What is Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market?

The Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market refers to the specialized sector of the nuclear power industry that deals with the production, distribution, and sales of instrumentation cables specifically designed for nuclear power plants. These cables are crucial for ensuring the safe and efficient operation of nuclear facilities, as they are responsible for transmitting signals and data necessary for monitoring and controlling various processes within the plant. The "Class 1E" designation indicates that these cables meet stringent safety and performance standards required for nuclear applications, ensuring they can withstand harsh environmental conditions and maintain functionality during emergencies. The market for these cables is driven by the ongoing demand for reliable and safe nuclear energy, as well as the need to upgrade and maintain existing nuclear infrastructure. As countries continue to explore nuclear power as a sustainable energy source, the demand for high-quality instrumentation cables is expected to grow, making this market an essential component of the global energy landscape.

in the Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market:

In the Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market, various types of cables are utilized by different customers based on their specific needs and requirements. These cables are designed to perform under extreme conditions, ensuring the safety and reliability of nuclear power plants. One of the primary types of cables used in this market is the Conventional Island Cable, which holds the largest market share. These cables are typically used in the non-nuclear sections of the plant, where they play a crucial role in transmitting data and signals necessary for the plant's operation. They are designed to withstand high temperatures, radiation, and other environmental factors that are common in nuclear power plants. Another important type of cable is the Safety Class Cable, which is used in critical areas of the plant where safety is of utmost importance. These cables are designed to maintain their functionality even in the event of an emergency, such as a fire or an earthquake. They are constructed with materials that can resist high levels of radiation and heat, ensuring that they continue to transmit signals and data without interruption. Additionally, there are Control Cables, which are used to connect various control systems within the plant. These cables are essential for the operation of the plant's control systems, which monitor and regulate the plant's processes. They are designed to be highly reliable and durable, capable of withstanding the harsh conditions of a nuclear power plant. Instrumentation Cables are another type used in this market, specifically designed for transmitting low-level signals from sensors and instruments to control systems. These cables are crucial for the accurate monitoring of the plant's processes, ensuring that the plant operates safely and efficiently. They are constructed with materials that provide excellent resistance to radiation and electromagnetic interference, ensuring that the signals they transmit are accurate and reliable. Power Cables are also used in nuclear power plants, providing the necessary electrical power to various systems and components within the plant. These cables are designed to handle high voltages and currents, ensuring that the plant's systems receive the power they need to operate. They are constructed with materials that can withstand high temperatures and radiation, ensuring their reliability and safety. Finally, there are Specialty Cables, which are designed for specific applications within the plant. These cables are often custom-made to meet the unique requirements of a particular system or component, ensuring that they provide the necessary performance and reliability. Overall, the Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market offers a wide range of cable types, each designed to meet the specific needs of nuclear power plants. These cables are essential for the safe and efficient operation of nuclear facilities, ensuring that they can continue to provide reliable and sustainable energy.

in the Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market:

The Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market serves a variety of applications within nuclear power plants, each requiring specific types of cables to ensure safe and efficient operation. One of the primary applications is in the monitoring and control systems of the plant. These systems rely on instrumentation cables to transmit data from sensors and instruments to control systems, allowing operators to monitor the plant's processes and make necessary adjustments. The accuracy and reliability of these cables are crucial, as any disruption in data transmission could lead to unsafe operating conditions. Another important application is in the safety systems of the plant. These systems are designed to protect the plant and its personnel in the event of an emergency, such as a fire or an earthquake. Safety Class Cables are used in these systems to ensure that they continue to function even under extreme conditions. These cables are constructed with materials that can withstand high levels of radiation and heat, ensuring that they maintain their functionality during emergencies. Additionally, control systems within the plant rely on control cables to connect various components and systems. These cables are essential for the operation of the plant's control systems, which regulate the plant's processes and ensure that they operate within safe parameters. The reliability and durability of these cables are critical, as any failure could lead to a loss of control over the plant's processes. Power distribution is another key application of instrumentation cables in nuclear power plants. Power cables are used to provide electrical power to various systems and components within the plant, ensuring that they receive the necessary power to operate. These cables are designed to handle high voltages and currents, ensuring that they can deliver the required power safely and efficiently. Finally, there are specialty applications within the plant that require custom-made cables to meet specific requirements. These specialty cables are often used in unique systems or components that have specific performance and reliability needs. Overall, the Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market plays a crucial role in ensuring the safe and efficient operation of nuclear power plants. The various applications of these cables highlight their importance in maintaining the reliability and safety of nuclear facilities, making them an essential component of the global energy landscape.

Global Class 1E Nuclear Power Plant Instrumentation Cables Sales Market Outlook:

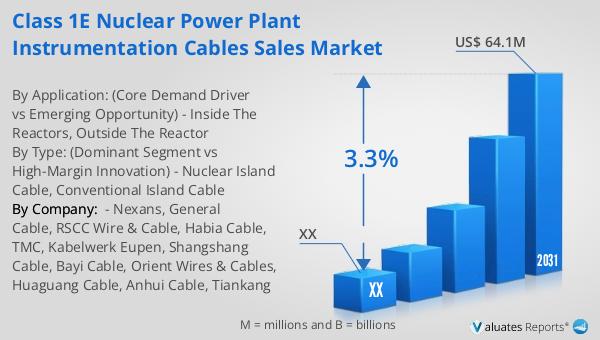

The market outlook for the Global Class 1E Nuclear Power Plant Instrumentation Cables sector indicates a significant growth trajectory. In 2024, the market size was valued at approximately $51.2 million, and it is projected to expand to a revised size of $64.1 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.3% during the forecast period from 2025 to 2031. This growth is driven by the increasing demand for reliable and safe nuclear energy, as well as the need to upgrade and maintain existing nuclear infrastructure. The market is dominated by the top four manufacturers, who collectively hold a market share exceeding 55%. Geographically, China emerges as the largest market, accounting for over 30% of the global share, followed by Europe and the United States, which together hold about 50% of the market share. In terms of product segmentation, the Conventional Island Cable stands out as the largest segment, capturing over 85% of the market share. This dominance underscores the critical role these cables play in the non-nuclear sections of the plant, where they are essential for transmitting data and signals necessary for the plant's operation. The market's growth prospects are further bolstered by the ongoing advancements in cable technology, which are enhancing the performance and reliability of these essential components in nuclear power plants.

| Report Metric | Details |

| Report Name | Class 1E Nuclear Power Plant Instrumentation Cables Sales Market |

| Forecasted market size in 2031 | US$ 64.1 million |

| CAGR | 3.3% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Nexans, General Cable, RSCC Wire & Cable, Habia Cable, TMC, Kabelwerk Eupen, Shangshang Cable, Bayi Cable, Orient Wires & Cables, Huaguang Cable, Anhui Cable, Tiankang |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |