What is Global Tung Oil Market?

The Global Tung Oil Market is a fascinating sector that revolves around the production, distribution, and consumption of tung oil, a drying oil extracted from the seeds of the tung tree. This oil is renowned for its quick-drying properties and water-resistant finish, making it a popular choice in various industries. The market is driven by the demand for eco-friendly and sustainable products, as tung oil is a natural and biodegradable substance. It is primarily used in wood finishing, paints, and coatings, offering a durable and glossy finish. The market is influenced by factors such as the availability of raw materials, technological advancements in extraction and processing, and the growing awareness of environmental issues. The global reach of the tung oil market is expanding, with significant contributions from regions like North America and Asia, where the cultivation of tung trees is prevalent. As industries continue to seek sustainable alternatives, the demand for tung oil is expected to grow, making it a vital component in the global market for natural oils.

Raw Tung Oil, Boiled Tung Oil in the Global Tung Oil Market:

Raw tung oil and boiled tung oil are two primary forms of tung oil that cater to different needs within the Global Tung Oil Market. Raw tung oil is the purest form, extracted directly from the seeds of the tung tree without any additives or processing. It is known for its natural, clear finish and is often used in applications where a non-toxic and eco-friendly product is desired. Raw tung oil penetrates deeply into wood, providing a protective barrier that enhances the natural grain and color of the wood. It is favored by craftsmen and artisans who appreciate its natural properties and ability to preserve the authenticity of the wood. On the other hand, boiled tung oil undergoes a heating process that accelerates its drying time and enhances its durability. This form of tung oil is often mixed with chemical dryers to improve its performance in industrial applications. Boiled tung oil is commonly used in the production of varnishes, paints, and coatings, where a quick-drying and hard-wearing finish is required. It provides a glossy and water-resistant surface, making it ideal for outdoor furniture, decks, and other wooden structures exposed to the elements. The choice between raw and boiled tung oil depends on the specific requirements of the project, with raw tung oil being preferred for its natural and eco-friendly attributes, while boiled tung oil is chosen for its enhanced performance and durability. The Global Tung Oil Market continues to evolve as manufacturers and consumers seek products that balance environmental sustainability with high performance. The demand for both raw and boiled tung oil is influenced by trends in the construction, furniture, and automotive industries, where the emphasis is on sustainable materials and finishes. As the market grows, innovations in processing and application techniques are expected to further enhance the versatility and appeal of tung oil products.

Wood Finishing, Electronic in the Global Tung Oil Market:

The Global Tung Oil Market finds significant applications in areas such as wood finishing and electronics, where its unique properties are highly valued. In wood finishing, tung oil is prized for its ability to penetrate deeply into the wood, providing a durable and water-resistant finish that enhances the natural beauty of the wood grain. It is often used in the restoration of antique furniture, where preserving the original appearance is crucial. Tung oil's natural and non-toxic properties make it an ideal choice for finishing wooden toys, kitchen utensils, and other items that come into contact with food or children. Its ability to withstand moisture and resist mold and mildew makes it a popular choice for outdoor furniture and decking. In the electronics industry, tung oil is used as an insulating material due to its excellent dielectric properties. It is applied as a protective coating on electronic components to prevent moisture ingress and corrosion, ensuring the longevity and reliability of the devices. The oil's ability to form a flexible and durable film makes it suitable for use in flexible electronics, where maintaining the integrity of the components is essential. The demand for tung oil in these applications is driven by the growing emphasis on sustainability and the need for eco-friendly materials that do not compromise on performance. As industries continue to innovate and seek greener alternatives, the role of tung oil in wood finishing and electronics is expected to expand, offering new opportunities for growth in the Global Tung Oil Market.

Global Tung Oil Market Outlook:

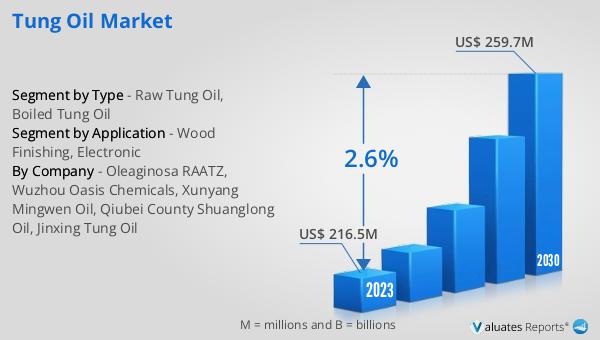

In 2024, the global market size of tung oil was valued at approximately US$ 228 million, with projections indicating a growth to around US$ 272 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 2.6% during the forecast period from 2025 to 2031. North America holds the largest share of the tung oil market, accounting for about 34% of the market share, followed by China, which represents approximately 23% of the market. The market is dominated by the top three companies, which collectively occupy about 58% of the market share. This concentration of market power suggests a competitive landscape where leading companies have a significant influence on market trends and pricing. The growth of the tung oil market is driven by the increasing demand for sustainable and eco-friendly products across various industries. As consumers and manufacturers alike prioritize environmental responsibility, the market for tung oil is poised for steady growth. The regional distribution of the market highlights the importance of North America and China as key players in the global tung oil industry, with their substantial market shares reflecting strong demand and production capabilities. The outlook for the Global Tung Oil Market suggests a promising future, with opportunities for expansion and innovation as the world continues to embrace sustainable practices.

| Report Metric | Details |

| Report Name | Tung Oil Market |

| CAGR | 2.6% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Oleaginosa RAATZ, Wuzhou Oasis Chemicals, Xunyang Mingwen Oil, Qiubei County Shuanglong Oil, Jinxing Tung Oil |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |