What is Global Borderless Display Panel Market?

The Global Borderless Display Panel Market refers to the industry focused on producing and distributing display panels that have minimal or no visible borders, providing a seamless viewing experience. These panels are increasingly popular in various electronic devices, such as smartphones, televisions, and computer monitors, due to their sleek and modern design. The demand for borderless display panels is driven by consumer preferences for larger screens and enhanced visual aesthetics, as well as technological advancements that allow for thinner and more efficient displays. Manufacturers are continuously innovating to improve the quality and functionality of these panels, incorporating features like higher resolution, better color accuracy, and energy efficiency. The market is also influenced by the growing trend of smart devices and the Internet of Things (IoT), which require advanced display technologies. As a result, the Global Borderless Display Panel Market is expected to see significant growth, with companies investing in research and development to meet the evolving needs of consumers and businesses alike. This market is characterized by intense competition, with key players striving to gain a competitive edge through product differentiation and strategic partnerships.

OLED, LCD, Others in the Global Borderless Display Panel Market:

In the Global Borderless Display Panel Market, various technologies are employed to create the seamless screens that consumers desire. Among these, OLED (Organic Light Emitting Diode) and LCD (Liquid Crystal Display) are the most prominent, each offering distinct advantages and challenges. OLED technology is renowned for its ability to produce vibrant colors and deep blacks, thanks to its self-lighting pixels that eliminate the need for a backlight. This results in thinner and more flexible displays, making OLED a popular choice for high-end smartphones and televisions. However, OLED panels can be more expensive to produce and may suffer from issues like burn-in, where static images can leave a permanent mark on the screen. On the other hand, LCD technology, which uses a backlight to illuminate pixels, is more cost-effective and widely used in a variety of devices. LCD panels offer good color reproduction and brightness, making them suitable for environments with high ambient light. They are also less prone to burn-in compared to OLED displays. However, LCDs are generally thicker and less flexible, which can limit their application in certain devices. Beyond OLED and LCD, other technologies are emerging in the borderless display market. For instance, MicroLED is gaining attention for its potential to combine the best features of OLED and LCD. MicroLED displays use microscopic LEDs to create images, offering high brightness, excellent color accuracy, and energy efficiency without the risk of burn-in. However, the technology is still in its early stages and can be costly to manufacture. Another emerging technology is Quantum Dot, which enhances the color and brightness of LCD panels by using nanocrystals that emit specific wavelengths of light. This technology is being integrated into some high-end televisions and monitors, providing a competitive edge in the market. As the Global Borderless Display Panel Market continues to evolve, manufacturers are exploring these and other technologies to meet the growing demand for high-quality, borderless displays. The choice of technology often depends on the specific application and consumer preferences, with factors like cost, performance, and durability playing a crucial role in decision-making. Companies are also investing in research and development to overcome the limitations of existing technologies and to innovate new solutions that can offer even better performance and aesthetics. The competition among different display technologies is driving innovation and pushing the boundaries of what is possible in the realm of borderless displays. As a result, consumers can expect to see continued improvements in the quality and functionality of the devices they use every day, from smartphones and computers to televisions and beyond.

Smartphone, Computer, TV, Others in the Global Borderless Display Panel Market:

The usage of Global Borderless Display Panels spans across various devices, significantly enhancing the user experience in smartphones, computers, televisions, and other electronic gadgets. In smartphones, borderless displays have become a hallmark of modern design, offering users a larger screen area without increasing the overall size of the device. This is particularly appealing for activities like gaming, video streaming, and multitasking, where a larger display can provide a more immersive experience. Manufacturers are leveraging borderless designs to differentiate their products in a highly competitive market, often combining them with advanced features like high refresh rates and HDR support to attract tech-savvy consumers. In the realm of computers, borderless display panels are increasingly being used in monitors and laptops. For monitors, a borderless design allows for a more seamless multi-monitor setup, which is beneficial for professionals who require extensive screen real estate for tasks such as video editing, graphic design, and financial analysis. In laptops, borderless displays contribute to a more compact and portable design, making them ideal for users who need to work on the go. The aesthetic appeal of borderless screens also plays a role in consumer choice, as they offer a modern and sleek look that complements contemporary workspaces. Televisions are another area where borderless display panels are making a significant impact. With the rise of streaming services and high-definition content, consumers are seeking larger and more immersive screens for their home entertainment systems. Borderless TVs provide a cinematic viewing experience by maximizing the screen area and minimizing distractions from bezels. This trend is particularly evident in high-end models, where manufacturers are incorporating advanced technologies like OLED and Quantum Dot to deliver superior picture quality. The demand for borderless TVs is also driven by the growing popularity of smart TVs, which integrate internet connectivity and interactive features, further enhancing the viewing experience. Beyond smartphones, computers, and televisions, borderless display panels are finding applications in other areas such as digital signage, automotive displays, and wearable devices. In digital signage, borderless displays offer a sleek and modern look that can attract attention in retail environments, airports, and public spaces. Automotive displays are increasingly adopting borderless designs to provide drivers with a more integrated and intuitive interface for navigation, entertainment, and vehicle information. Wearable devices, such as smartwatches and fitness trackers, benefit from borderless displays by offering a larger screen area in a compact form factor, improving usability and aesthetics. As the Global Borderless Display Panel Market continues to grow, the versatility and appeal of these displays are expected to drive their adoption across a wide range of applications, enhancing the user experience and setting new standards for design and functionality.

Global Borderless Display Panel Market Outlook:

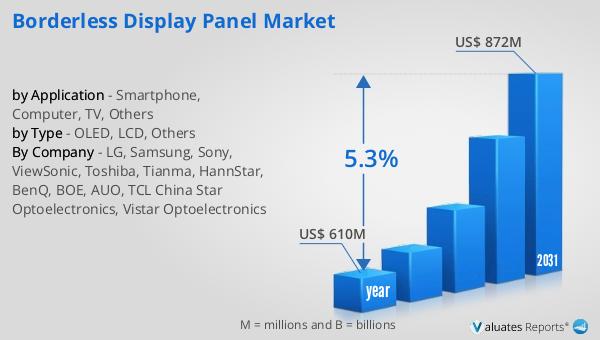

The outlook for the Global Borderless Display Panel Market indicates a promising future, with significant growth anticipated over the coming years. In 2024, the market was valued at approximately $610 million, reflecting the increasing demand for sleek and modern display solutions across various industries. This demand is driven by consumer preferences for larger screens and enhanced visual aesthetics, as well as technological advancements that allow for thinner and more efficient displays. As manufacturers continue to innovate and improve the quality and functionality of borderless display panels, the market is projected to expand further. By 2031, the market size is expected to reach around $872 million, growing at a compound annual growth rate (CAGR) of 5.3% during the forecast period. This growth is indicative of the ongoing trend towards borderless designs in electronic devices, as well as the increasing adoption of advanced display technologies such as OLED, MicroLED, and Quantum Dot. The competitive landscape of the market is characterized by intense competition, with key players striving to gain a competitive edge through product differentiation and strategic partnerships. As a result, consumers can expect to see continued improvements in the quality and functionality of the devices they use every day, from smartphones and computers to televisions and beyond. The Global Borderless Display Panel Market is poised to play a crucial role in shaping the future of display technology, offering consumers and businesses alike a wide range of innovative and high-quality solutions.

| Report Metric | Details |

| Report Name | Borderless Display Panel Market |

| Accounted market size in year | US$ 610 million |

| Forecasted market size in 2031 | US$ 872 million |

| CAGR | 5.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | LG, Samsung, Sony, ViewSonic, Toshiba, Tianma, HannStar, BenQ, BOE, AUO, TCL China Star Optoelectronics, Vistar Optoelectronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |