What is Global Reprocessing Medical Equipment Market?

The Global Reprocessing Medical Equipment Market is a significant segment within the healthcare industry, focusing on the reprocessing of medical devices to ensure they can be safely reused. This market is driven by the need to reduce medical waste and healthcare costs while maintaining high standards of patient safety. Reprocessing involves cleaning, disinfecting, and sterilizing used medical equipment, making it safe for subsequent use. This process is crucial in extending the life of medical devices, thereby reducing the need for new equipment and minimizing environmental impact. The market encompasses a wide range of devices, including surgical instruments, catheters, and endoscopes, among others. With advancements in technology and stringent regulatory guidelines, the reprocessing of medical equipment has become more efficient and reliable. The growing awareness of sustainable practices in healthcare further propels the demand for reprocessed medical devices. As healthcare facilities strive to balance cost-effectiveness with quality care, the Global Reprocessing Medical Equipment Market is poised for continued growth, offering solutions that align with both economic and environmental goals. This market not only supports the healthcare industry's sustainability efforts but also ensures that medical facilities can provide high-quality care without compromising safety or efficacy.

Cardiovascular Devices, General Surgery Devices, Laparoscopic Devices, Others in the Global Reprocessing Medical Equipment Market:

Cardiovascular devices are a critical component of the Global Reprocessing Medical Equipment Market, as they are essential in diagnosing and treating heart-related conditions. These devices include catheters, guidewires, and electrophysiology catheters, which are often reprocessed to ensure cost-effectiveness and sustainability. Reprocessing cardiovascular devices involves meticulous cleaning and sterilization processes to maintain their functionality and safety. This practice not only reduces the financial burden on healthcare facilities but also minimizes medical waste, contributing to environmental conservation. General surgery devices, such as forceps, scissors, and retractors, are also integral to the reprocessing market. These instruments are used in a variety of surgical procedures and require precise reprocessing to ensure they remain sterile and effective for reuse. The reprocessing of general surgery devices helps healthcare providers manage costs while maintaining high standards of patient care. Laparoscopic devices, used in minimally invasive surgeries, are another key segment within the reprocessing market. These devices, including trocars and laparoscopes, are reprocessed to extend their lifespan and reduce the need for new equipment. The reprocessing of laparoscopic devices is particularly important as it supports the growing trend towards minimally invasive procedures, which offer numerous benefits such as reduced recovery times and lower risk of complications. Other devices within the reprocessing market include orthopedic instruments, endoscopes, and respiratory equipment. Each of these categories requires specific reprocessing techniques to ensure they meet safety and efficacy standards. The reprocessing of orthopedic instruments, for example, involves rigorous cleaning and sterilization to prevent infections and ensure successful surgical outcomes. Endoscopes, used for diagnostic and therapeutic procedures, require careful reprocessing to maintain their delicate components and ensure accurate performance. Respiratory equipment, such as ventilator circuits and breathing masks, is reprocessed to ensure they are free from contaminants and safe for patient use. The Global Reprocessing Medical Equipment Market plays a vital role in supporting healthcare facilities' efforts to provide high-quality care while managing costs and reducing environmental impact. By extending the life of medical devices through reprocessing, healthcare providers can allocate resources more efficiently and focus on delivering optimal patient outcomes. As the demand for sustainable healthcare solutions continues to grow, the reprocessing market is expected to expand, offering innovative solutions that align with both economic and environmental objectives.

Medical Hygiene, Plastic Surgery, Others in the Global Reprocessing Medical Equipment Market:

The usage of the Global Reprocessing Medical Equipment Market extends to various areas, including medical hygiene, plastic surgery, and other specialized fields. In the realm of medical hygiene, reprocessed equipment plays a crucial role in maintaining sterile environments and preventing the spread of infections. Hospitals and clinics rely on reprocessed devices to ensure that all instruments used in patient care are free from contaminants. This is particularly important in settings where infection control is paramount, such as operating rooms and intensive care units. By utilizing reprocessed equipment, healthcare facilities can uphold stringent hygiene standards while managing costs effectively. In plastic surgery, the reprocessing of medical equipment is essential for maintaining the precision and safety required in cosmetic and reconstructive procedures. Instruments used in plastic surgery, such as scalpels, forceps, and retractors, are reprocessed to ensure they remain sharp and sterile for each use. This not only enhances the quality of surgical outcomes but also reduces the financial burden on both patients and healthcare providers. The reprocessing of plastic surgery devices supports the growing demand for cosmetic procedures by offering cost-effective solutions without compromising safety or efficacy. Beyond medical hygiene and plastic surgery, the Global Reprocessing Medical Equipment Market also serves other specialized areas, such as ophthalmology, dentistry, and orthopedics. In ophthalmology, reprocessed devices like surgical instruments and diagnostic tools are used to ensure precise and safe eye care. The reprocessing of these devices helps ophthalmologists provide high-quality care while managing costs and reducing waste. In dentistry, reprocessed equipment such as dental handpieces and surgical instruments are essential for maintaining oral hygiene and ensuring successful dental procedures. The reprocessing of dental devices supports the delivery of cost-effective dental care while adhering to strict hygiene standards. In orthopedics, reprocessed instruments and implants are used to perform surgeries and treat musculoskeletal conditions. The reprocessing of orthopedic devices ensures they remain sterile and functional, supporting successful surgical outcomes and patient recovery. The Global Reprocessing Medical Equipment Market plays a vital role in supporting various healthcare fields by providing sustainable and cost-effective solutions. By extending the life of medical devices through reprocessing, healthcare providers can allocate resources more efficiently and focus on delivering optimal patient outcomes. As the demand for sustainable healthcare solutions continues to grow, the reprocessing market is expected to expand, offering innovative solutions that align with both economic and environmental objectives.

Global Reprocessing Medical Equipment Market Outlook:

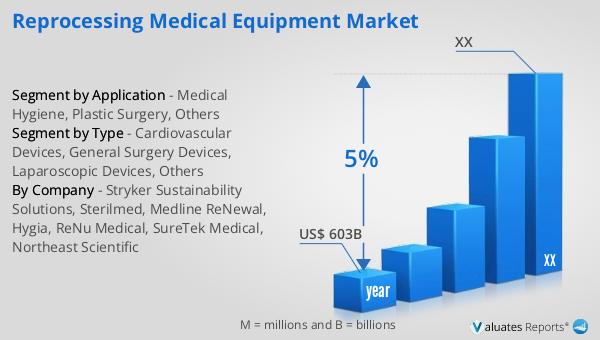

Our research indicates that the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth trajectory underscores the increasing demand for medical devices across various healthcare sectors, driven by advancements in technology and the rising prevalence of chronic diseases. The expansion of the medical device market is also fueled by the growing emphasis on improving healthcare infrastructure and the adoption of innovative medical technologies. As healthcare providers strive to enhance patient care and outcomes, the demand for advanced medical devices continues to rise. This growth is further supported by the increasing focus on personalized medicine and the integration of digital technologies in healthcare delivery. The projected growth of the medical device market highlights the importance of continued investment in research and development to drive innovation and meet the evolving needs of healthcare providers and patients. As the market expands, it presents significant opportunities for stakeholders to capitalize on emerging trends and technologies, ultimately contributing to the advancement of global healthcare systems. The anticipated growth of the medical device market reflects the ongoing efforts to improve healthcare access and quality, ensuring that patients receive the best possible care. This positive outlook for the medical device market underscores the critical role that these devices play in enhancing patient outcomes and supporting the delivery of high-quality healthcare services worldwide.

| Report Metric | Details |

| Report Name | Reprocessing Medical Equipment Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Stryker Sustainability Solutions, Sterilmed, Medline ReNewal, Hygia, ReNu Medical, SureTek Medical, Northeast Scientific |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |