What is Global Heat Transfer Dye Sublimation Printer Market?

The Global Heat Transfer Dye Sublimation Printer Market is a specialized segment within the printing industry that focuses on the use of dye sublimation technology for transferring images onto various materials. This market is characterized by its ability to produce high-quality, vibrant prints that are durable and resistant to fading. Dye sublimation printers work by using heat to transfer dye onto materials such as fabric, paper, or plastic. This process is particularly popular in industries that require detailed and colorful prints, such as fashion, home decor, and advertising. The market is driven by the increasing demand for customized and personalized products, as well as advancements in printing technology that have made these printers more efficient and cost-effective. Additionally, the growing trend of digital printing and the shift towards eco-friendly printing solutions are also contributing to the market's expansion. As businesses and consumers continue to seek high-quality printing solutions, the Global Heat Transfer Dye Sublimation Printer Market is expected to see significant growth in the coming years.

Small-format Printers, Large-format Printers in the Global Heat Transfer Dye Sublimation Printer Market:

Small-format and large-format printers play crucial roles in the Global Heat Transfer Dye Sublimation Printer Market, each catering to different needs and applications. Small-format printers are typically used for personal or small business purposes, where the demand for customized products like t-shirts, mugs, and small promotional items is high. These printers are compact, making them suitable for limited spaces, and they offer a cost-effective solution for businesses that do not require large-scale production. Small-format printers are ideal for producing high-quality prints with intricate details, making them popular among hobbyists and small enterprises that focus on personalized gifts and merchandise. On the other hand, large-format printers are designed for industrial and commercial use, where the need for large-scale production and high-volume printing is paramount. These printers are capable of handling larger materials and producing prints that are suitable for applications such as banners, billboards, and large signage. The large-format printers dominate the market due to their versatility and ability to produce high-quality prints on a larger scale. They are essential for businesses that require extensive printing capabilities, such as advertising agencies, textile manufacturers, and interior decorators. The demand for large-format printers is driven by the need for vibrant and durable prints that can withstand outdoor conditions and maintain their quality over time. Both small-format and large-format printers are integral to the Global Heat Transfer Dye Sublimation Printer Market, each serving distinct purposes and catering to different segments of the market. As technology continues to advance, these printers are becoming more efficient, offering faster printing speeds and improved print quality, which in turn is driving their adoption across various industries. The choice between small-format and large-format printers ultimately depends on the specific needs of the business or individual, with considerations such as production volume, print size, and budget playing a significant role in the decision-making process.

Apparel Products, Home Decoration and Interior, Soft Signage and Billboard, Others in the Global Heat Transfer Dye Sublimation Printer Market:

The Global Heat Transfer Dye Sublimation Printer Market finds extensive usage across various sectors, including apparel products, home decoration and interior, soft signage and billboard, and other applications. In the apparel industry, dye sublimation printers are used to create vibrant and durable prints on fabrics, making them ideal for producing customized clothing items such as t-shirts, sportswear, and fashion accessories. The ability to produce intricate designs and vibrant colors makes these printers a popular choice for fashion designers and clothing manufacturers who seek to offer unique and personalized products to their customers. In the realm of home decoration and interior design, dye sublimation printers are used to create custom prints on items such as curtains, cushions, and wall art. The high-quality prints produced by these printers add a touch of personalization and creativity to home interiors, allowing homeowners to express their individual style and preferences. Soft signage and billboards also benefit from the capabilities of dye sublimation printers, as they require large, eye-catching prints that can withstand outdoor conditions. These printers are used to produce banners, flags, and other promotional materials that are essential for advertising and marketing campaigns. The durability and vibrancy of the prints make them suitable for both indoor and outdoor use, ensuring that the message remains visible and impactful over time. Other applications of dye sublimation printers include the production of promotional items, personalized gifts, and custom merchandise. The versatility of these printers allows businesses to explore new opportunities and expand their product offerings, catering to the growing demand for customized and personalized products. As the market continues to evolve, the usage of dye sublimation printers is expected to expand further, driven by advancements in technology and the increasing demand for high-quality, customized printing solutions across various industries.

Global Heat Transfer Dye Sublimation Printer Market Outlook:

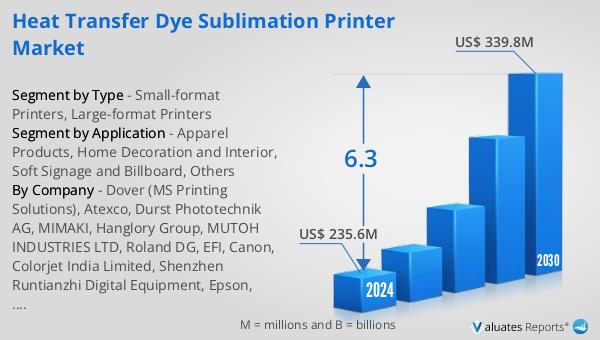

The global market for Heat Transfer Dye Sublimation Printers was valued at $249 million in 2024 and is anticipated to grow to a revised size of $379 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.3% during the forecast period. Within this market, large-format printers represent the largest segment, accounting for approximately 90% of the market share. This dominance is attributed to their extensive use in industries that require large-scale, high-quality printing solutions, such as advertising and textile manufacturing. Large-format printers are favored for their ability to produce vibrant, durable prints on a larger scale, making them indispensable for applications like billboards, banners, and large signage. In terms of application, apparel products hold a significant share of about 60%, highlighting the importance of dye sublimation printers in the fashion and textile industry. The demand for customized and personalized clothing items has driven the adoption of these printers, as they offer the ability to produce intricate designs and vibrant colors on various fabrics. As the market continues to grow, the focus remains on enhancing the efficiency and capabilities of dye sublimation printers to meet the evolving needs of businesses and consumers alike.

| Report Metric | Details |

| Report Name | Heat Transfer Dye Sublimation Printer Market |

| Accounted market size in year | US$ 249 million |

| Forecasted market size in 2031 | US$ 379 million |

| CAGR | 6.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dover (MS Printing Solutions), Atexco, Durst Phototechnik AG, MIMAKI, Hanglory Group, MUTOH INDUSTRIES LTD, Roland DG, EFI, Canon, Colorjet India Limited, Shenzhen Runtianzhi Digital Equipment, Epson, Shanghai Signstar Digital Technology, JHF, HP |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |