What is Global Neon Market?

The Global Neon Market is a fascinating segment of the industrial gas industry, primarily driven by its unique properties and diverse applications. Neon is a noble gas, known for its inertness and distinct reddish-orange glow when electrified. It is extracted from the atmosphere through a process of fractional distillation of liquid air, which is a complex and energy-intensive procedure. The market for neon is influenced by its demand in various sectors such as electronics, lighting, and signage. The semiconductor industry, in particular, is a significant consumer of neon, as it is used in the manufacturing of chips and other electronic components. Additionally, neon is utilized in laser technology, where its properties are harnessed for precision cutting and medical applications. The market dynamics are shaped by factors such as technological advancements, economic conditions, and regulatory policies. The supply chain for neon is relatively concentrated, with a few key players dominating the market. This concentration can lead to price volatility, especially during periods of increased demand or supply disruptions. Overall, the Global Neon Market is a vital component of the broader industrial gas sector, with its growth closely tied to technological and industrial developments.

<5N, 5N, >5N in the Global Neon Market:

In the Global Neon Market, purity levels are a critical factor that determines the suitability of neon for various applications. The terms <5N, 5N, and >5N refer to the purity levels of neon gas, with 'N' representing the number of nines in the purity percentage. For instance, 5N neon has a purity of 99.999%, while <5N indicates a purity level below 99.999%, and >5N signifies a purity level above 99.999%. Each of these purity levels serves different industrial needs. <5N neon, with its lower purity, is often used in applications where ultra-high purity is not essential, such as in some types of lighting and signage. This level of purity is sufficient for creating the vibrant colors associated with neon lights, which are popular in advertising and artistic displays. However, the presence of impurities can affect the color and brightness of the light, making it less desirable for high-precision applications. On the other hand, 5N neon is the standard for most industrial applications, including the semiconductor industry. The high purity level ensures that there are minimal impurities that could interfere with the manufacturing processes of electronic components. In semiconductor manufacturing, neon is used in excimer lasers, which are essential for photolithography, a process that involves etching intricate patterns onto silicon wafers. The presence of impurities in the neon gas could lead to defects in the semiconductor chips, affecting their performance and reliability. Therefore, maintaining a high level of purity is crucial in this context. >5N neon, with its ultra-high purity, is used in the most demanding applications where even the slightest impurity could have significant consequences. This level of purity is often required in advanced laser technologies and certain medical applications. In laser technology, for instance, the presence of impurities can affect the laser's precision and efficiency, which is critical in applications such as eye surgery and precision cutting. Similarly, in medical applications, the use of ultra-high purity neon ensures that there are no contaminants that could pose a risk to patient safety. The production of >5N neon requires advanced purification techniques and stringent quality control measures, making it more expensive than lower purity levels. The demand for different purity levels of neon is influenced by the specific requirements of various industries. As technology advances and the need for precision and reliability increases, the demand for higher purity neon is expected to grow. However, the production of ultra-high purity neon is challenging and requires significant investment in technology and infrastructure. This can lead to supply constraints and price fluctuations, particularly in times of increased demand. The Global Neon Market is thus characterized by a delicate balance between supply and demand, with purity levels playing a crucial role in determining market dynamics.

Semiconductor, Laser, Fluorescent Light Bulbs, Signage, Others in the Global Neon Market:

The Global Neon Market finds its usage across a variety of sectors, each leveraging the unique properties of neon to meet specific needs. In the semiconductor industry, neon plays a pivotal role in the manufacturing of microchips and other electronic components. It is used in excimer lasers, which are crucial for the photolithography process. This process involves etching intricate patterns onto silicon wafers, a fundamental step in chip production. The high purity of neon ensures that the lasers operate with precision, minimizing defects in the chips and enhancing their performance and reliability. The demand for neon in this sector is driven by the continuous advancement in technology and the increasing complexity of electronic devices. In the field of laser technology, neon is used in gas lasers, where it serves as a medium for generating laser light. These lasers are employed in a range of applications, from precision cutting and welding in industrial settings to medical procedures such as eye surgery. The inert nature of neon makes it an ideal choice for these applications, as it does not react with other substances and maintains the stability of the laser beam. The use of neon in lasers is expected to grow as industries seek more efficient and precise cutting and manufacturing techniques. Neon is also a key component in fluorescent light bulbs, where it is used to produce light through the excitation of gas molecules. When an electric current passes through the neon gas, it emits a bright glow, which is then converted into visible light by the phosphor coating inside the bulb. This technology is widely used in commercial and residential lighting due to its energy efficiency and long lifespan. The demand for neon in this sector is influenced by trends in energy conservation and the shift towards more sustainable lighting solutions. In the realm of signage, neon lights are renowned for their vibrant colors and eye-catching displays. They are a popular choice for advertising and artistic installations, providing a unique aesthetic appeal that is difficult to replicate with other lighting technologies. The flexibility of neon tubes allows for the creation of intricate designs and lettering, making them a versatile option for businesses looking to attract attention. The use of neon in signage is driven by the need for distinctive and memorable branding, as well as the enduring appeal of neon's retro aesthetic. Beyond these applications, neon is used in a variety of other areas, including scientific research and cryogenics. In research settings, neon is used as a coolant in cryogenic experiments due to its low boiling point and inert properties. It is also used in the calibration of scientific instruments, where its stable and predictable behavior is an asset. The versatility of neon and its unique properties make it a valuable resource across multiple industries, with its usage continuing to evolve as new technologies and applications emerge.

Global Neon Market Outlook:

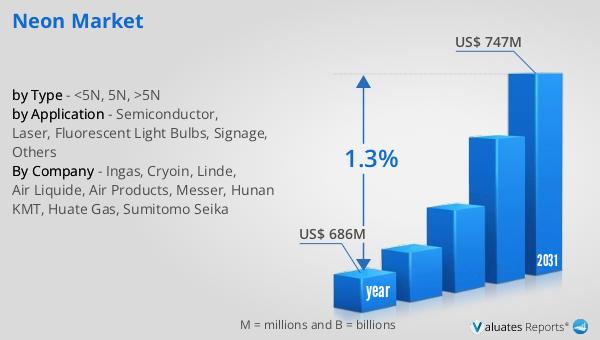

In 2024, the global market for neon was valued at approximately $686 million, and it is anticipated to grow to a revised size of $747 million by 2031, reflecting a compound annual growth rate (CAGR) of 1.3% over the forecast period. This growth trajectory highlights the steady demand for neon across various industries, despite the challenges associated with its production and supply. The market is dominated by a few key players, with the top five manufacturers accounting for nearly 70% of the market share. These leading companies include Ingas, Linde, Air Liquide, and Air Products, among others. Their dominance is attributed to their advanced production capabilities and extensive distribution networks, which enable them to meet the global demand for neon efficiently. The Asia Pacific region emerges as the largest producer of neon, holding a significant share of approximately 65%. This dominance is driven by the region's robust industrial base and the presence of major semiconductor manufacturing hubs, which are key consumers of neon. Following Asia Pacific, North America and Europe also contribute to the global neon market, albeit to a lesser extent. The concentration of production in these regions underscores the strategic importance of neon in supporting technological advancements and industrial growth. As the market continues to evolve, the focus remains on enhancing production efficiency and ensuring a stable supply to meet the diverse needs of industries worldwide.

| Report Metric | Details |

| Report Name | Neon Market |

| Accounted market size in year | US$ 686 million |

| Forecasted market size in 2031 | US$ 747 million |

| CAGR | 1.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Ingas, Cryoin, Linde, Air Liquide, Air Products, Messer, Hunan KMT, Huate Gas, Sumitomo Seika |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |