What is Global Broiler Farming Market?

The Global Broiler Farming Market refers to the worldwide industry focused on the breeding and raising of broiler chickens, which are specifically bred for meat production. Broilers are a type of chicken that grow rapidly and are typically ready for market within six to seven weeks. This market is a significant segment of the poultry industry, driven by the increasing demand for chicken meat due to its affordability, nutritional value, and versatility in cooking. The market encompasses various stages, including breeding, hatching, raising, processing, and distribution. It is influenced by factors such as consumer preferences, technological advancements in farming practices, and regulatory policies. The global nature of this market means it is subject to international trade dynamics, with major producers and exporters like the United States, China, and Brazil playing pivotal roles. The market is also impacted by issues such as animal welfare, environmental concerns, and the need for sustainable farming practices. As the demand for protein continues to rise globally, the broiler farming market is expected to grow, adapting to changing consumer trends and technological innovations.

Fresh & Frozen, Processed in the Global Broiler Farming Market:

In the Global Broiler Farming Market, the categories of fresh and frozen, as well as processed broiler products, play crucial roles in meeting diverse consumer needs. Fresh broiler products are those that have not been subjected to freezing and are typically sold in local markets or through direct retail channels. These products are favored for their perceived quality and taste, as they are often considered to be more natural and less processed. Fresh broiler meat is popular in regions where consumers prefer to purchase meat that is freshly slaughtered and have access to local markets or butcher shops. On the other hand, frozen broiler products are those that have been preserved through freezing, allowing for longer shelf life and easier transportation over long distances. This category is essential for international trade, as it enables producers to export broiler meat to distant markets without compromising quality. Frozen broiler products are also convenient for consumers who prefer to buy in bulk and store meat for extended periods. The processed broiler segment includes a wide range of products such as nuggets, patties, sausages, and deli meats. These products are often seasoned, cooked, or otherwise prepared to enhance flavor and convenience. Processed broiler products cater to the growing demand for ready-to-eat or easy-to-cook meals, driven by busy lifestyles and the increasing popularity of fast food. The processing of broiler meat involves various techniques, including marinating, breading, and smoking, to create diverse product offerings. This segment is also influenced by health trends, with consumers seeking products that are lower in fat, sodium, and artificial additives. The global market for fresh, frozen, and processed broiler products is shaped by factors such as consumer preferences, cultural dietary habits, and economic conditions. In developed regions, there is a growing trend towards organic and free-range broiler products, reflecting a shift towards more sustainable and ethical consumption. In contrast, developing regions may prioritize affordability and accessibility, with frozen and processed products playing a significant role in meeting protein needs. The market is also impacted by technological advancements in processing and packaging, which enhance product quality and safety. Innovations such as vacuum packaging, modified atmosphere packaging, and advanced freezing techniques help maintain the freshness and nutritional value of broiler products. Additionally, the rise of e-commerce and online grocery shopping has expanded the reach of fresh, frozen, and processed broiler products, allowing consumers to access a wider variety of options from the comfort of their homes. Overall, the fresh, frozen, and processed segments of the Global Broiler Farming Market are integral to the industry's ability to cater to diverse consumer demands and adapt to changing market dynamics.

Retail, Catering Services, Processing Food Plants, Others in the Global Broiler Farming Market:

The Global Broiler Farming Market serves various sectors, including retail, catering services, processing food plants, and others, each with distinct requirements and contributions to the market's growth. In the retail sector, broiler products are sold directly to consumers through supermarkets, grocery stores, and local markets. Retailers offer a range of broiler products, from fresh cuts to frozen and processed items, catering to different consumer preferences and budgets. The retail sector plays a crucial role in shaping consumer perceptions and driving demand for broiler products, as it is the primary point of contact between producers and consumers. Retailers also influence market trends by promoting specific products, such as organic or free-range broiler meat, and responding to consumer demands for transparency and sustainability. In the catering services sector, broiler products are a staple ingredient in many cuisines and are widely used by restaurants, hotels, and food service providers. The versatility and affordability of broiler meat make it a popular choice for chefs and caterers, who use it in a variety of dishes, from grilled chicken to elaborate gourmet creations. The catering sector is a significant driver of demand for broiler products, as it requires a consistent supply of high-quality meat to meet the needs of diverse menus and customer preferences. This sector also benefits from the availability of processed broiler products, which offer convenience and consistency in portion sizes and preparation. Processing food plants are another critical area of the Global Broiler Farming Market, where broiler meat is transformed into a wide range of value-added products. These plants utilize advanced technologies and techniques to produce items such as chicken nuggets, sausages, and deli meats, catering to the growing demand for convenient and ready-to-eat options. Processing plants play a vital role in the market by adding value to raw broiler meat and expanding its applications beyond traditional cuts. They also contribute to the market's growth by developing innovative products that align with consumer trends, such as healthier options with reduced fat and sodium content. Other areas of the Global Broiler Farming Market include institutional buyers, such as schools, hospitals, and military organizations, which require large quantities of broiler products for their food service operations. These buyers often prioritize cost-effectiveness and reliability in their purchasing decisions, making frozen and processed broiler products an attractive option. Additionally, the market serves niche segments, such as pet food manufacturers, who use broiler meat as a protein source in their products. Overall, the Global Broiler Farming Market's usage across retail, catering services, processing food plants, and other sectors highlights its versatility and importance in meeting the diverse needs of consumers and businesses worldwide.

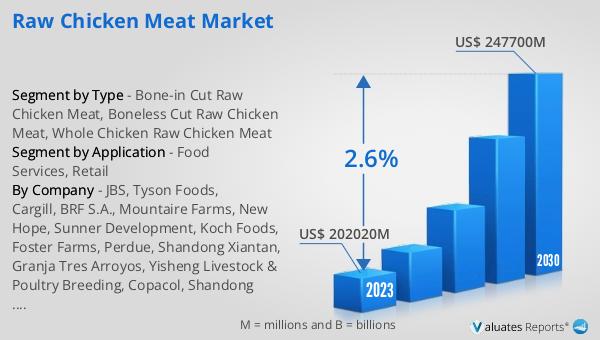

Global Broiler Farming Market Outlook:

The outlook for the Global Broiler Farming Market indicates a robust growth trajectory, with the market valued at approximately $183.41 billion in 2024 and anticipated to expand to around $257.18 billion by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.0% over the forecast period. The market's expansion is driven by several factors, including rising global demand for affordable and high-quality protein sources, advancements in farming and processing technologies, and increasing consumer awareness of health and nutrition. The market is characterized by the presence of key players who hold significant market shares, with the top three manufacturers accounting for nearly 20% of the market. These leading companies include JBS, Tyson Foods Inc., Cargill, BRF S.A., and Sanderson Farms Inc., among others. These companies have established themselves as industry leaders through strategic investments in production capacity, supply chain optimization, and product innovation. Their dominance in the market is further reinforced by their ability to adapt to changing consumer preferences and regulatory requirements. As the market continues to evolve, these key players are likely to play a pivotal role in shaping its future direction, leveraging their expertise and resources to capitalize on emerging opportunities and address challenges such as sustainability and animal welfare.

| Report Metric |

Details |

| Report Name |

Broiler Farming Market |

| Accounted market size in year |

US$ 183410 million |

| Forecasted market size in 2031 |

US$ 257180 million |

| CAGR |

5.0% |

| Base Year |

year |

| Forecasted years |

2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

- Retail

- Catering Services

- Processing Food Plants

- Others

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

JBS, Tyson Foods, Inc., Cargill, BRF S.A., Sanderson Farms Inc., Wens Foodstuff Group, Perdue Farms Inc., Industrias Bachoco, LDC, Plukon Food Group B.V., Wayne Farm, New Hope Liuhe, MHP, PHW-Gruppe, Mountaire Farms, Lihua Animal Husbandry, Sunner Development, Indian Broiler Group |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |