What is Global Boron Market?

The global boron market is a significant segment of the chemical industry, focusing on the extraction, processing, and distribution of boron and its compounds. Boron is a versatile element used in various applications due to its unique properties, such as high thermal resistance and the ability to form strong covalent bonds. The market is driven by the demand for boron in industries like glass, ceramics, agriculture, and detergents, among others. Boron is primarily extracted from borate minerals found in regions like Turkey, the United States, and South America. The market's growth is influenced by factors such as technological advancements, increasing demand for sustainable agricultural practices, and the expansion of the glass and ceramics industries. Additionally, environmental regulations and the need for efficient resource management play a crucial role in shaping the market dynamics. As industries continue to innovate and seek sustainable solutions, the global boron market is expected to evolve, offering new opportunities and challenges for stakeholders involved in the production and application of boron-based products.

Salt Lake Source, Mine Source in the Global Boron Market:

The global boron market sources its raw materials primarily from two main types: salt lake sources and mine sources. Salt lake sources refer to the extraction of boron from saline lakes, where borate minerals are dissolved in the water. These lakes, often found in arid regions, are rich in boron due to the natural evaporation process that concentrates the minerals. The extraction process involves pumping the saline water into evaporation ponds, where the water gradually evaporates, leaving behind borate-rich deposits. This method is considered environmentally friendly as it relies on natural processes and requires minimal energy input. However, it is dependent on climatic conditions and the availability of suitable lake sites, which can limit its scalability. On the other hand, mine sources involve the extraction of boron from underground deposits. This method is more traditional and involves mining operations to extract borate minerals from the earth. The extracted ore is then processed to separate the boron compounds from other minerals. Mining operations can be more energy-intensive and have a larger environmental footprint compared to salt lake extraction. However, they offer a more consistent and reliable supply of boron, as they are less affected by climatic variations. The choice between salt lake and mine sources depends on various factors, including the geographical location, environmental considerations, and economic viability. In regions where salt lakes are abundant, such as parts of South America and Asia, salt lake extraction is often preferred due to its lower environmental impact and cost-effectiveness. Conversely, in areas where boron deposits are located underground, mining operations are more prevalent. The global boron market relies on a combination of these sources to meet the growing demand for boron-based products. As the market continues to expand, there is a need for sustainable and efficient extraction methods to ensure a steady supply of boron while minimizing environmental impact. Innovations in extraction technologies and resource management practices are crucial for the future growth and sustainability of the boron market.

Glass, Ceramics, Agriculture, Detergents, Others in the Global Boron Market:

Boron is a critical component in various industries, with its applications spanning across glass, ceramics, agriculture, detergents, and other sectors. In the glass industry, boron is used to produce borosilicate glass, known for its high thermal resistance and durability. This type of glass is commonly used in laboratory equipment, cookware, and lighting products. The addition of boron enhances the glass's resistance to thermal shock, making it ideal for applications that require exposure to high temperatures. In the ceramics industry, boron is used as a fluxing agent, reducing the melting temperature of ceramic materials and improving their mechanical properties. This results in stronger, more durable ceramic products that are used in various applications, including tiles, sanitary ware, and electrical insulators. In agriculture, boron is an essential micronutrient for plant growth, playing a vital role in cell wall formation and the development of reproductive structures. Boron deficiency can lead to reduced crop yields and poor plant health, making it a crucial component of fertilizers and soil amendments. In the detergent industry, boron compounds are used as bleaching agents and water softeners, enhancing the cleaning efficiency of detergents. Boron-based detergents are effective in removing stains and maintaining the brightness of fabrics. Additionally, boron finds applications in other sectors, such as metallurgy, where it is used as an alloying agent to improve the hardness and strength of metals. It is also used in the production of boron fibers, which are lightweight and strong, making them suitable for aerospace and defense applications. The versatility of boron and its compounds makes it an indispensable element in various industries, driving the demand for boron-based products globally. As industries continue to innovate and develop new applications for boron, the global boron market is expected to grow, offering new opportunities for manufacturers and suppliers.

Global Boron Market Outlook:

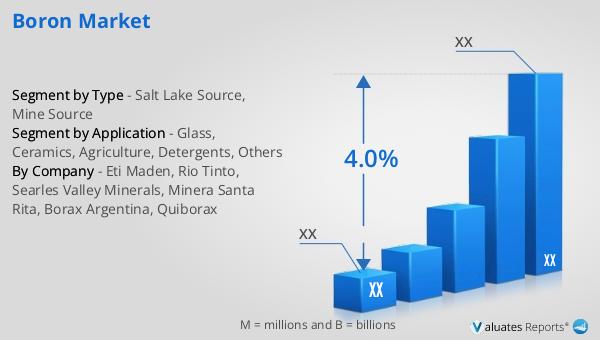

In 2024, the global boron market was valued at approximately US$ 2,672 million, with projections indicating that it could reach around US$ 3,503 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.0% during the forecast period from 2025 to 2031. Turkey stands out as the leading producer of boron, holding a significant market share of about 45%. This dominance is attributed to the country's rich borate mineral reserves and well-established extraction and processing infrastructure. Following Turkey, North America holds a substantial market share of 30%, driven by the presence of major boron producers and a strong demand for boron-based products in various industries. The global boron market is characterized by the presence of key players such as Etimine, Rio Tinto, and Searles Valley Minerals, who collectively account for approximately 75% of the market share. These companies have established themselves as leaders in the industry through their extensive product portfolios, strategic partnerships, and continuous investments in research and development. The market's growth is supported by the increasing demand for boron in applications such as glass, ceramics, agriculture, and detergents, as well as the development of new technologies and sustainable practices. As the market continues to evolve, stakeholders are focusing on enhancing their production capabilities, expanding their geographical presence, and exploring new applications for boron to capitalize on the growing demand.

| Report Metric | Details |

| Report Name | Boron Market |

| CAGR | 4.0% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Eti Maden, Rio Tinto, Searles Valley Minerals, Minera Santa Rita, Borax Argentina, Quiborax |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |