a crucial segment of the chemical industry, focusing on substances that are added to materials to prevent or slow the spread of fire. These chemicals are essential in enhancing the safety of various products by reducing their flammability. Flame retardants are used in a wide range of applications, including textiles, electronics, construction materials, and transportation. The market is driven by stringent fire safety regulations and the increasing demand for fire-resistant materials in various industries. As urbanization and industrialization continue to rise, the need for flame retardant chemicals is expected to grow, particularly in developing regions. The market is characterized by a diverse range of products, including organic and inorganic flame retardants, each with specific applications and benefits. The ongoing research and development efforts in this field aim to create more efficient and environmentally friendly flame retardants, addressing concerns about the potential health and environmental impacts of traditional flame retardant chemicals. Overall, the global flame retardant chemicals market plays a vital role in ensuring safety and compliance across multiple sectors, making it an indispensable part of modern industry.

Organic Flame Retardant Chemicals, Inorganic Flame Retardant Chemicals in the Global Flame Retardant Chemicals Market:

Organic flame retardant chemicals are a significant segment within the global flame retardant chemicals market. These compounds are primarily carbon-based and are used to enhance the fire resistance of various materials. Organic flame retardants include brominated, chlorinated, and phosphorus-based compounds. Brominated flame retardants are widely used due to their effectiveness in a variety of applications, including electronics and textiles. They work by releasing bromine atoms that interfere with the combustion process, thus slowing down the spread of fire. However, concerns about their environmental persistence and potential health impacts have led to increased scrutiny and regulation. Chlorinated flame retardants, on the other hand, are used in applications where high thermal stability is required, such as in the automotive and construction industries. These compounds release chlorine atoms that help in forming a protective char layer on the material's surface, thereby preventing further combustion. Phosphorus-based flame retardants are gaining popularity due to their lower environmental impact compared to brominated and chlorinated compounds. They are used in a variety of applications, including textiles, plastics, and coatings. These compounds work by promoting char formation and releasing phosphoric acid, which helps in forming a protective barrier against fire. Inorganic flame retardant chemicals, on the other hand, are primarily mineral-based and include compounds such as aluminum hydroxide, magnesium hydroxide, and antimony trioxide. Aluminum hydroxide is one of the most widely used inorganic flame retardants due to its effectiveness and low cost. It works by releasing water vapor when heated, which cools the material and dilutes flammable gases. Magnesium hydroxide functions similarly but is used in applications requiring higher processing temperatures. Antimony trioxide is often used in combination with halogenated flame retardants to enhance their effectiveness. It acts as a synergist, promoting the formation of a protective char layer. Inorganic flame retardants are generally considered to be more environmentally friendly than their organic counterparts, as they do not release toxic gases during combustion. However, they may require higher loadings to achieve the same level of fire resistance, which can affect the mechanical properties of the material. Overall, both organic and inorganic flame retardant chemicals play a crucial role in enhancing the fire safety of various products. The choice between them depends on factors such as the specific application, regulatory requirements, and environmental considerations. As the demand for safer and more sustainable flame retardants continues to grow, ongoing research and development efforts are focused on creating new compounds that offer improved performance and reduced environmental impact.

Building & Construction, Electronics & Appliances, Wire & Cable, Automotive, Others in the Global Flame Retardant Chemicals Market:

The global flame retardant chemicals market finds extensive usage across various sectors, each with specific requirements and challenges. In the building and construction industry, flame retardants are crucial for ensuring the safety of structures by reducing the flammability of construction materials such as insulation, roofing, and wall coverings. These chemicals help in meeting stringent fire safety regulations and standards, thereby protecting lives and property. In the electronics and appliances sector, flame retardants are used to enhance the fire resistance of components such as circuit boards, connectors, and casings. With the increasing demand for electronic devices, the need for effective flame retardants is also on the rise. These chemicals help in preventing electrical fires and ensuring the safety of consumers. In the wire and cable industry, flame retardants are essential for preventing the spread of fire through electrical wiring systems. They are used in the insulation and jacketing of cables to enhance their fire resistance and ensure compliance with safety standards. In the automotive industry, flame retardants are used in various components such as seats, dashboards, and interior panels to enhance their fire resistance. With the increasing focus on passenger safety, the demand for flame retardants in this sector is expected to grow. Other applications of flame retardant chemicals include textiles, furniture, and packaging materials. In the textile industry, flame retardants are used to enhance the fire resistance of fabrics used in clothing, upholstery, and curtains. In the furniture industry, these chemicals are used in the production of fire-resistant foams and coverings. In the packaging industry, flame retardants are used to enhance the fire resistance of packaging materials, particularly those used for transporting hazardous goods. Overall, the global flame retardant chemicals market plays a vital role in enhancing the safety and compliance of various products across multiple sectors. As the demand for fire-resistant materials continues to grow, the market is expected to witness significant growth in the coming years.

Global Flame Retardant Chemicals Market Outlook:

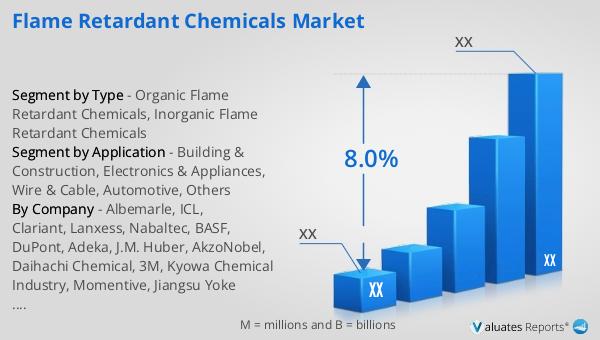

In 2024, the global flame retardant chemicals market was valued at approximately US$ 13,390 million. Projections indicate that by 2031, this market could expand to around US$ 22,770 million, reflecting a compound annual growth rate (CAGR) of 8.0% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold about 20% of the market share. Geographically, China emerges as the largest market, accounting for roughly 45% of the global share, followed by North America, which holds about 15%. When examining product segments, organic flame retardant chemicals lead the market, comprising approximately 65% of the total share. This data underscores the significant role of organic flame retardants in the industry, driven by their widespread application and effectiveness. The market dynamics highlight the importance of innovation and adaptation to regulatory changes, as manufacturers strive to meet the growing demand for safer and more sustainable flame retardant solutions. As the industry evolves, the focus remains on balancing performance with environmental and health considerations, ensuring that flame retardant chemicals continue to play a crucial role in enhancing safety across various applications.

| Report Metric | Details |

| Report Name | Flame Retardant Chemicals Market |

| CAGR | 8.0% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Albemarle, ICL, Clariant, Lanxess, Nabaltec, BASF, DuPont, Adeka, J.M. Huber, AkzoNobel, Daihachi Chemical, 3M, Kyowa Chemical Industry, Momentive, Jiangsu Yoke Technology, Zhejiang Wansheng, Jinan Taixing Fine Chemical, Hangzhou JLS, Shandong Brother |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |