What is Global Aluminium Monobloc Can Market?

The Global Aluminium Monobloc Can Market refers to the worldwide industry focused on the production and distribution of aluminium cans made from a single piece of metal. These cans are known for their seamless design, which provides enhanced durability and a sleek appearance. Aluminium monobloc cans are widely used across various industries due to their lightweight nature, recyclability, and ability to preserve the contents by providing an effective barrier against light, air, and moisture. The market encompasses a range of can sizes and is driven by the increasing demand for sustainable packaging solutions. As consumers and companies become more environmentally conscious, the preference for recyclable materials like aluminium has grown, boosting the market's expansion. Additionally, the versatility of these cans makes them suitable for packaging a variety of products, from beverages and cosmetics to pharmaceuticals and other consumer goods. The market's growth is also supported by technological advancements in can manufacturing, which enhance production efficiency and reduce costs. Overall, the Global Aluminium Monobloc Can Market is a dynamic sector that plays a crucial role in the packaging industry, driven by sustainability trends and the need for high-quality, durable packaging solutions.

Less than 100ml, 100ml-200ml, 200ml-500ml, More than 500ml in the Global Aluminium Monobloc Can Market:

In the Global Aluminium Monobloc Can Market, the categorization based on can size plays a significant role in addressing diverse consumer needs and product specifications. Starting with cans that are less than 100ml, these are typically used for products that require precise dosing or are consumed in smaller quantities. Such cans are ideal for travel-sized cosmetics, sample-sized beverages, or pharmaceutical products where dosage control is crucial. The compact size makes them convenient for on-the-go use, appealing to consumers who prioritize portability and convenience. Moving to the 100ml-200ml category, these cans are often used for energy drinks, small servings of alcoholic beverages, or personal care products like deodorants and hair sprays. This size strikes a balance between portability and sufficient volume, catering to consumers who seek a moderate quantity without compromising on convenience. The 200ml-500ml range is popular for a wide array of beverages, including soft drinks, juices, and ready-to-drink teas and coffees. This size is also favored in the personal care industry for products like shaving creams and body sprays, offering a generous amount while remaining easy to handle. Finally, cans that are more than 500ml are typically used for family-sized beverages or bulk products. These larger cans are suitable for sharing or for consumers who prefer purchasing in larger quantities to reduce packaging waste. They are also used in the food industry for items like cooking sprays or whipped cream. Each size category within the Global Aluminium Monobloc Can Market is designed to meet specific consumer needs, ensuring that products are packaged in a way that enhances user experience while maintaining the integrity and quality of the contents. The diversity in can sizes reflects the market's adaptability to various consumer preferences and industry requirements, highlighting its importance in the global packaging landscape.

Cosmetic, Beverage, Pharmaceutical, Others in the Global Aluminium Monobloc Can Market:

The usage of aluminium monobloc cans spans several key areas, each benefiting from the unique properties of these containers. In the cosmetics industry, aluminium monobloc cans are favored for their ability to protect sensitive formulations from light and air, ensuring product stability and longevity. They are commonly used for aerosol products like hairsprays, deodorants, and shaving creams, where the can's seamless design prevents leakage and maintains pressure. The sleek, metallic finish of aluminium cans also adds a premium feel to cosmetic products, enhancing their appeal to consumers. In the beverage sector, aluminium monobloc cans are a popular choice due to their lightweight nature and excellent recyclability. They are used for packaging a wide range of drinks, from carbonated soft drinks and energy drinks to craft beers and cocktails. The cans' ability to chill quickly and maintain the beverage's carbonation makes them a preferred option for both manufacturers and consumers. Additionally, the recyclability of aluminium aligns with the growing demand for sustainable packaging solutions in the beverage industry. In the pharmaceutical field, aluminium monobloc cans are used for products that require airtight and light-resistant packaging to preserve their efficacy. They are ideal for aerosol medications, topical sprays, and other pharmaceutical products that benefit from the can's protective properties. The cans' durability and resistance to corrosion ensure that the contents remain uncontaminated and safe for use. Beyond these industries, aluminium monobloc cans are also utilized in various other sectors, including household products and industrial applications. Their versatility and ability to be customized with different coatings and finishes make them suitable for a wide range of products, from cleaning sprays to automotive lubricants. Overall, the Global Aluminium Monobloc Can Market serves a diverse array of industries, providing reliable and sustainable packaging solutions that meet the specific needs of each sector.

Global Aluminium Monobloc Can Market Outlook:

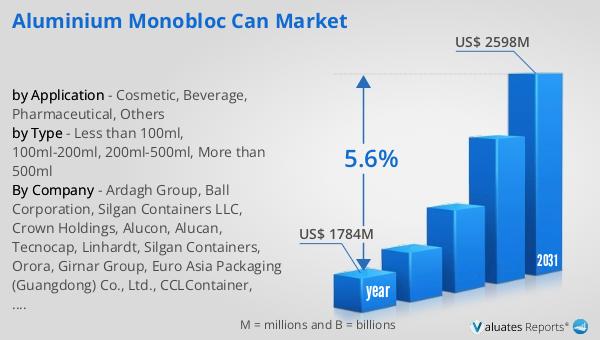

The global market for Aluminium Monobloc Can was valued at $1,784 million in 2024, and it is anticipated to grow significantly, reaching an estimated size of $2,598 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 5.6% over the forecast period. This upward trend is indicative of the increasing demand for aluminium monobloc cans across various industries, driven by their numerous advantages such as durability, recyclability, and the ability to preserve product integrity. The market's expansion is also fueled by the rising consumer preference for sustainable packaging solutions, as aluminium cans are highly recyclable and contribute to reducing environmental impact. Additionally, advancements in can manufacturing technologies have improved production efficiency and reduced costs, further supporting market growth. The versatility of aluminium monobloc cans, which are used in sectors ranging from cosmetics and beverages to pharmaceuticals and household products, also contributes to their growing popularity. As industries continue to seek packaging solutions that align with sustainability goals and consumer preferences, the demand for aluminium monobloc cans is expected to remain strong, driving the market's growth in the coming years.

| Report Metric | Details |

| Report Name | Aluminium Monobloc Can Market |

| Accounted market size in year | US$ 1784 million |

| Forecasted market size in 2031 | US$ 2598 million |

| CAGR | 5.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Ardagh Group, Ball Corporation, Silgan Containers LLC, Crown Holdings, Alucon, Alucan, Tecnocap, Linhardt, Silgan Containers, Orora, Girnar Group, Euro Asia Packaging (Guangdong) Co., Ltd., CCLContainer, Tangshan Junrong Aluminum Co., Ltd., COFCO Packaging Holdings Limited, Jiatian Pharmaceutical Packaging Co., Ltd., Trivium Packaging, Baofeng Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |