What is Global Automotive Stand Alone Accelerometer Market?

The Global Automotive Stand Alone Accelerometer Market refers to the segment of the automotive industry that focuses on the production and sale of accelerometers used independently within vehicles. These devices are crucial for measuring acceleration forces, which can be used to monitor vehicle dynamics, enhance safety features, and improve overall vehicle performance. Stand-alone accelerometers are distinct from those integrated into other systems, offering more precise and dedicated measurements. They play a vital role in various automotive applications, such as airbag deployment, electronic stability control, and navigation systems. The market for these accelerometers is driven by the increasing demand for advanced safety features and the growing trend of vehicle electrification. As automotive technology continues to evolve, the need for accurate and reliable acceleration data becomes more critical, making stand-alone accelerometers an essential component in modern vehicles. The market is characterized by technological advancements, competitive pricing, and a focus on innovation to meet the diverse needs of automotive manufacturers and consumers alike.

MEMS Accelerometer, Piezoelectric Accelerometer in the Global Automotive Stand Alone Accelerometer Market:

MEMS (Micro-Electro-Mechanical Systems) accelerometers and piezoelectric accelerometers are two primary types of sensors used in the Global Automotive Stand Alone Accelerometer Market. MEMS accelerometers are widely used due to their small size, low cost, and high reliability. They work by detecting changes in capacitance caused by the movement of a micro-machined structure within the sensor. This change in capacitance is then converted into an electrical signal that represents the acceleration. MEMS accelerometers are highly versatile and can be used in various automotive applications, including airbag systems, electronic stability control, and navigation systems. Their ability to provide accurate and reliable data makes them an essential component in modern vehicles. On the other hand, piezoelectric accelerometers operate based on the piezoelectric effect, where certain materials generate an electrical charge in response to mechanical stress. These accelerometers are known for their high sensitivity and wide frequency range, making them suitable for applications that require precise measurements of dynamic forces. In the automotive industry, piezoelectric accelerometers are often used in vibration analysis, engine monitoring, and suspension systems. While they are generally more expensive than MEMS accelerometers, their superior performance in specific applications justifies the cost. Both MEMS and piezoelectric accelerometers play a crucial role in the automotive industry, providing the necessary data to enhance vehicle safety, performance, and comfort. As the demand for advanced automotive technologies continues to grow, the market for these accelerometers is expected to expand, driven by innovations in sensor technology and the increasing integration of electronic systems in vehicles. The choice between MEMS and piezoelectric accelerometers depends on the specific requirements of the application, with factors such as cost, size, sensitivity, and frequency range influencing the decision. Overall, the Global Automotive Stand Alone Accelerometer Market is poised for significant growth, driven by the increasing demand for advanced safety features and the continuous evolution of automotive technology.

Passenger Car, Commercial Car in the Global Automotive Stand Alone Accelerometer Market:

The usage of Global Automotive Stand Alone Accelerometer Market in passenger cars and commercial vehicles is extensive and varied, reflecting the diverse needs and requirements of these two segments. In passenger cars, stand-alone accelerometers are primarily used to enhance safety and comfort. They are integral to systems such as airbags, where they detect sudden deceleration and trigger the deployment of airbags to protect occupants during a collision. Additionally, accelerometers are used in electronic stability control systems to monitor vehicle dynamics and prevent skidding or loss of control. This is particularly important in passenger cars, where safety is a top priority for consumers. Furthermore, accelerometers are used in navigation systems to provide accurate positioning data, improving the overall driving experience. In commercial vehicles, the focus is often on performance and efficiency. Stand-alone accelerometers are used in engine monitoring systems to detect vibrations and identify potential issues before they lead to costly repairs or downtime. This is crucial for fleet operators who need to maintain the reliability and efficiency of their vehicles. Additionally, accelerometers are used in suspension systems to monitor and adjust the ride quality, ensuring that commercial vehicles can handle varying loads and road conditions. This is particularly important for heavy-duty trucks and buses, where stability and comfort are essential for both drivers and passengers. Overall, the usage of stand-alone accelerometers in passenger cars and commercial vehicles highlights their versatility and importance in the automotive industry. As technology continues to advance, the demand for these sensors is expected to grow, driven by the need for improved safety, performance, and efficiency in both segments.

Global Automotive Stand Alone Accelerometer Market Outlook:

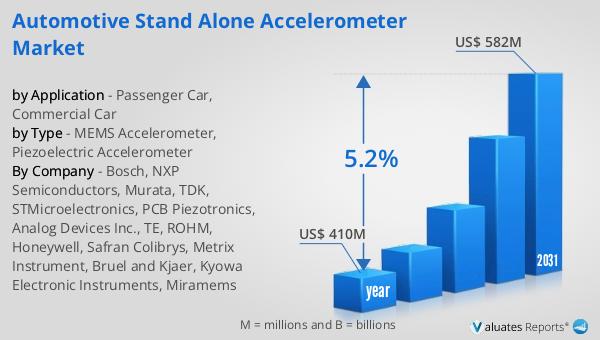

The global market for Automotive Stand Alone Accelerometer was valued at approximately $410 million in 2024, and it is anticipated to grow to a revised size of around $582 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.2% over the forecast period. This upward trend is indicative of the increasing demand for advanced automotive technologies and the critical role that accelerometers play in enhancing vehicle safety and performance. The market's expansion is driven by several factors, including the growing adoption of electronic systems in vehicles, the rising demand for advanced safety features, and the continuous evolution of automotive technology. As vehicles become more sophisticated, the need for accurate and reliable acceleration data becomes more pronounced, making stand-alone accelerometers an essential component in modern vehicles. The market is characterized by technological advancements, competitive pricing, and a focus on innovation to meet the diverse needs of automotive manufacturers and consumers alike. As the automotive industry continues to evolve, the Global Automotive Stand Alone Accelerometer Market is poised for significant growth, driven by the increasing demand for advanced safety features and the continuous evolution of automotive technology.

| Report Metric | Details |

| Report Name | Automotive Stand Alone Accelerometer Market |

| Accounted market size in year | US$ 410 million |

| Forecasted market size in 2031 | US$ 582 million |

| CAGR | 5.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bosch, NXP Semiconductors, Murata, TDK, STMicroelectronics, PCB Piezotronics, Analog Devices Inc., TE, ROHM, Honeywell, Safran Colibrys, Metrix Instrument, Bruel and Kjaer, Kyowa Electronic Instruments, Miramems |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |