What is Global HD Map for Autonomous Driving Market?

The Global HD Map for Autonomous Driving Market is a rapidly evolving sector that plays a crucial role in the development and deployment of autonomous vehicles. HD maps, or high-definition maps, are detailed digital representations of the road environment, providing essential data that enhances the navigation and safety of self-driving cars. These maps include precise information about road geometry, lane configurations, traffic signs, and other critical elements that autonomous vehicles need to understand their surroundings and make informed driving decisions. As the demand for autonomous driving technology grows, the need for accurate and up-to-date HD maps becomes increasingly important. These maps are continuously updated using data from various sources, including sensors on vehicles and satellite imagery, to ensure they reflect real-world conditions. The market for HD maps is driven by advancements in technology, increasing investments in autonomous vehicle development, and the growing emphasis on road safety. As a result, the Global HD Map for Autonomous Driving Market is poised for significant growth, with numerous companies and stakeholders investing in the creation and refinement of these essential tools for the future of transportation.

Crowdsourcing Model, Centralized Mode in the Global HD Map for Autonomous Driving Market:

The Crowdsourcing Model and Centralized Mode are two prominent approaches within the Global HD Map for Autonomous Driving Market, each offering unique advantages and challenges. The Crowdsourcing Model relies on data collected from a vast network of vehicles equipped with sensors and cameras. These vehicles continuously gather information about their surroundings, such as road conditions, traffic patterns, and changes in infrastructure. This data is then aggregated and processed to update HD maps in real-time. The primary advantage of the Crowdsourcing Model is its ability to provide up-to-date and highly detailed maps, as it leverages the collective input of numerous vehicles on the road. This approach is particularly effective in rapidly changing environments, where traditional mapping methods may struggle to keep pace. However, the Crowdsourcing Model also presents challenges, such as ensuring data accuracy and consistency, as well as addressing privacy concerns related to the collection and use of vehicle data. On the other hand, the Centralized Mode involves the creation and maintenance of HD maps by specialized mapping companies or organizations. These entities use advanced technologies, such as LiDAR and aerial imagery, to capture detailed information about the road environment. The data is then processed and compiled into comprehensive HD maps, which are distributed to autonomous vehicles. The Centralized Mode offers the advantage of producing highly accurate and reliable maps, as the data is collected and verified by experts in the field. Additionally, this approach allows for greater control over data quality and security, as the mapping process is managed by a centralized entity. However, the Centralized Mode may face challenges in terms of scalability and responsiveness, as updating maps to reflect real-time changes can be a resource-intensive process. Both the Crowdsourcing Model and Centralized Mode play vital roles in the Global HD Map for Autonomous Driving Market, and the choice between them often depends on factors such as the specific requirements of autonomous vehicle systems, the availability of resources, and the desired level of map accuracy and detail. As the market continues to evolve, it is likely that a combination of these approaches will be used to create the most effective and comprehensive HD maps for autonomous driving.

L1/L2+ Driving Automation, L3 Driving Automation, Others in the Global HD Map for Autonomous Driving Market:

The Global HD Map for Autonomous Driving Market finds its application across various levels of driving automation, including L1/L2+ Driving Automation, L3 Driving Automation, and others. In the context of L1/L2+ Driving Automation, HD maps play a supportive role by providing enhanced situational awareness and aiding in the execution of advanced driver assistance systems (ADAS). These systems, which include features like adaptive cruise control and lane-keeping assistance, rely on HD maps to accurately interpret road conditions and make informed decisions. By offering precise information about road geometry, traffic signs, and lane configurations, HD maps enable L1/L2+ systems to function more effectively, improving safety and convenience for drivers. As vehicles progress to L3 Driving Automation, the reliance on HD maps becomes even more critical. At this level, vehicles are capable of performing most driving tasks autonomously, but human intervention may still be required in certain situations. HD maps provide the necessary data for L3 systems to navigate complex environments, such as urban areas and highways, with a high degree of accuracy. These maps help vehicles understand their surroundings, anticipate potential hazards, and make real-time adjustments to their driving behavior. The use of HD maps in L3 Driving Automation is essential for ensuring the safety and reliability of autonomous vehicles, as they transition from human-assisted to fully autonomous operation. Beyond L1/L2+ and L3 Driving Automation, HD maps are also utilized in other areas of autonomous driving, such as fleet management and logistics. In these applications, HD maps enable efficient route planning and optimization, helping companies reduce operational costs and improve delivery times. By providing detailed information about road networks and traffic conditions, HD maps allow fleet operators to make data-driven decisions that enhance the overall efficiency of their operations. Additionally, HD maps are used in the development and testing of autonomous vehicle technologies, serving as a critical tool for simulation and validation processes. As the Global HD Map for Autonomous Driving Market continues to expand, the use of these maps across various levels of driving automation and related applications will play a pivotal role in shaping the future of transportation.

Global HD Map for Autonomous Driving Market Outlook:

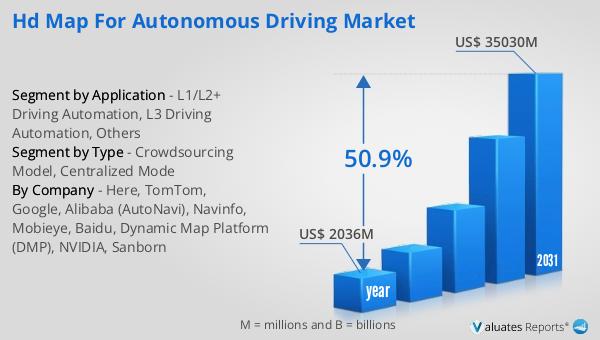

The global market for HD Maps tailored for Autonomous Driving was valued at approximately USD 2,968 million in 2024, with projections indicating a significant expansion to a revised size of USD 51,080 million by 2031. This growth trajectory reflects a robust compound annual growth rate (CAGR) of 50.9% over the forecast period. A notable aspect of this market is the concentration of market share among the top five manufacturers, who collectively hold over 80% of the market. This indicates a competitive landscape dominated by a few key players who are likely driving innovation and setting industry standards. Within the product segments, the crowdsourcing model emerges as the largest, commanding a share exceeding 72%. This model's prominence underscores the industry's reliance on real-time data collection from a network of vehicles to maintain up-to-date and accurate maps. In terms of application, L1/L2 driving automation is the most significant segment, with a staggering share of over 99%. This highlights the current focus of HD map applications on enhancing advanced driver assistance systems (ADAS) and supporting semi-autonomous driving technologies. As the market evolves, these dynamics are expected to shape the development and deployment of HD maps, influencing the broader landscape of autonomous driving technology.

| Report Metric | Details |

| Report Name | HD Map for Autonomous Driving Market |

| Accounted market size in year | US$ 2968 million |

| Forecasted market size in 2031 | US$ 51080 million |

| CAGR | 50.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Here, TomTom, Google, Alibaba (AutoNavi), Navinfo, Mobieye, Baidu, Dynamic Map Platform (DMP), NVIDIA, Sanborn |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |