What is Global Road Inspection Vehicle Market?

The Global Road Inspection Vehicle Market is a specialized segment within the broader automotive and infrastructure sectors, focusing on vehicles designed to assess and monitor the condition of roadways. These vehicles are equipped with advanced technologies such as high-resolution cameras, laser scanners, and ground-penetrating radar to detect and analyze road surface conditions, structural integrity, and potential hazards. The primary goal of these vehicles is to ensure road safety and maintenance efficiency by providing accurate and timely data to road authorities and maintenance teams. As infrastructure ages and traffic volumes increase, the demand for road inspection vehicles is expected to grow, driven by the need for regular and thorough inspections to prevent accidents and costly repairs. These vehicles play a crucial role in maintaining the quality and safety of roads, highways, and other transportation networks, making them an essential tool for governments and private road management companies worldwide. By leveraging cutting-edge technology, road inspection vehicles help in extending the lifespan of road infrastructure and optimizing maintenance budgets, ultimately contributing to safer and more reliable transportation systems.

Mounted on Special Vehicle, Mounted on General Vehicle in the Global Road Inspection Vehicle Market:

In the Global Road Inspection Vehicle Market, vehicles can be categorized based on their mounting type: Mounted on Special Vehicle and Mounted on General Vehicle. Vehicles mounted on special vehicles are custom-designed and built specifically for road inspection purposes. These vehicles are often equipped with specialized equipment and technology tailored to the unique requirements of road inspection tasks. They may include features such as advanced imaging systems, laser scanning devices, and data processing units that are integrated into the vehicle's design. The advantage of using special vehicles is their ability to provide highly accurate and detailed data, as they are engineered to accommodate the specific needs of road inspection. These vehicles are typically used in scenarios where precision and comprehensive data collection are paramount, such as in the inspection of critical infrastructure or in regions with complex road networks. On the other hand, vehicles mounted on general vehicles are standard vehicles that have been modified or equipped with road inspection equipment. These vehicles offer a more flexible and cost-effective solution for road inspection tasks, as they can be easily adapted to different inspection requirements and can be used for other purposes when not engaged in inspection activities. General vehicles are often used in routine inspections or in areas where the road network is less complex, and the need for specialized equipment is not as critical. The choice between special and general vehicles depends on various factors, including the specific requirements of the inspection task, budget constraints, and the availability of technology. Both types of vehicles play a vital role in the Global Road Inspection Vehicle Market, providing essential data that helps in maintaining and improving road infrastructure. As technology continues to advance, the capabilities of both special and general vehicles are expected to evolve, offering even more sophisticated solutions for road inspection.

Road, Highway, Airport Runway, Others in the Global Road Inspection Vehicle Market:

The Global Road Inspection Vehicle Market finds its application in various areas, including roads, highways, airport runways, and other infrastructure. On roads, these vehicles are used to monitor surface conditions, identify potholes, cracks, and other defects that could pose safety risks to motorists. By providing real-time data on road conditions, inspection vehicles enable timely maintenance and repairs, reducing the likelihood of accidents and extending the lifespan of road surfaces. On highways, where traffic volumes are higher and speeds are greater, the role of inspection vehicles becomes even more critical. They help in identifying structural weaknesses and potential hazards that could lead to serious accidents or traffic disruptions. By ensuring that highways are in optimal condition, these vehicles contribute to smoother and safer travel for commuters and freight transport. In the context of airport runways, road inspection vehicles play a crucial role in maintaining the safety and efficiency of air travel. Runways are subject to significant wear and tear due to the heavy loads and high speeds of aircraft landings and takeoffs. Inspection vehicles equipped with advanced sensors and imaging technology can detect surface irregularities and structural issues that could compromise the safety of aircraft operations. By facilitating regular inspections and maintenance, these vehicles help in preventing accidents and ensuring the smooth operation of airport facilities. Beyond roads, highways, and runways, road inspection vehicles are also used in other areas such as bridges, tunnels, and parking lots. In these contexts, they provide valuable data that aids in the maintenance and management of infrastructure, ensuring safety and reliability for users. Overall, the Global Road Inspection Vehicle Market plays a vital role in maintaining the integrity and safety of transportation networks, supporting the efficient movement of people and goods.

Global Road Inspection Vehicle Market Outlook:

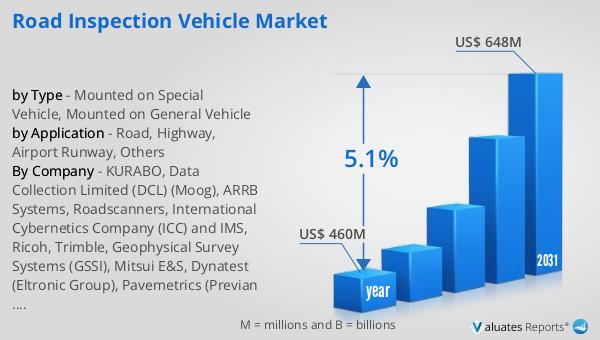

The global market for Road Inspection Vehicles was valued at approximately $460 million in 2024. This market is anticipated to expand significantly, reaching an estimated size of $648 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.1% over the forecast period. The increasing demand for road inspection vehicles is driven by the need for enhanced road safety and maintenance efficiency. As infrastructure ages and traffic volumes rise, the importance of regular and thorough road inspections becomes more pronounced. Road inspection vehicles, equipped with advanced technologies, provide critical data that aids in the timely maintenance and repair of roadways, thereby preventing accidents and reducing long-term repair costs. The projected growth in the market reflects the increasing recognition of the value that these vehicles bring to road management and maintenance efforts. By investing in road inspection vehicles, governments and private road management companies can optimize their maintenance budgets and extend the lifespan of their infrastructure. This market outlook underscores the growing importance of road inspection vehicles in ensuring the safety and reliability of transportation networks worldwide.

| Report Metric | Details |

| Report Name | Road Inspection Vehicle Market |

| Accounted market size in year | US$ 460 million |

| Forecasted market size in 2031 | US$ 648 million |

| CAGR | 5.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | KURABO, Data Collection Limited (DCL) (Moog), ARRB Systems, Roadscanners, International Cybernetics Company (ICC) and IMS, Ricoh, Trimble, Geophysical Survey Systems (GSSI), Mitsui E&S, Dynatest (Eltronic Group), Pavemetrics (Previan Technologies), ELAG Elektronik, RoadMainT, Wuhan ZOYON, Shanghai Pres Highway and Traffic Technology, Beijing Zhongtian Hengyu, Wuhan XROE, Hunan Lianzhi Technology, Shanxi Yicun Transportation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |