What is Global Combustion Analyzer Market?

The Global Combustion Analyzer Market is a dynamic and essential segment within the broader field of environmental and industrial monitoring. Combustion analyzers are sophisticated devices used to measure the efficiency and emissions of combustion processes. These devices are crucial in ensuring that combustion systems, such as boilers, furnaces, and engines, operate efficiently and within environmental regulations. The market for combustion analyzers is driven by the increasing demand for energy efficiency and the need to reduce harmful emissions. As industries and governments worldwide strive to meet stringent environmental standards, the demand for accurate and reliable combustion analysis tools has grown. The market encompasses a range of products, from portable devices used for field testing to stationary systems integrated into industrial processes. With advancements in technology, modern combustion analyzers offer enhanced features such as wireless connectivity, real-time data analysis, and user-friendly interfaces, making them indispensable tools for engineers and technicians. The global market is characterized by a diverse range of manufacturers and suppliers, each offering unique solutions tailored to specific applications and industries. As environmental concerns continue to rise, the Global Combustion Analyzer Market is poised for sustained growth, driven by innovation and the ongoing pursuit of cleaner, more efficient energy solutions.

Portable Combustion Analyzer, Stationary Combustion Analyzer in the Global Combustion Analyzer Market:

Portable combustion analyzers are compact, handheld devices designed for on-the-go testing and analysis of combustion systems. These analyzers are particularly useful for field technicians and engineers who need to perform quick and accurate assessments of combustion efficiency and emissions in various settings. Portable combustion analyzers are equipped with sensors that measure key parameters such as oxygen levels, carbon monoxide, carbon dioxide, and nitrogen oxides. These measurements help determine the efficiency of the combustion process and identify any potential issues that may need addressing. The portability of these devices makes them ideal for use in diverse environments, from residential heating systems to large industrial boilers. They are often used during routine maintenance checks, troubleshooting, and compliance testing to ensure that systems are operating within regulatory limits. The ease of use and versatility of portable combustion analyzers have made them a popular choice among professionals in the HVAC, energy, and manufacturing sectors. On the other hand, stationary combustion analyzers are designed for continuous monitoring and analysis of combustion processes in industrial settings. These systems are typically integrated into the combustion equipment and provide real-time data on the performance and emissions of the system. Stationary analyzers are essential for large-scale operations where maintaining optimal combustion efficiency is critical for both economic and environmental reasons. They offer advanced features such as automated data logging, remote monitoring, and integration with control systems, allowing for seamless operation and management of combustion processes. The use of stationary combustion analyzers is prevalent in industries such as power generation, petrochemicals, and manufacturing, where precise control of combustion parameters is necessary to meet production goals and environmental standards. Both portable and stationary combustion analyzers play a vital role in the Global Combustion Analyzer Market, catering to the diverse needs of different industries and applications. As technology continues to evolve, these devices are becoming more sophisticated, offering enhanced accuracy, reliability, and ease of use. The ongoing demand for energy efficiency and emission reduction is expected to drive further innovation and growth in this market segment, as industries seek to optimize their combustion processes and minimize their environmental impact.

Commercial, Residential, Industrial in the Global Combustion Analyzer Market:

The Global Combustion Analyzer Market finds extensive application across various sectors, including commercial, residential, and industrial areas. In the commercial sector, combustion analyzers are used to ensure the efficient operation of heating, ventilation, and air conditioning (HVAC) systems. These systems are critical for maintaining comfortable indoor environments in office buildings, shopping centers, and other commercial establishments. By using combustion analyzers, facility managers can optimize the performance of HVAC systems, reduce energy consumption, and ensure compliance with environmental regulations. In the residential sector, combustion analyzers are employed to assess the efficiency and safety of home heating systems, such as furnaces and boilers. Homeowners and technicians use these devices to perform routine maintenance checks, identify potential issues, and ensure that heating systems are operating safely and efficiently. This not only helps in reducing energy bills but also minimizes the risk of carbon monoxide poisoning, which can result from faulty combustion systems. In the industrial sector, combustion analyzers are indispensable tools for monitoring and optimizing combustion processes in large-scale operations. Industries such as power generation, petrochemicals, and manufacturing rely on combustion analyzers to ensure that their systems are running at peak efficiency and within environmental compliance. These analyzers provide real-time data on combustion performance, allowing operators to make informed decisions and adjustments to improve efficiency and reduce emissions. The use of combustion analyzers in industrial settings is crucial for meeting production targets, minimizing operational costs, and adhering to stringent environmental standards. Overall, the Global Combustion Analyzer Market plays a vital role in enhancing energy efficiency and reducing emissions across various sectors. As the demand for cleaner and more efficient energy solutions continues to grow, the importance of combustion analyzers in achieving these goals cannot be overstated. The market is poised for continued growth as industries and consumers alike seek to optimize their energy use and minimize their environmental impact.

Global Combustion Analyzer Market Outlook:

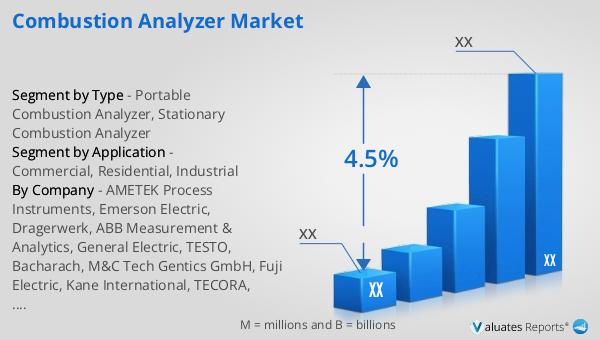

In 2024, the global market size for combustion analyzers was valued at approximately $1,158 million. Looking ahead, it is projected to grow to around $1,569 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2025 to 2031. The market is characterized by a concentration of key players, with the top five manufacturers accounting for about 40% of the market share. Among the various product segments, portable combustion analyzers hold the largest share, representing approximately 60% of the market. This dominance can be attributed to the versatility and convenience offered by portable devices, which are widely used across different sectors for on-site testing and analysis. The growth of the combustion analyzer market is driven by the increasing demand for energy efficiency and the need to comply with stringent environmental regulations. As industries and consumers alike seek to optimize their energy use and reduce emissions, the demand for reliable and accurate combustion analysis tools is expected to rise. The market is also benefiting from technological advancements, which are enhancing the capabilities and features of combustion analyzers, making them more user-friendly and efficient. Overall, the Global Combustion Analyzer Market is poised for sustained growth, driven by the ongoing pursuit of cleaner and more efficient energy solutions.

| Report Metric | Details |

| Report Name | Combustion Analyzer Market |

| CAGR | 4.5% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | AMETEK Process Instruments, Emerson Electric, Dragerwerk, ABB Measurement & Analytics, General Electric, TESTO, Bacharach, M&C Tech Gentics GmbH, Fuji Electric, Kane International, TECORA, ENOTEC, Seitron, KIMO Instruments, WOHLER, Wuhan Cubic Optoelectronic, CODEL International, UEI TEST INSTRUMENTS, Dwyer Instruments, MRU Instruments, Nova Analytical Systems, Shanghai Encel Instruments, Eurotron Instruments, Adev |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |