What is Global Gas Sensor for Automotive Market?

The Global Gas Sensor for Automotive Market is a rapidly evolving sector that plays a crucial role in enhancing vehicle safety, efficiency, and environmental compliance. Gas sensors in automobiles are essential for detecting and measuring the concentration of various gases emitted by vehicles, such as carbon monoxide, nitrogen oxides, and hydrocarbons. These sensors are integral to the vehicle's emission control system, ensuring that the emissions remain within the regulatory limits set by governments worldwide. The market for these sensors is driven by the increasing demand for vehicles that meet stringent emission standards, the growing awareness of environmental issues, and the technological advancements in sensor technology. As automotive manufacturers strive to produce cleaner and more efficient vehicles, the demand for advanced gas sensors continues to rise. These sensors not only help in reducing harmful emissions but also contribute to improving the overall performance and fuel efficiency of vehicles. With the automotive industry undergoing a significant transformation towards electrification and hybridization, the role of gas sensors is becoming even more critical in ensuring that vehicles are both environmentally friendly and high-performing.

Exhaust Gas Sensor, Intake Gas Sensor in the Global Gas Sensor for Automotive Market:

Exhaust gas sensors and intake gas sensors are two primary types of sensors used in the Global Gas Sensor for Automotive Market, each serving distinct yet complementary roles in vehicle operation. Exhaust gas sensors are primarily responsible for monitoring the gases emitted from the vehicle's exhaust system. These sensors play a pivotal role in ensuring that the emissions are within the permissible limits, thereby helping in reducing the environmental impact of vehicles. They detect harmful gases such as carbon monoxide (CO), nitrogen oxides (NOx), and hydrocarbons (HC), which are byproducts of the combustion process in the engine. By providing real-time data on the concentration of these gases, exhaust gas sensors enable the vehicle's engine control unit (ECU) to adjust the air-fuel mixture, ignition timing, and other parameters to optimize combustion efficiency and minimize emissions. This not only helps in meeting stringent emission regulations but also enhances the vehicle's fuel efficiency and performance. On the other hand, intake gas sensors are used to monitor the air entering the engine. These sensors measure parameters such as air mass flow, temperature, and pressure, which are critical for determining the optimal air-fuel ratio for combustion. By ensuring that the engine receives the right amount of air, intake gas sensors help in achieving efficient combustion, reducing fuel consumption, and minimizing emissions. They also play a crucial role in turbocharged engines, where precise control of the air intake is essential for maximizing performance and efficiency. Together, exhaust and intake gas sensors form an integral part of the vehicle's emission control system, working in tandem to ensure that the engine operates efficiently and cleanly. As the automotive industry continues to evolve, the demand for advanced gas sensors is expected to grow, driven by the need for vehicles that are both environmentally friendly and high-performing. With advancements in sensor technology, modern gas sensors are becoming more accurate, reliable, and capable of operating in harsh automotive environments. This is enabling automotive manufacturers to develop vehicles that not only meet but exceed emission standards, contributing to a cleaner and more sustainable future.

Passenger Vehicle, Commercial Vehicle in the Global Gas Sensor for Automotive Market:

The usage of gas sensors in the Global Gas Sensor for Automotive Market is particularly significant in two major vehicle categories: passenger vehicles and commercial vehicles. In passenger vehicles, gas sensors are primarily used to enhance the safety, efficiency, and environmental compliance of the vehicle. With the increasing awareness of environmental issues and the implementation of stringent emission regulations, automotive manufacturers are focusing on developing passenger vehicles that are both fuel-efficient and low-emission. Gas sensors play a crucial role in achieving this by providing real-time data on the concentration of various gases emitted by the vehicle. This data is used by the vehicle's engine control unit (ECU) to optimize combustion efficiency, reduce emissions, and improve fuel economy. In addition to emission control, gas sensors also contribute to the overall performance and safety of passenger vehicles by ensuring that the engine operates efficiently and reliably. In commercial vehicles, the role of gas sensors is even more critical due to the larger size and higher emission levels of these vehicles. Commercial vehicles, such as trucks and buses, are subject to stringent emission regulations, and non-compliance can result in significant penalties. Gas sensors help in ensuring that commercial vehicles meet these regulations by monitoring the emissions and providing real-time data to the vehicle's ECU. This enables the ECU to make necessary adjustments to the engine parameters, ensuring that the emissions remain within the permissible limits. Moreover, gas sensors also contribute to the fuel efficiency and performance of commercial vehicles by optimizing the combustion process. This is particularly important for commercial vehicles, as fuel costs constitute a significant portion of their operating expenses. By improving fuel efficiency, gas sensors help in reducing the overall operating costs of commercial vehicles, making them more economical and sustainable. Furthermore, with the increasing focus on reducing the carbon footprint of commercial vehicles, the demand for advanced gas sensors is expected to grow, driving the development of cleaner and more efficient commercial vehicles. Overall, the usage of gas sensors in both passenger and commercial vehicles is essential for meeting emission regulations, improving fuel efficiency, and enhancing vehicle performance, contributing to a cleaner and more sustainable automotive industry.

Global Gas Sensor for Automotive Market Outlook:

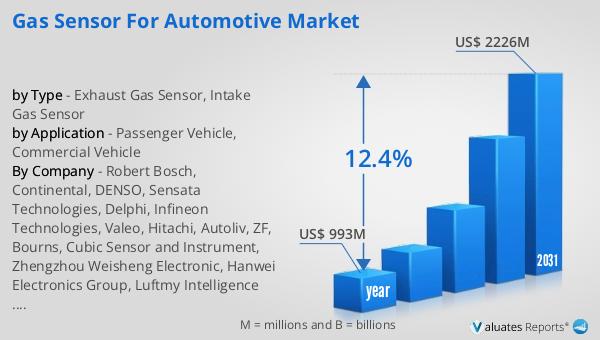

The global market for gas sensors in the automotive sector is experiencing significant growth, reflecting the increasing demand for vehicles that are both environmentally friendly and high-performing. In 2024, the market was valued at approximately $993 million, indicating a robust interest in these essential components. Looking ahead, the market is projected to expand substantially, reaching an estimated size of $2,226 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 12.4% over the forecast period. This impressive growth rate underscores the critical role that gas sensors play in the automotive industry, particularly as manufacturers strive to meet stringent emission standards and enhance vehicle efficiency. The rising awareness of environmental issues and the push for cleaner, more efficient vehicles are key drivers of this market expansion. As automotive technology continues to advance, the demand for sophisticated gas sensors that can accurately monitor and control emissions is expected to increase. This growth is not only a testament to the importance of gas sensors in modern vehicles but also highlights the ongoing transformation of the automotive industry towards sustainability and innovation. The market outlook for gas sensors in the automotive sector is indeed promising, with significant opportunities for growth and development in the coming years.

| Report Metric | Details |

| Report Name | Gas Sensor for Automotive Market |

| Accounted market size in year | US$ 993 million |

| Forecasted market size in 2031 | US$ 2226 million |

| CAGR | 12.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Robert Bosch, Continental, DENSO, Sensata Technologies, Delphi, Infineon Technologies, Valeo, Hitachi, Autoliv, ZF, Bourns, Cubic Sensor and Instrument, Zhengzhou Weisheng Electronic, Hanwei Electronics Group, Luftmy Intelligence Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |