What is Global Opaque Fused Quartz Market?

The Global Opaque Fused Quartz Market is a specialized segment within the broader quartz industry, focusing on the production and application of opaque fused quartz materials. These materials are known for their exceptional thermal and chemical stability, making them highly valuable in various high-tech industries. Opaque fused quartz is produced by melting high-purity silica sand at extremely high temperatures, resulting in a material that is both durable and resistant to thermal shock. This market is driven by the increasing demand for high-performance materials in sectors such as semiconductors, photovoltaics, and advanced lighting solutions. The unique properties of opaque fused quartz, such as its low thermal expansion and high resistance to chemical corrosion, make it an ideal choice for applications that require precision and reliability. As industries continue to innovate and develop new technologies, the demand for opaque fused quartz is expected to grow, further solidifying its importance in the global market. The market is characterized by a focus on high purity levels, with products often exceeding 99.8% purity to meet the stringent requirements of advanced applications. This emphasis on quality and performance ensures that opaque fused quartz remains a critical component in cutting-edge technological advancements.

Above 99.8%, Above 99.9% in the Global Opaque Fused Quartz Market:

In the realm of the Global Opaque Fused Quartz Market, purity levels play a crucial role in determining the material's suitability for various applications. Products with a purity level above 99.8% are highly sought after due to their superior performance characteristics. These materials are primarily used in industries where even the slightest impurity can lead to significant performance degradation or failure. For instance, in the semiconductor industry, the presence of impurities can affect the electrical properties of the materials, leading to inefficiencies or defects in the final product. Therefore, maintaining a high purity level is essential to ensure the reliability and efficiency of semiconductor components. Similarly, in the photovoltaic industry, high-purity opaque fused quartz is used in the production of solar cells. The material's ability to withstand high temperatures and resist chemical corrosion makes it an ideal choice for this application, where efficiency and longevity are paramount. Products with a purity level above 99.9% are even more specialized, catering to applications that demand the utmost precision and reliability. These materials are often used in research and development settings, where cutting-edge technologies are being developed and tested. The high purity level ensures that the material's properties remain consistent, allowing researchers to achieve accurate and reproducible results. In the illumination industry, high-purity opaque fused quartz is used in the production of advanced lighting solutions, such as high-intensity discharge lamps and LED components. The material's excellent thermal stability and resistance to thermal shock make it an ideal choice for these applications, where performance and durability are critical. Overall, the emphasis on high purity levels in the Global Opaque Fused Quartz Market underscores the importance of quality and performance in meeting the demands of advanced technological applications.

Semiconductor, Photovoltaic, Illumination, Other in the Global Opaque Fused Quartz Market:

The Global Opaque Fused Quartz Market finds its applications in several key areas, including semiconductors, photovoltaics, illumination, and other specialized fields. In the semiconductor industry, opaque fused quartz is used in the manufacturing of various components, such as wafers and crucibles. Its high thermal stability and low thermal expansion make it an ideal material for processes that involve extreme temperatures and precise measurements. The material's resistance to chemical corrosion also ensures that it can withstand the harsh environments often encountered in semiconductor manufacturing. In the photovoltaic industry, opaque fused quartz is used in the production of solar cells and panels. Its ability to withstand high temperatures and resist chemical degradation makes it an essential material for ensuring the efficiency and longevity of solar energy systems. The material's optical properties also play a crucial role in maximizing the absorption of sunlight, thereby enhancing the overall performance of photovoltaic devices. In the illumination industry, opaque fused quartz is used in the production of advanced lighting solutions, such as high-intensity discharge lamps and LED components. Its excellent thermal stability and resistance to thermal shock make it an ideal choice for applications that require high performance and durability. Additionally, the material's optical properties allow for precise control of light emission, enabling the development of innovative lighting solutions that meet the demands of modern consumers. Beyond these primary applications, opaque fused quartz is also used in other specialized fields, such as aerospace, telecommunications, and scientific research. In these areas, the material's unique properties are leveraged to develop cutting-edge technologies and solutions that push the boundaries of what is possible. Overall, the versatility and performance of opaque fused quartz make it a critical component in a wide range of industries, driving innovation and advancement across the globe.

Global Opaque Fused Quartz Market Outlook:

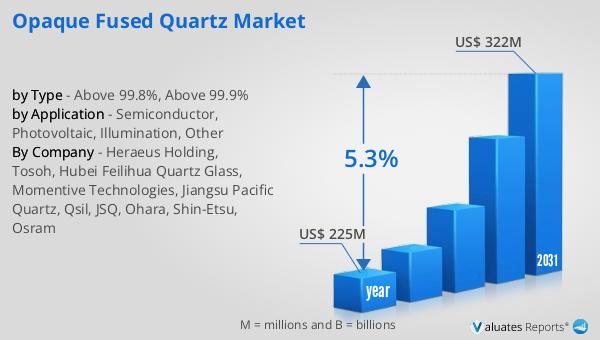

The global market for Opaque Fused Quartz was valued at $225 million in 2024 and is anticipated to grow to a revised size of $322 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.3% during the forecast period. This growth is primarily driven by the increasing demand for high-purity opaque fused silica, particularly those with a purity greater than 99.8%. The North American market for Opaque Fused Quartz is projected to experience significant growth, with estimates indicating an increase from its 2024 valuation to a higher figure by 2031, maintaining a steady CAGR throughout the forecast period from 2025 to 2031. This upward trend is indicative of the growing importance of opaque fused quartz in various high-tech industries, where its unique properties are leveraged to enhance performance and reliability. The emphasis on high purity levels underscores the critical role that quality and precision play in meeting the stringent requirements of advanced applications. As industries continue to evolve and innovate, the demand for high-performance materials like opaque fused quartz is expected to rise, further solidifying its position as a vital component in the global market. The market outlook highlights the potential for growth and expansion, driven by technological advancements and the increasing need for reliable and efficient materials in cutting-edge applications.

| Report Metric | Details |

| Report Name | Opaque Fused Quartz Market |

| Accounted market size in year | US$ 225 million |

| Forecasted market size in 2031 | US$ 322 million |

| CAGR | 5.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Heraeus Holding, Tosoh, Hubei Feilihua Quartz Glass, Momentive Technologies, Jiangsu Pacific Quartz, Qsil, JSQ, Ohara, Shin-Etsu, Osram |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |